The United Kingdom’s Government debt interest payments have been a topic of concern and scrutiny for many years. As one of the world’s largest economies, the UK has amassed a significant amount of debt, and the cost of servicing this debt has important implications for the nation’s fiscal health.

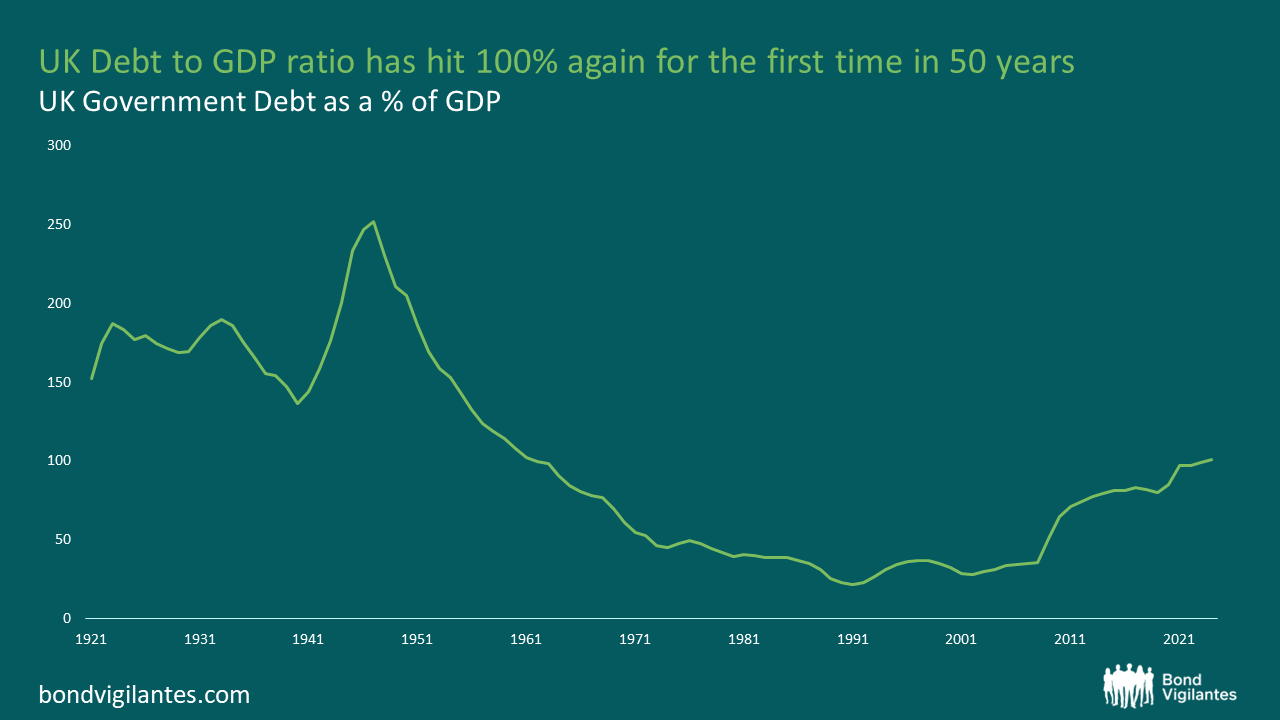

The current state of UK Government Debt as of 2023 is circa £2.5 trillion, which is 100% of GDP and equates to £38,000 per person.

