M&G Investments at a glance:

M&G Investments is part of M&G plc, an international financial services company. Helping people to manage and grow their wealth responsibly is our goal.

Globally, we manage over CHF 336,4 billion (as at 31 December 2023) on behalf of private and professional investors, including banks, pension funds, insurance companies, sovereign wealth funds, family offices and advisers.

We are one of the largest managers of private assets in Europe. We are also recognised for our global fixed-income expertise, our long-standing experience in multi-asset solutions and our innovative strength in equities. This strength includes a growing range of thematic equity funds focussed on sustainability. Thanks to our size, we have unique access to listed investment opportunities and private markets. We offer our clients a wide range of funds, as well as customised solutions.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

We have written many times on QE (Quantitative Easing) and QT (Quantitative Tightening); however, we have never talked about QN. QN is the ultimate goal for central banks – but what exactly is it?

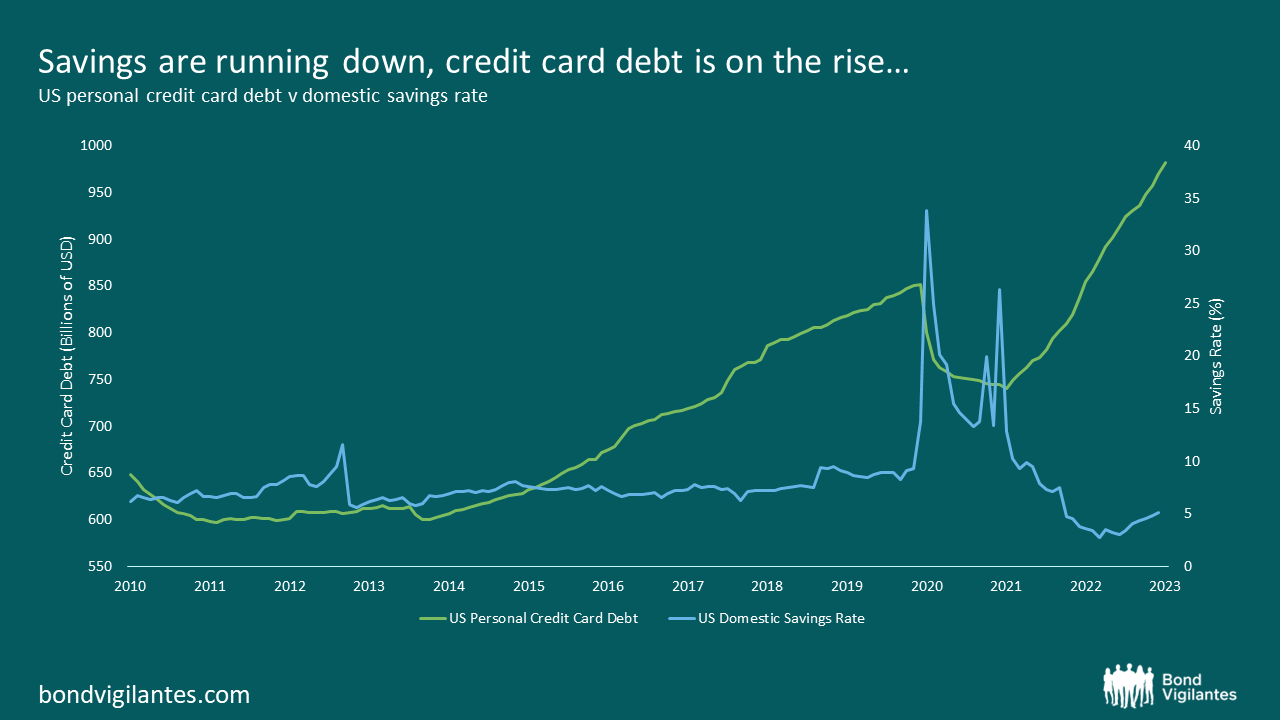

Consumption spending accounts for approximately two-thirds of the US economy. It is vital that we understand the dynamics of the consumer because if the consumer falters, so does the US economy, which has far-reaching consequence

