Higher real rates in the coming years might favor value stocks

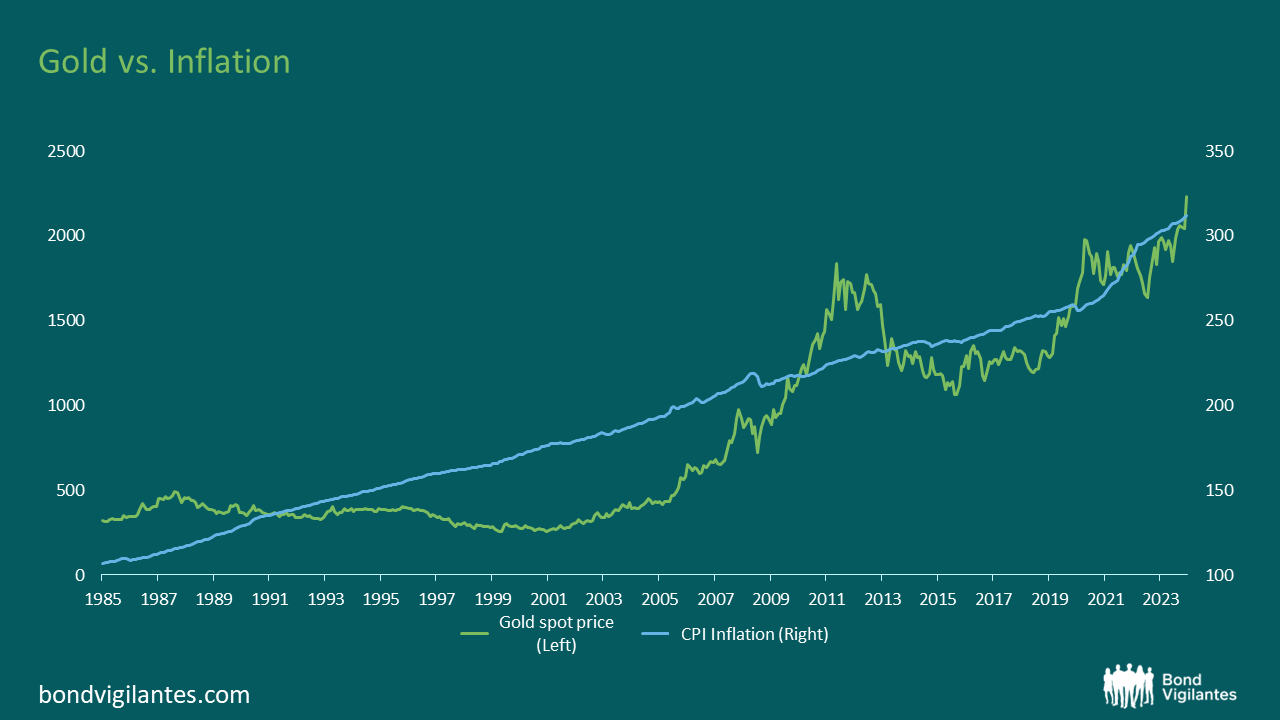

Renowned for its role as a hedge against economic uncertainty and inflation, gold has long captivated investors. One key factor influencing gold’s price is the relationship between real yields and inflation. Over the long term, gold has protected one against the pernicious effects of inflation and remains a powerful diversifier within an investment portfolio:

The yield curve in Japan is reaching intriguing levels. The Bank of Japan (BoJ) has remained resolute, maintaining an ultra-accommodative monetary policy in a world aggressively hiking interest rates to stem inflation.

What’s more, if you’d taken a 12 month sabbatical through 2023, spent on a desert island listening to the Smiths and the Velvet Underground, then upon firing up your Bloomberg on New Year’s Day, what would be most surprising of all, is that none of this uncertainty is visible in markets.

A focus on bond yields, the Magnificent 7, and the Fed pivot

Every year, the largest banks, asset managers and consulting firms publish their economic and market outlooks for the following year, highlighting key topics, trends, opportunities and areas of concerns. For the first time, we have used ChatGPT to skim-read through and summarize 48 of these outlook presentations and built a database, containing the various opinions expressed in the the areas that are traditionally of interest to our clients and us.