Source: ONS (July 2023)

Source: ONS (December 2022)

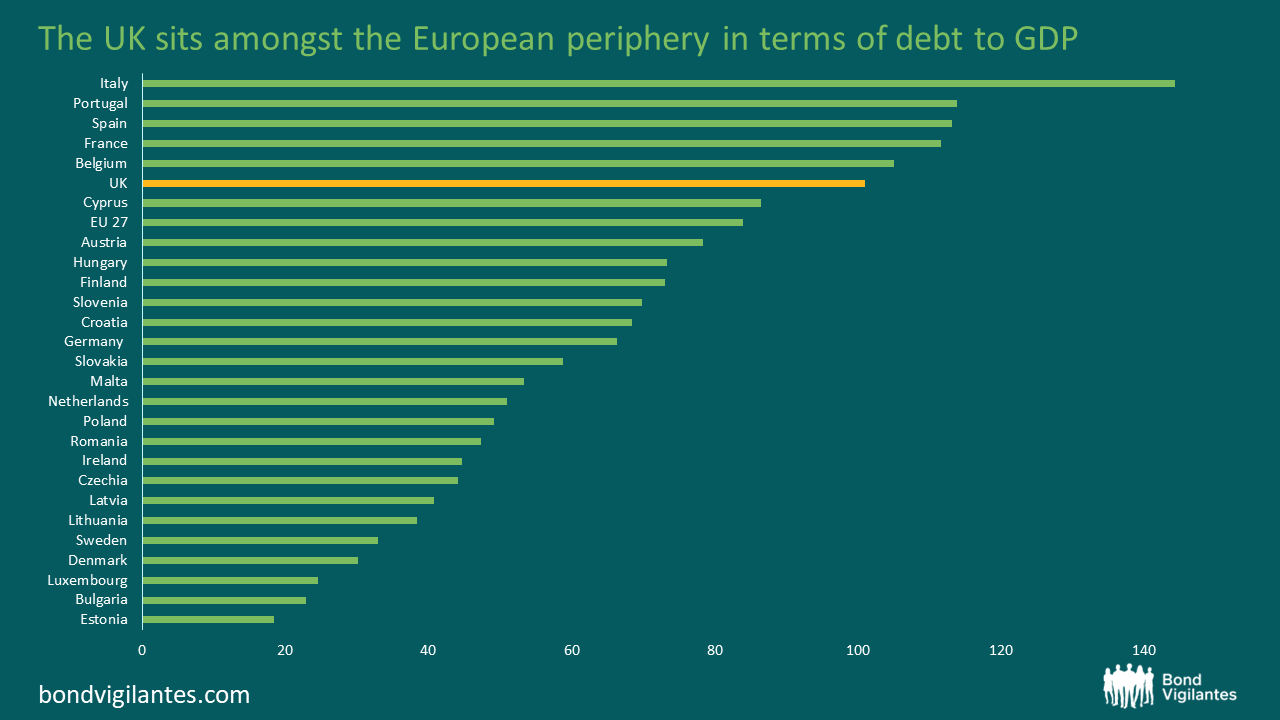

On a comparative basis, the UK is not the worst, but is sitting in amongst the likes of Italy, Portugal and Spain, which were embroiled in their sovereign debt crises only a few years ago. Although the crisis was the result of a number of factors, debt sustainability was the central cause.

Debt has accumulated and accelerated since 2008 through various channels, including government borrowing to fund budget deficits, economic stimulus measures, infrastructure projects and social spending. The low-interest rate environment since the 2008 global financial crisis has masked this growing problem and has helped keep debt servicing costs relatively manageable.

However, there is no sign of the low-interest rate environment returning anytime soon. So, this begs the question: are the chickens finally coming home to roost?

There are three key factors which are set to make the debt burden increasingly costly to service and maintain.

Source: OBR (July 2023)

It’s vital that the Government gets on top of the ever expanding mountain of debt. As this grows the economy becomes increasingly exposed to changes in interest rates and inflation.

Rising interest payments and the knock-on costs of these have subsequent impacts in the wider economy. Further action from the Government may also be necessary. Some measures may include the below:

The Government needs to manage these rising debt interest costs seriously, as they could very well start to drive policy.