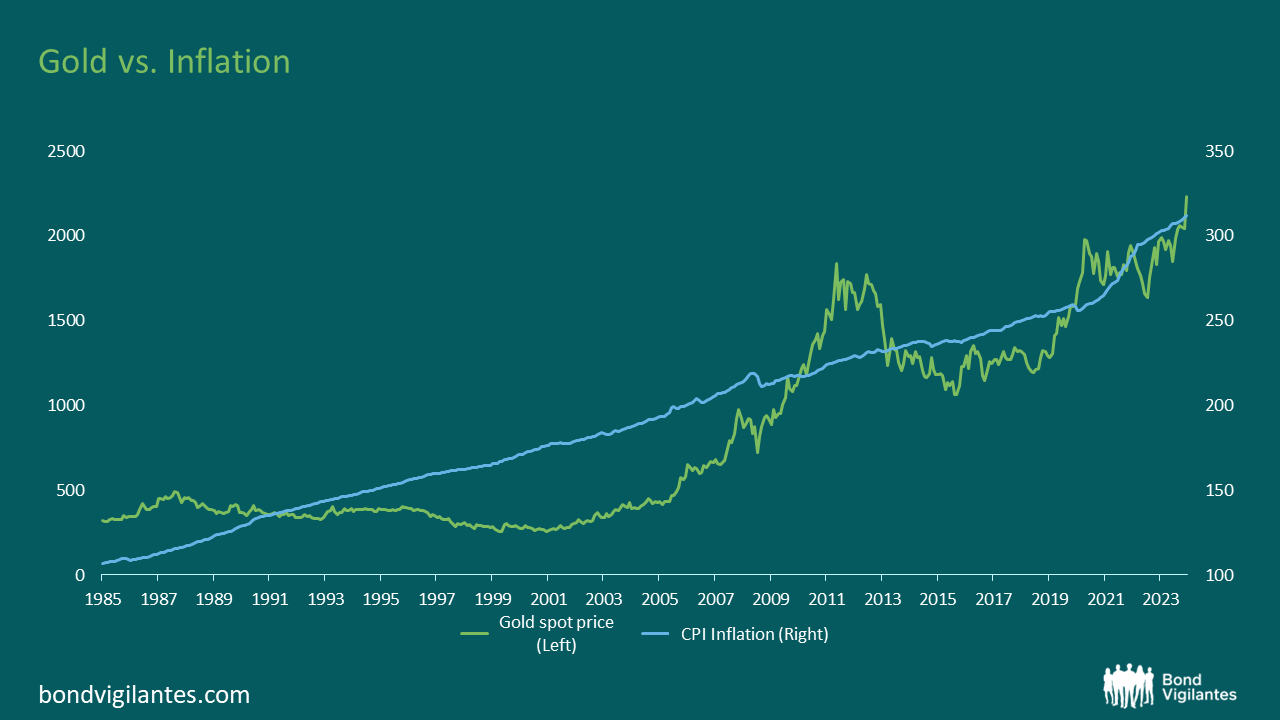

Renowned for its role as a hedge against economic uncertainty and inflation, gold has long captivated investors. One key factor influencing gold’s price is the relationship between real yields and inflation. Over the long term, gold has protected one against the pernicious effects of inflation and remains a powerful diversifier within an investment portfolio:

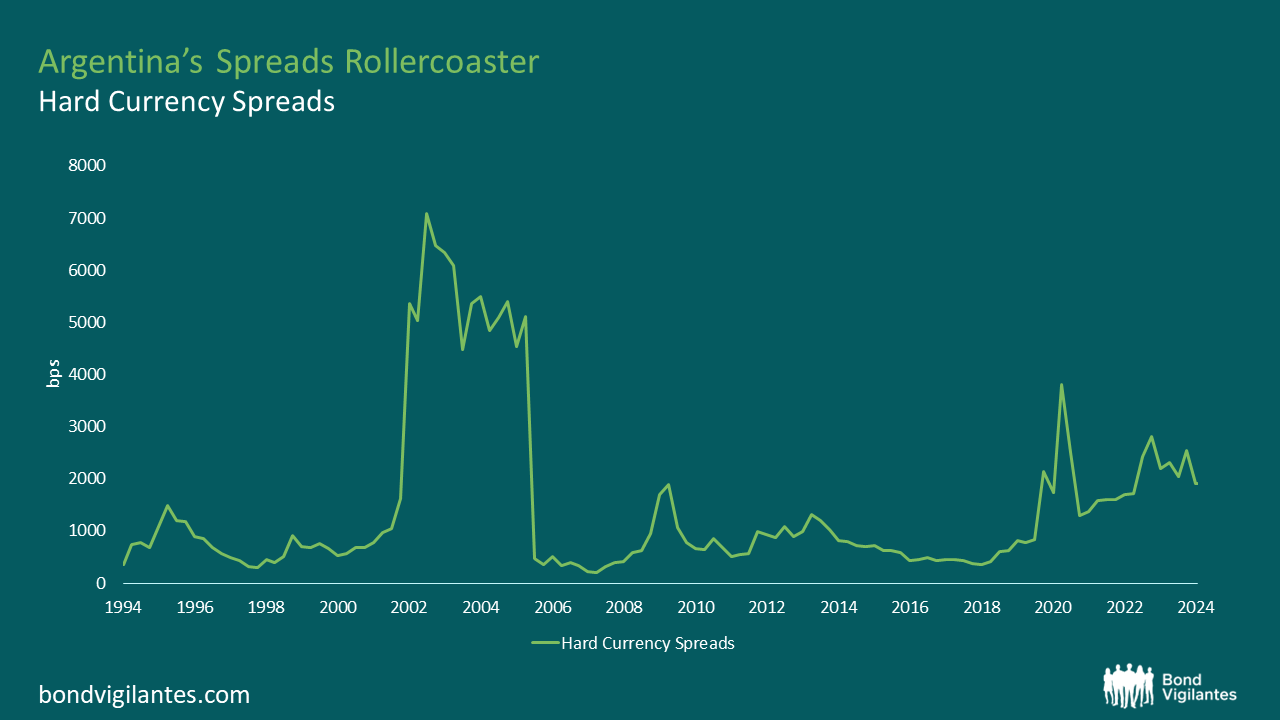

Javier Milei, Argentina’s newly elected president, shares similarities with Roosevelt in that he has inherited, to put it mildly, a struggling economy, and has begun attempting to implement reforms in very quick order.