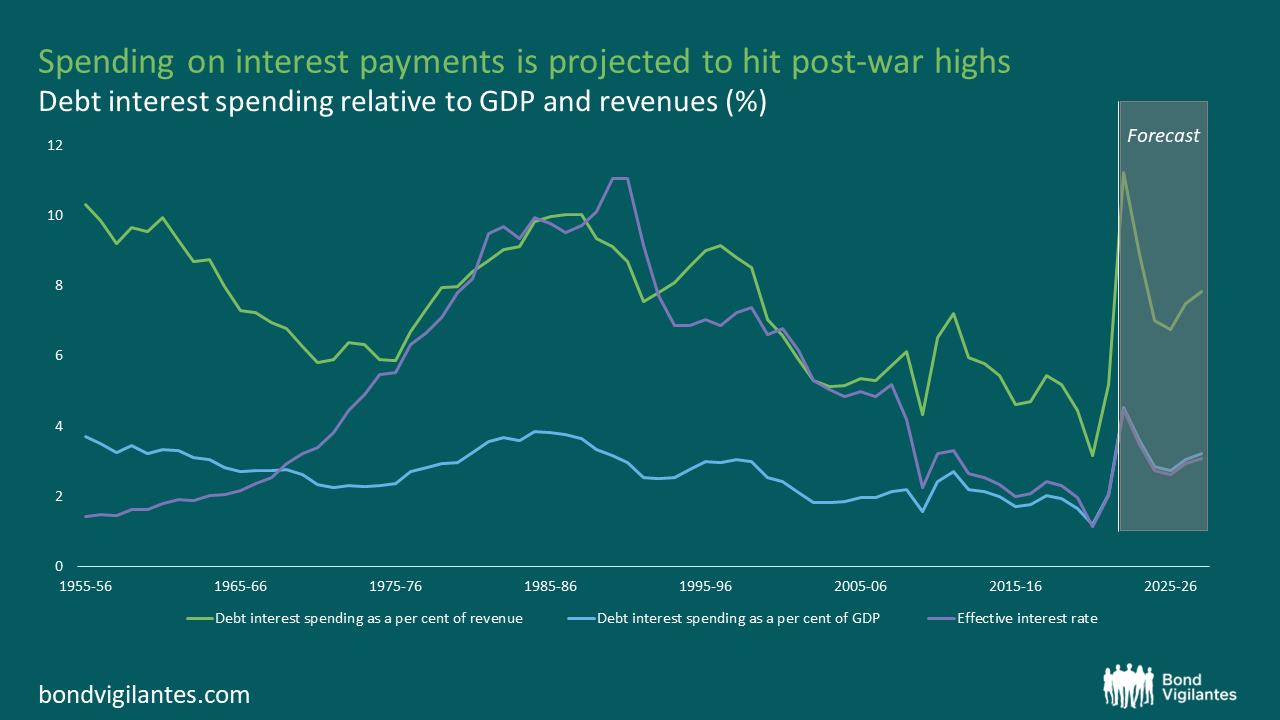

The below chart shows debt interest spending relative to GDP and revenues. This figure is projected to get to its highest since the post-war period over the coming 5 years.

Source: ONS, OBR (March 2023)

Let’s look at the two components of the debt interest spending-to-revenue measure and try to understand how the UK can get on top of this worrying trend.

Revenues are broadly a function of Taxes – Income, Corporation and VAT.