The yield curve in Japan is reaching intriguing levels. The Bank of Japan (BoJ) has remained resolute, maintaining an ultra-accommodative monetary policy in a world aggressively hiking interest rates to stem inflation.

What’s more, if you’d taken a 12 month sabbatical through 2023, spent on a desert island listening to the Smiths and the Velvet Underground, then upon firing up your Bloomberg on New Year’s Day, what would be most surprising of all, is that none of this uncertainty is visible in markets.

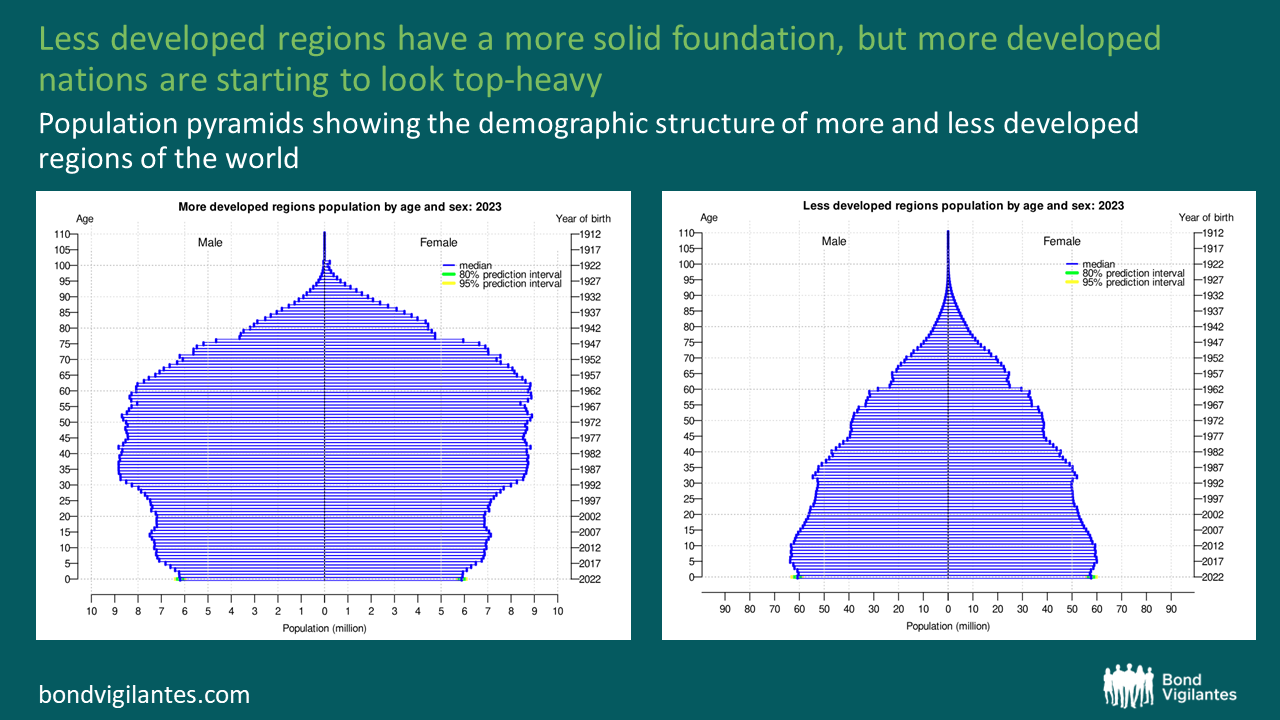

Demographic changes are set to have a significant impact on the world economy in the coming decades, as we have discussed on a number of occasions.