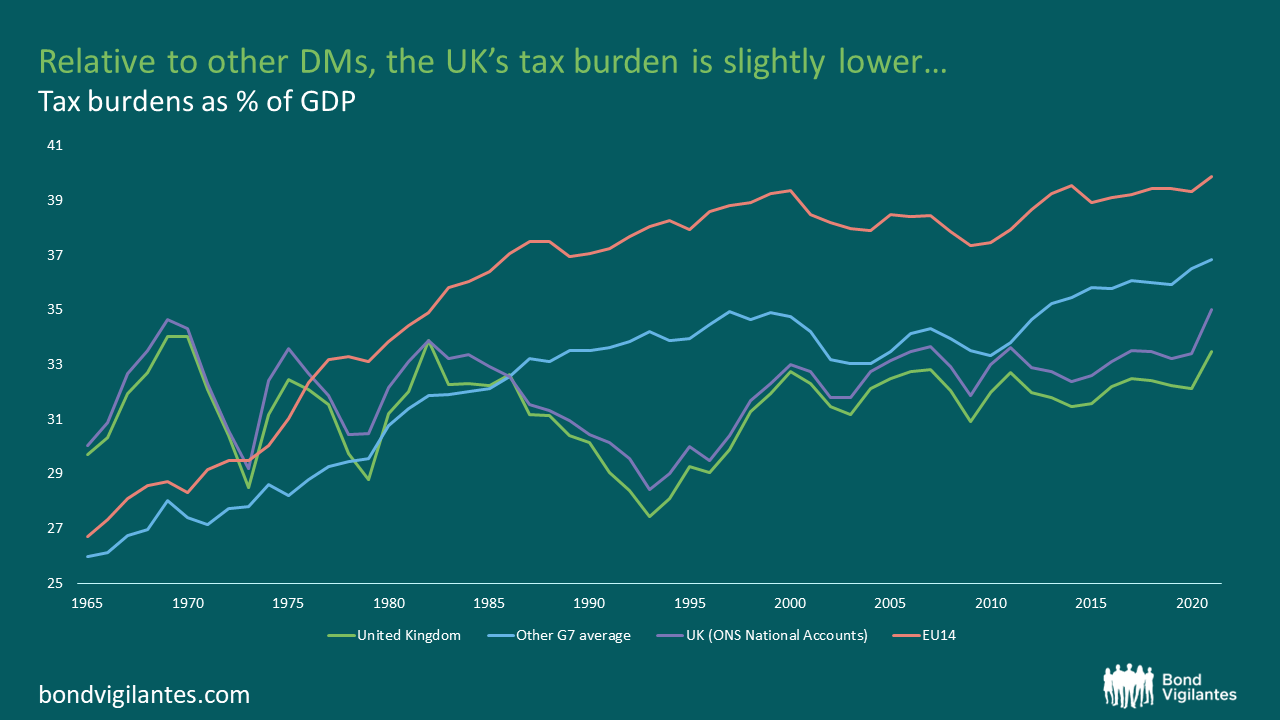

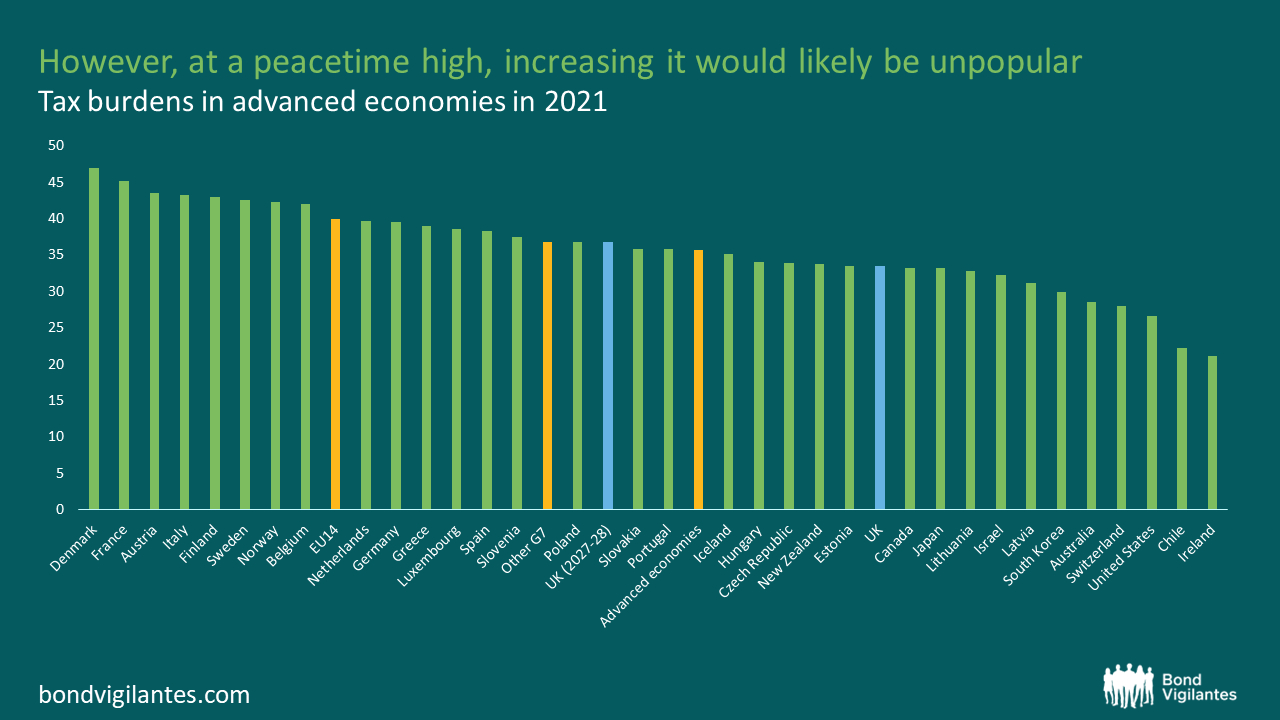

The chart below compares the UK’s long-term tax burden to other countries. Clearly, the UK is below some of its peers, suggesting there is scope to increase taxes. However, the level is currently at a peacetime high. It’s difficult to see taxes going up meaningfully from here. Let’s assume we are at or close to the maximum tax-generating point. Increasing tax revenue from here runs a real risk of slowing the economy further and is likely politically unpopular. Unless a tax increase is met with a meaningful improvement in Government services, it will be met with hostility. Equally, cutting taxes to spur growth is similarly difficult. We saw what happened when Kwasi Kwarteng tried to cut taxes to stimulate growth. The aptly names bond vigilantes were out in force and swiftly ended that agenda as investors lost confidence in the UK economy. Future Governments are going to be forced to demonstrate fiscal responsibility.

Source: OECD (March 2023)

Source: OECD, OBR (March 2023)

The various reasons for increasing debt interest payments have been discussed previously, but let’s take a minute to look at the various pressures here.