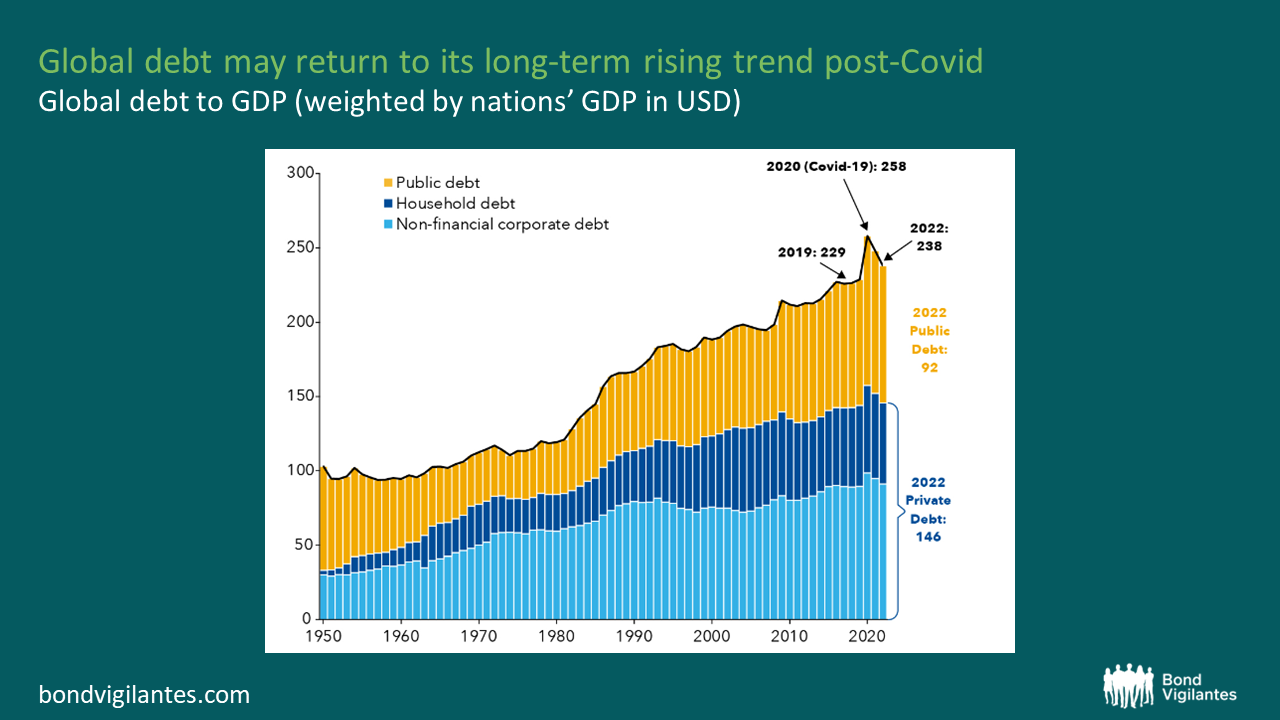

Governments have traditionally argued that as long as debt remains manageable and serviceable without difficulty, there’s little cause for concern. While this notion holds some truth, the reality is that recent growth has largely been fueled by an insurmountable increase in debt.

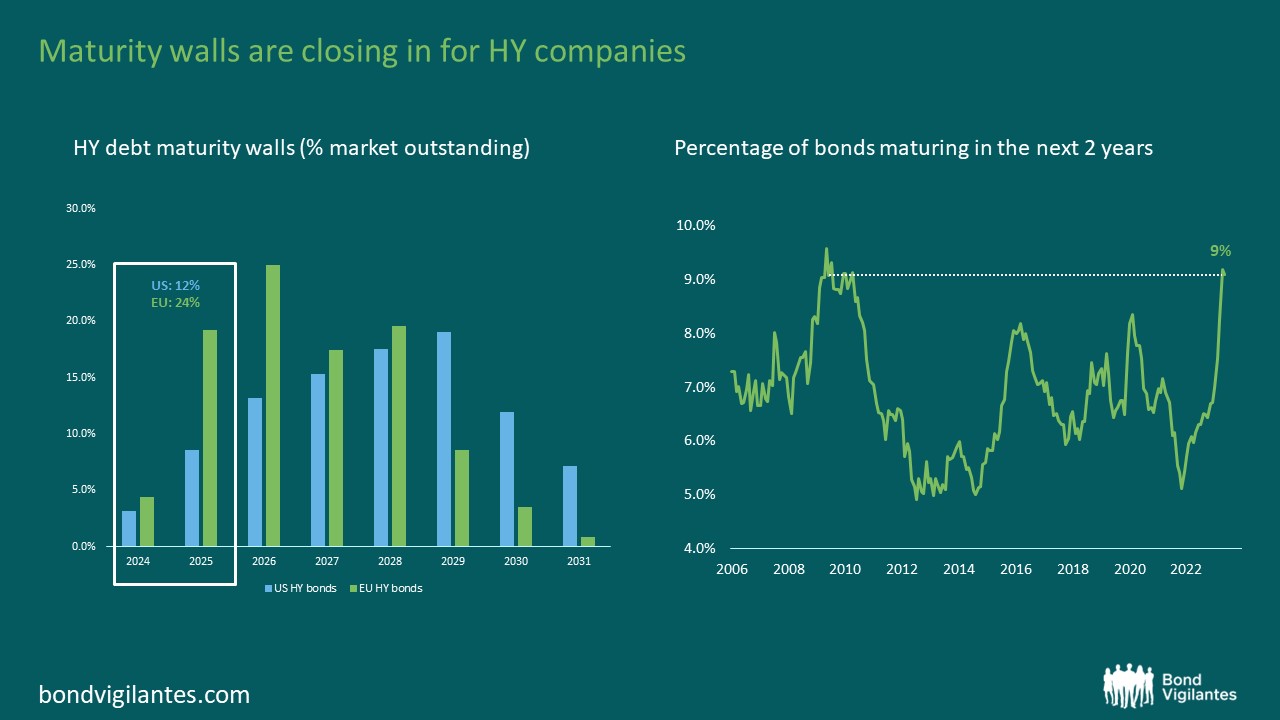

We are now 18 months into the Fed’s tightening cycle and many market participants, including us, have been surprised by the resilience of credit spreads, particularly in the high yield (HY) market where the option-adjusted spread for the Global HY index has dipped to the low 400s (bps), one of the tightest levels of post Global Financial Crisis observations.

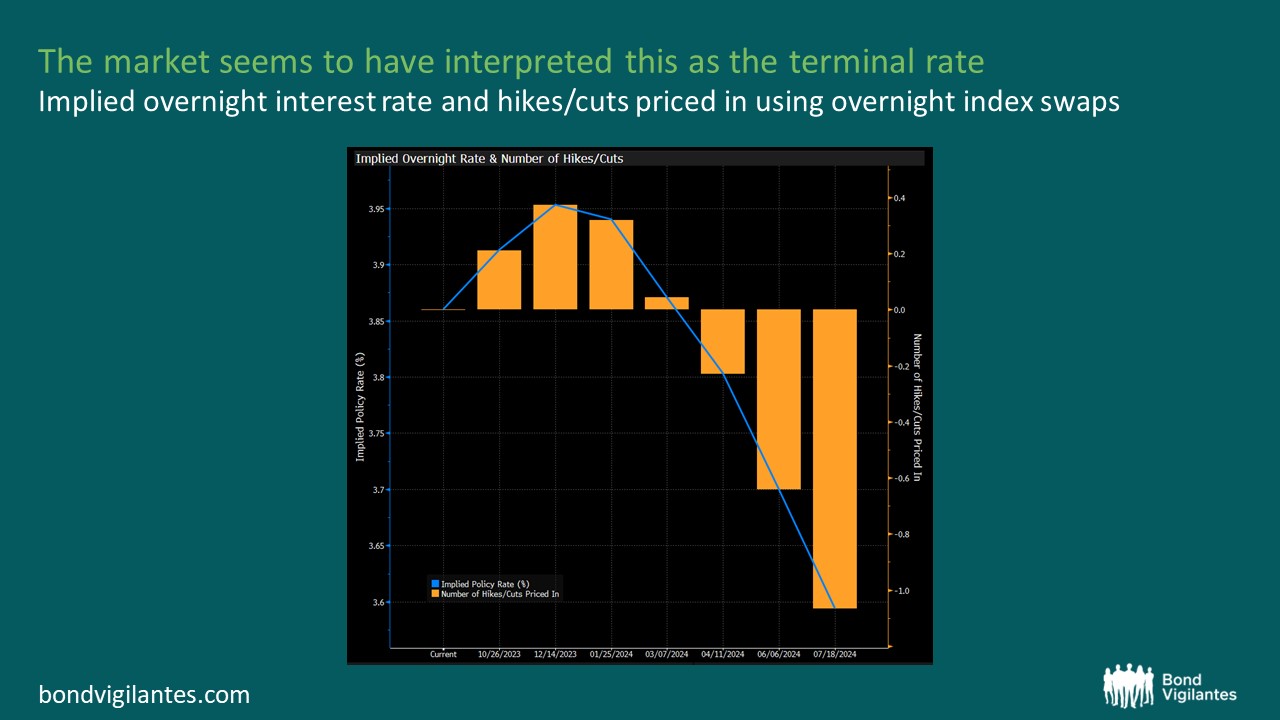

Has the ECB just delivered its final rate hike of the cycle?