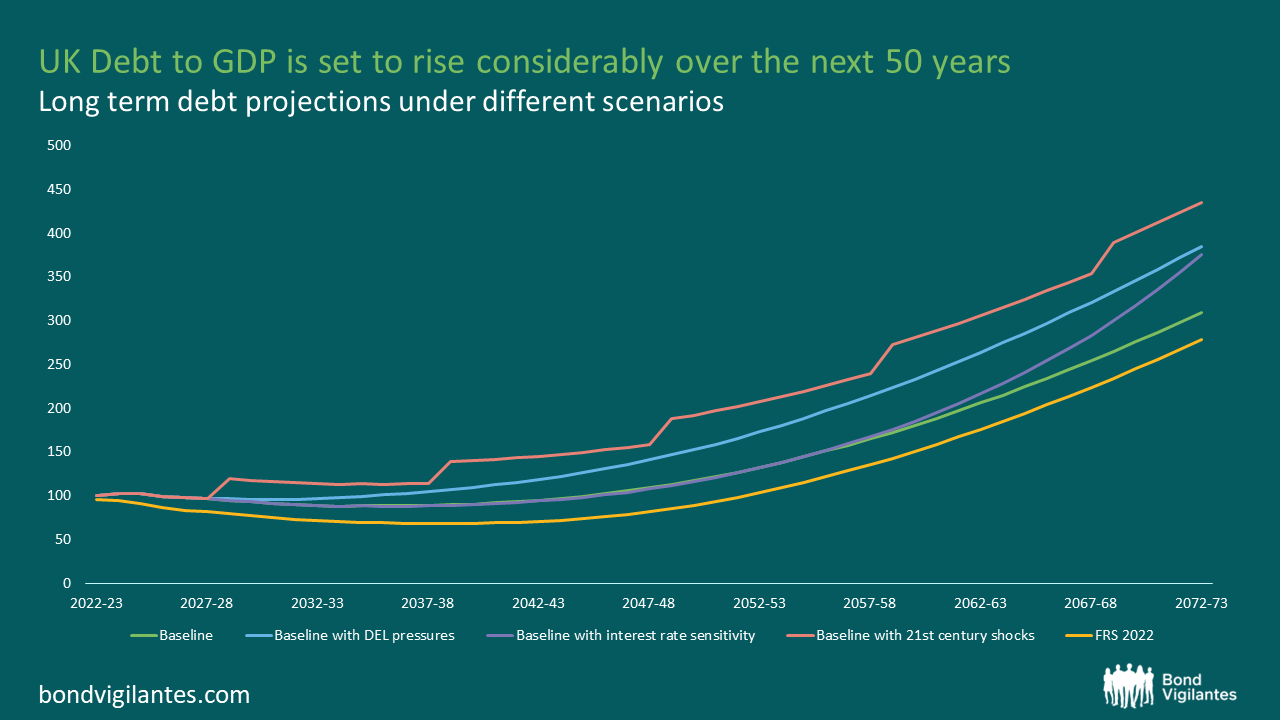

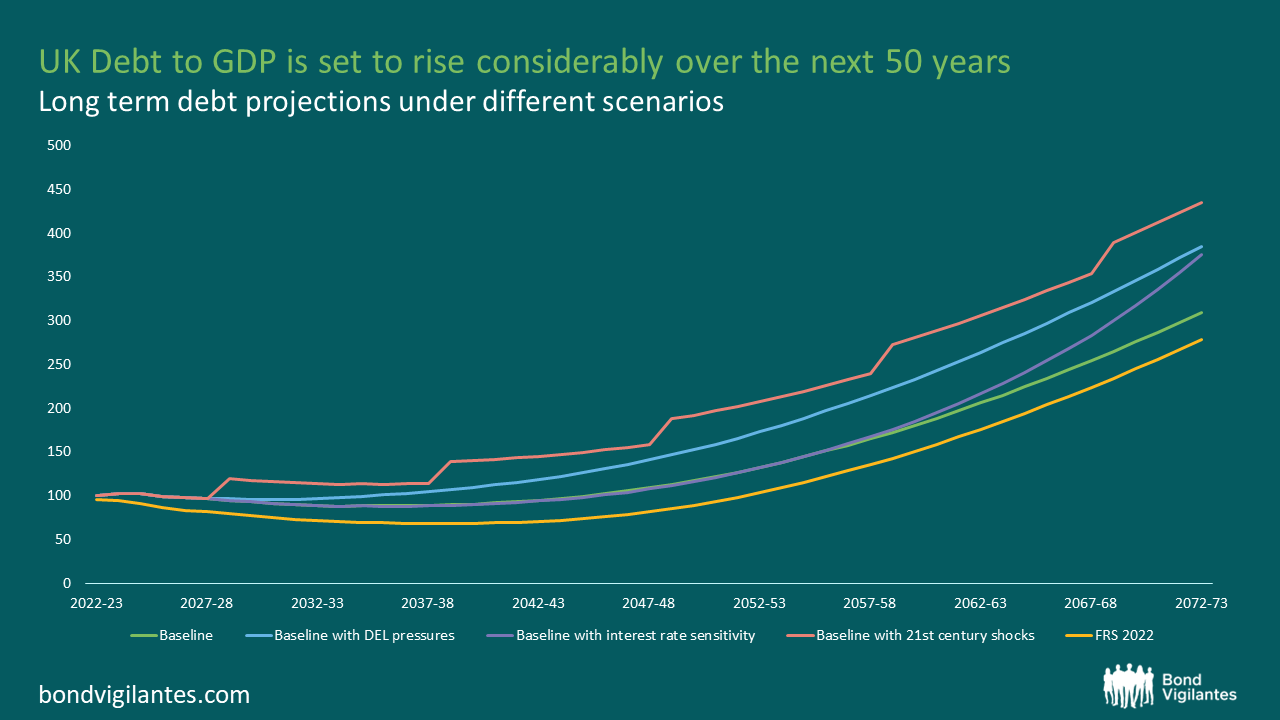

The chart below shows a long-term debt projection under various scenarios from the OBR; what is clear is that it’s going up, not down, under all scenarios. In fact, the OBR has projected that issuance for the next 5yrs is projected to be £1.1 trillion. That is almost half the entire stock of outstanding debt. Who is going to buy it, and at what level?

Source: OBR (July 2023)

Interestingly, the UK has the benefit of having the longest average debt maturity profile, amongst developed nations, of circa 14yrs. This means that rolling over debt at higher interest rates will take longer to feed through relative to a country that has a lower average maturity profile, like the US, which is circa 8yrs—a slight positive in that respect. However, the makeup of this debt is also important.