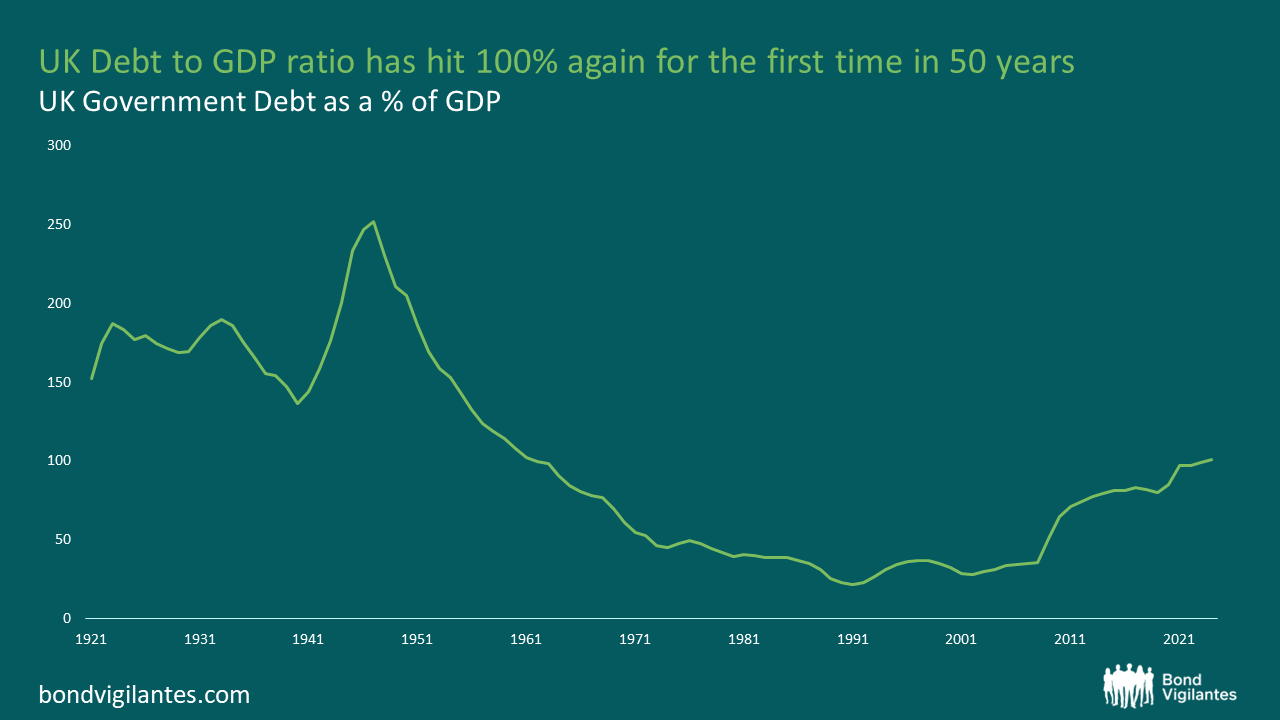

The current state of UK Government Debt as of 2023 is circa £2.5 trillion, which is 100% of GDP and equates to £38,000 per person.

An inverted yield curve refers to a situation in which short-term interest rates are higher than long-term interest rates for government bonds of the same credit quality. Inversion is considered unusual because, under normal circumstances, longer-term bonds tend to have higher yields than shorter-term bonds.

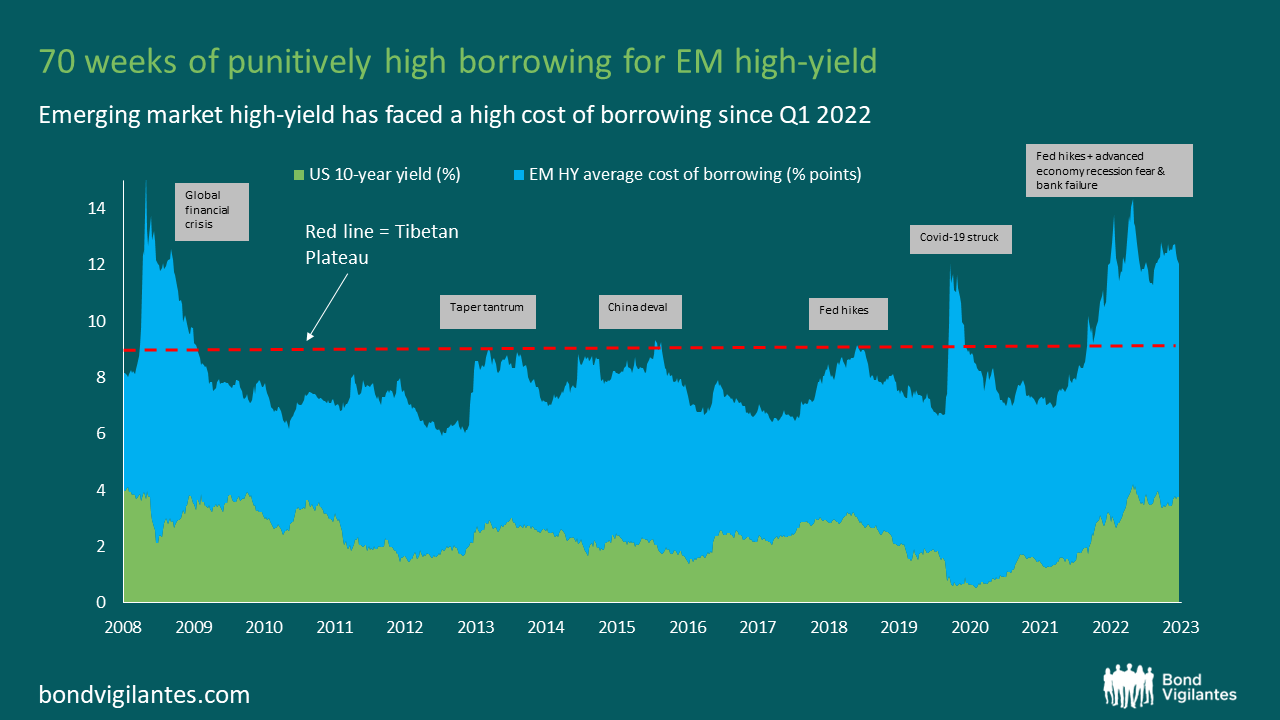

During this Fed hiking cycle emerging markets have been split into two camps.

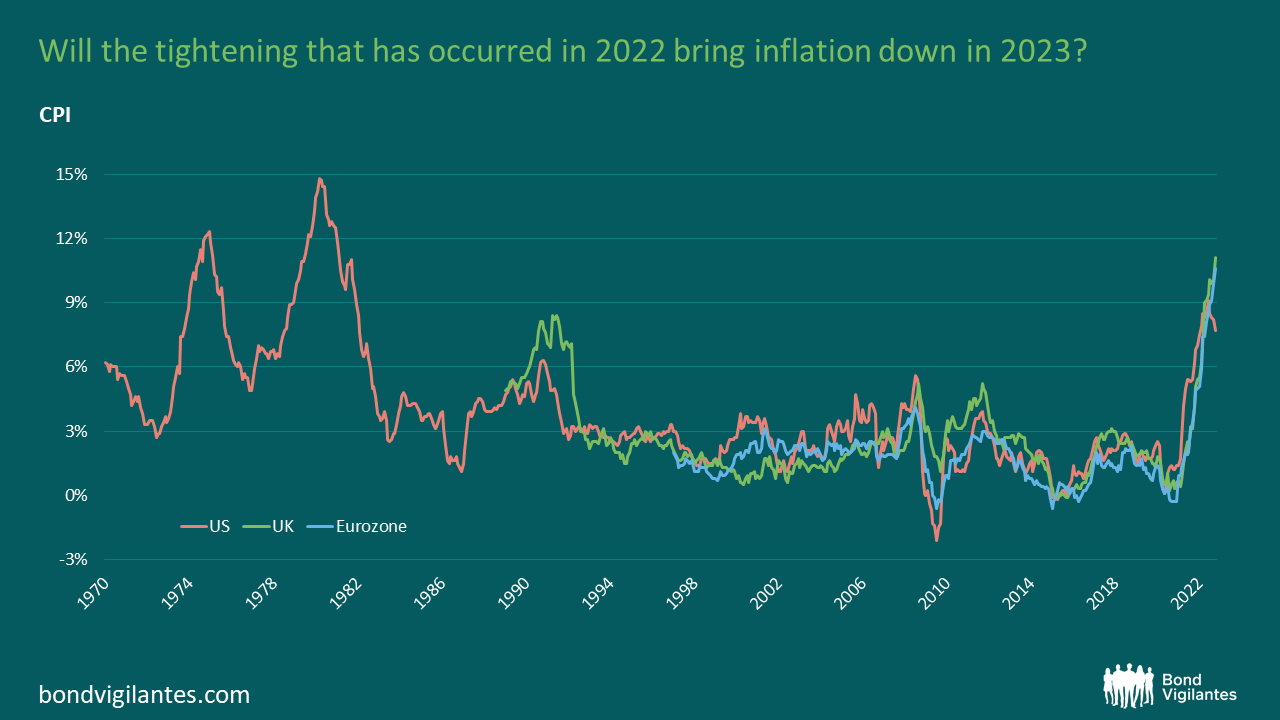

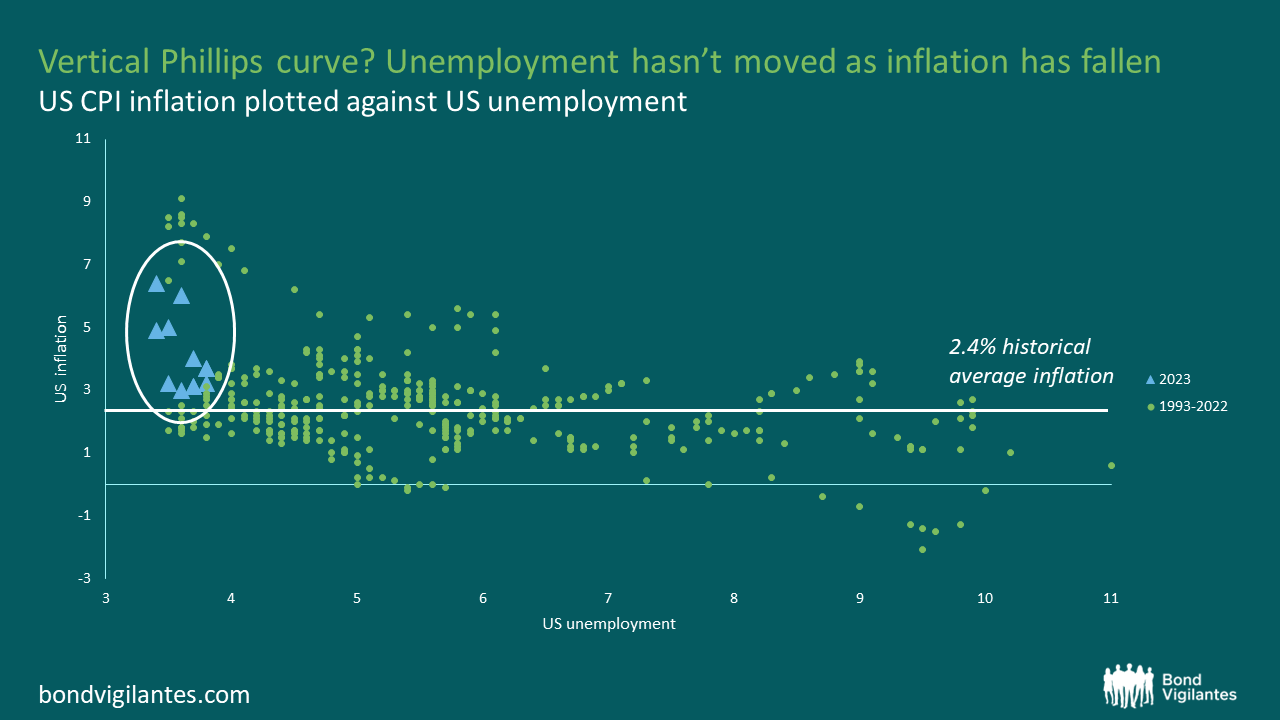

Inflation is one of the great economic debates and often leaves big economic thinkers at loggerheads. I am not a financial titan, but looking at the world from 100,000 feet, the conditions are in place for the world to see inflation heading meaningfully lower.

For a long time, it has made no sense to keep money under your mattress or invested in cash-like instruments (short dated, fixed return) such as money market funds, without facing an inflation-adjusted loss.