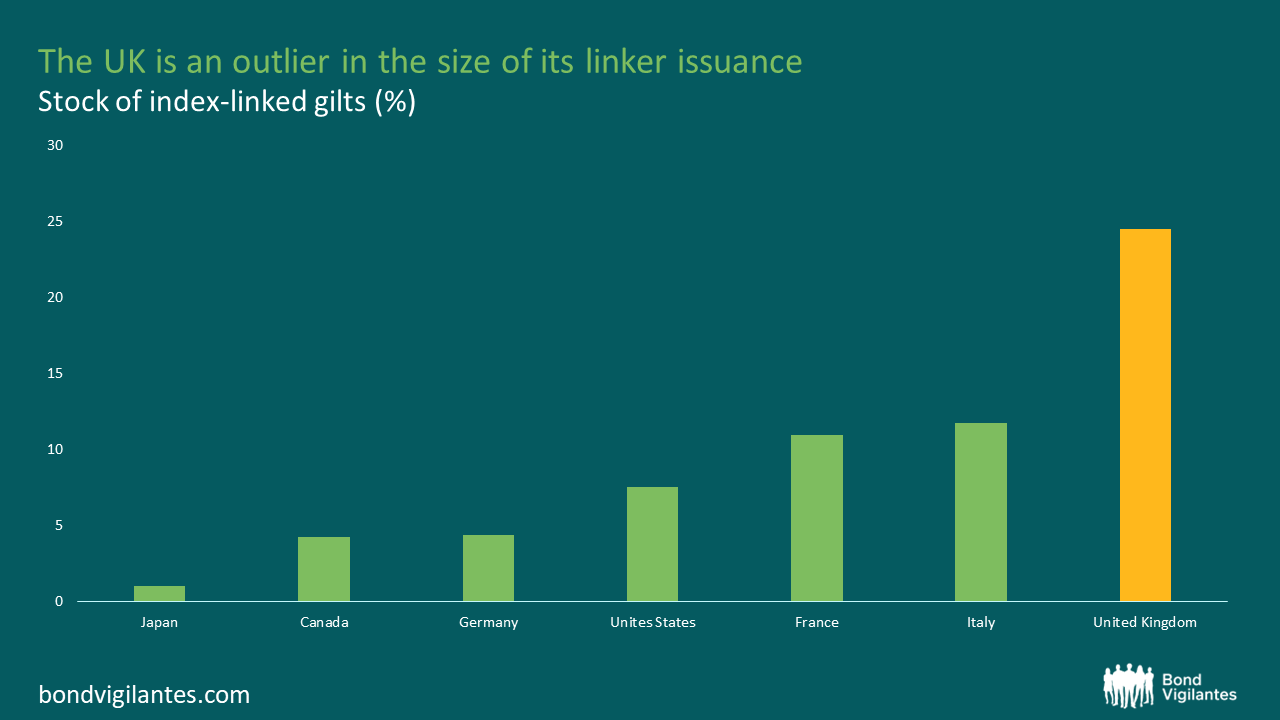

Inflation will erode debt as nominal GDP grows and existing outstanding fixed debt becomes smaller as a percentage of GDP. This can be a positive for those with a high proportion of fixed debt and an extended debt maturity profile. However, the UK has a relatively large proportion of inflation-linked debt as a percentage of total debt. As a result of inflation, the debt interest cost of inflation-linked bonds will rise in tandem, limiting this benefit. The UK has circa 25% of its debt linked to inflation, whereas Germany and US have circa 5% and 8%, respectively.

Source: Bloomberg (August 2023)

The UK’s Debt Management Office has made meaningful inroads in reducing this weighting over the last few years, but more needs to be done to limit the impact on debt interest payments when inflation spikes. The issuance of index-linked bonds can be a double-edged sword. If you issue index-linked bonds, you send a message to investors that you are serious about controlling inflation. If not, the opposite can be true.

However, if you have issued a high proportion of index-linked bonds and inflation materialises, the Government does not have the benefit of inflation eroding the debt stock.

The UK Government’s debt interest payments are poised to rise in future years to worrying levels due to factors such as rising debt levels, interest rate increases, and inflationary pressures. This will undoubtably weigh heavy and Government will face severe challenges in managing its fiscal priorities while servicing the ever growing debt. Striking a balance between addressing the debt burden and supporting economic growth will be critical for policymakers in the coming years.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

For Investment Professionals only. Not for onward distribution. No other persons should rely on the information contained within this blog. This blog provides commentary and views on bond markets. Prepared by M&G’s bond team, this information is aimed at investment professionals wishing to supplement their understanding of these markets. Information shown on the blog should not be taken as advice or a recommendation to make an investment decision.

This weblog does not represent the thoughts, intentions, plans or strategies of M&G plc or any associated companies. They are solely the author’s personal opinion.

Inappropriate comments will be deleted or edited at the author’s discretion.

This blog may contain, or be linked to, advice or statements from third parties. M&G make no representation as to the accuracy, completeness, timeliness or suitability of such information and we have not, and will not, review or update such information and caution you that any use made of such information is at your own risk. Some of the information contained on this blog may also have been prepared or provided by third parties and may not have been verified by us. M&G hereby exclude any liability arising out of any preparation or provision of such information for this blog and make no warranty as to the accuracy, suitability or completeness of any such information.

With the exception of iviewtv.com, the links we provide from this blog to other websites are provided for information only. We do not assume any responsibility or liability with respect to any website accessed via our blog. We do not monitor or review any of the websites accessible through these links. Once you have used these links to leave this blog you should note that we do not have any control over that other website. We therefore cannot be responsible for the protection and privacy of any information that you provide whilst visiting such websites and such websites are not governed by our Terms & Conditions. You should exercise caution and look at the privacy statement applicable to the website in question.

The presence of any advert on this blog is not an endorsement by M&G of the goods, services or website advertised.

No liability is assumed for any use, or misuse, of the information presented on this blog.

As you are probably aware, internet email cannot be guaranteed and is not secure. We recommend that you do not send any confidential information to us by email. If you choose to send any confidential information then you do so at your own risk. Instructions sent by you via email, and to this blog, are processed exclusively at your risk.

Whilst M&G uses every reasonable effort to maintain the availability of this blog we cannot guarantee this. This blog may also change from time to time and we cannot guarantee the continuation of the services offered through it.