A brief press release recently from Europe’s largest and possibly oldest industrial manufacturer, announcing a short-dated, small-sized bond, seems hardly significant. In time however it may come to be seen as heralding a transformation of bond markets.

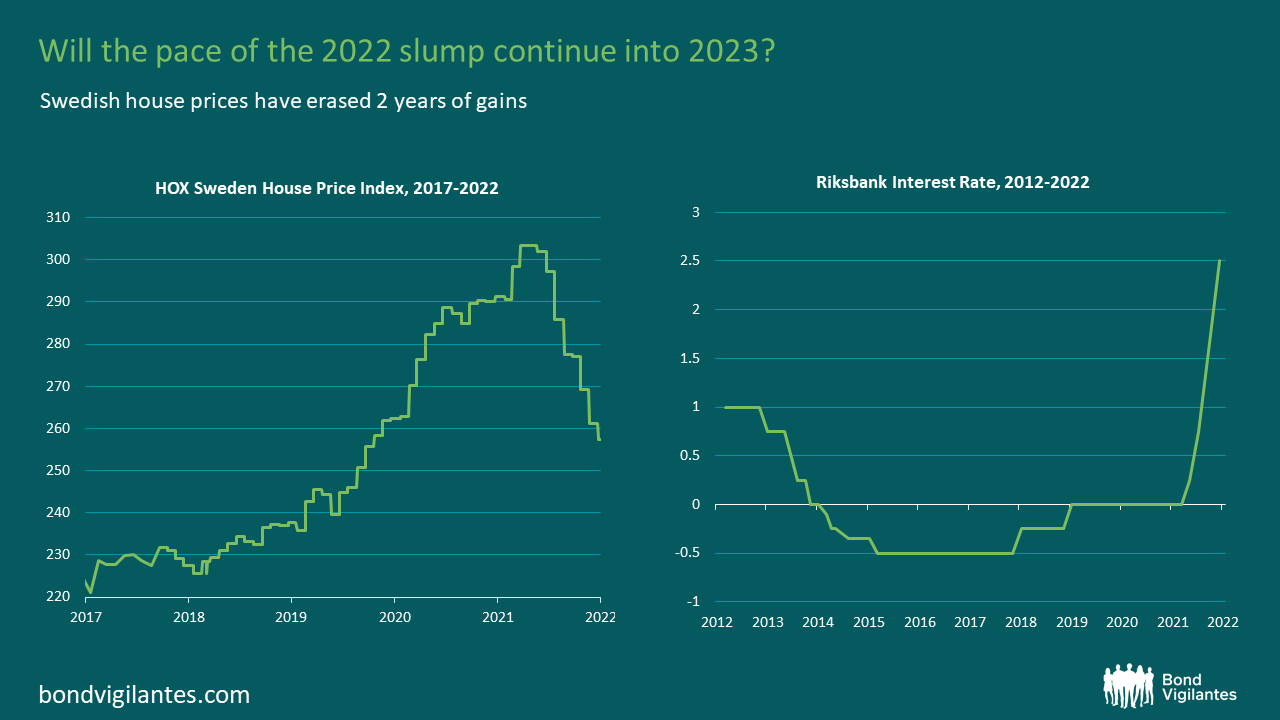

Real estate downturns (defined as two consecutive quarters of falling prices) have been triggered in a number of economies including Canada, Australia, New Zealand and the Nordics. One area where this trend is playing out most rapidly is Sweden, where house prices are falling at one of the fastest rates in the world.