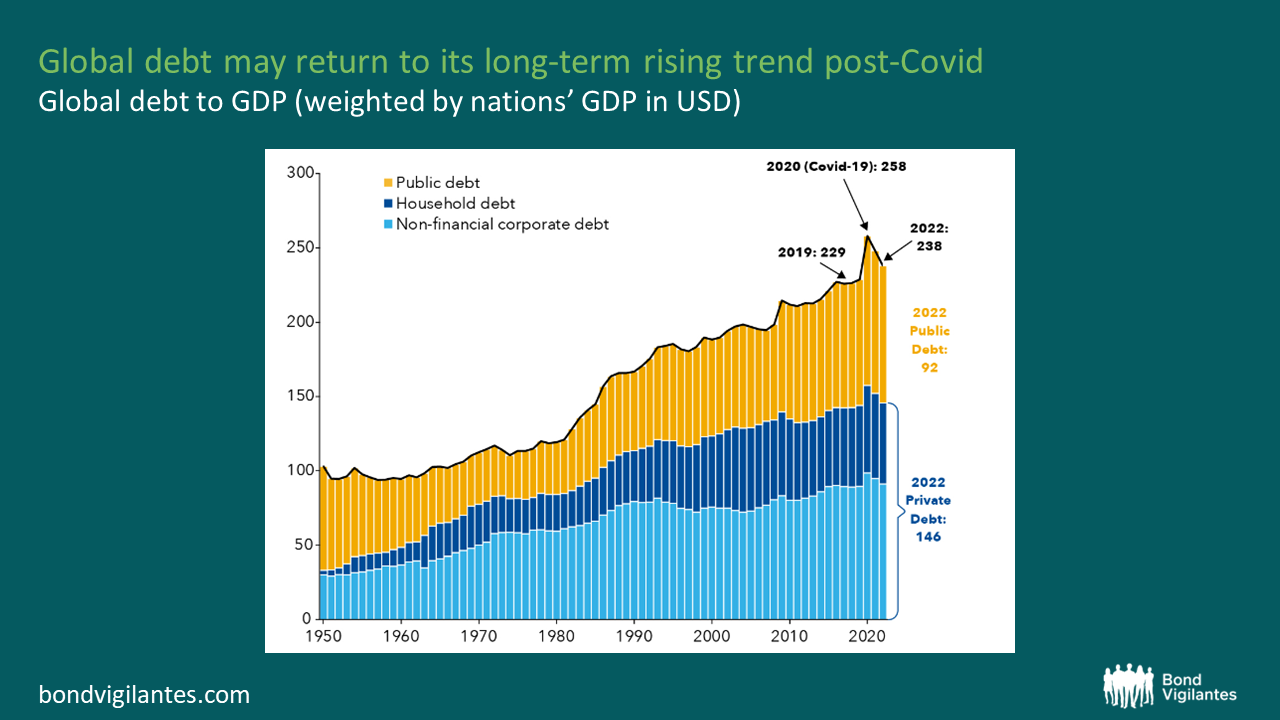

Governments have traditionally argued that as long as debt remains manageable and serviceable without difficulty, there’s little cause for concern. While this notion holds some truth, the reality is that recent growth has largely been fueled by an insurmountable increase in debt.

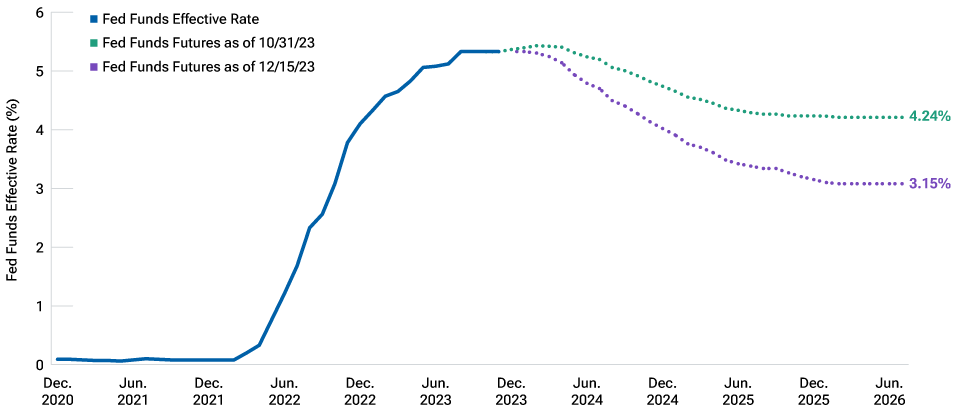

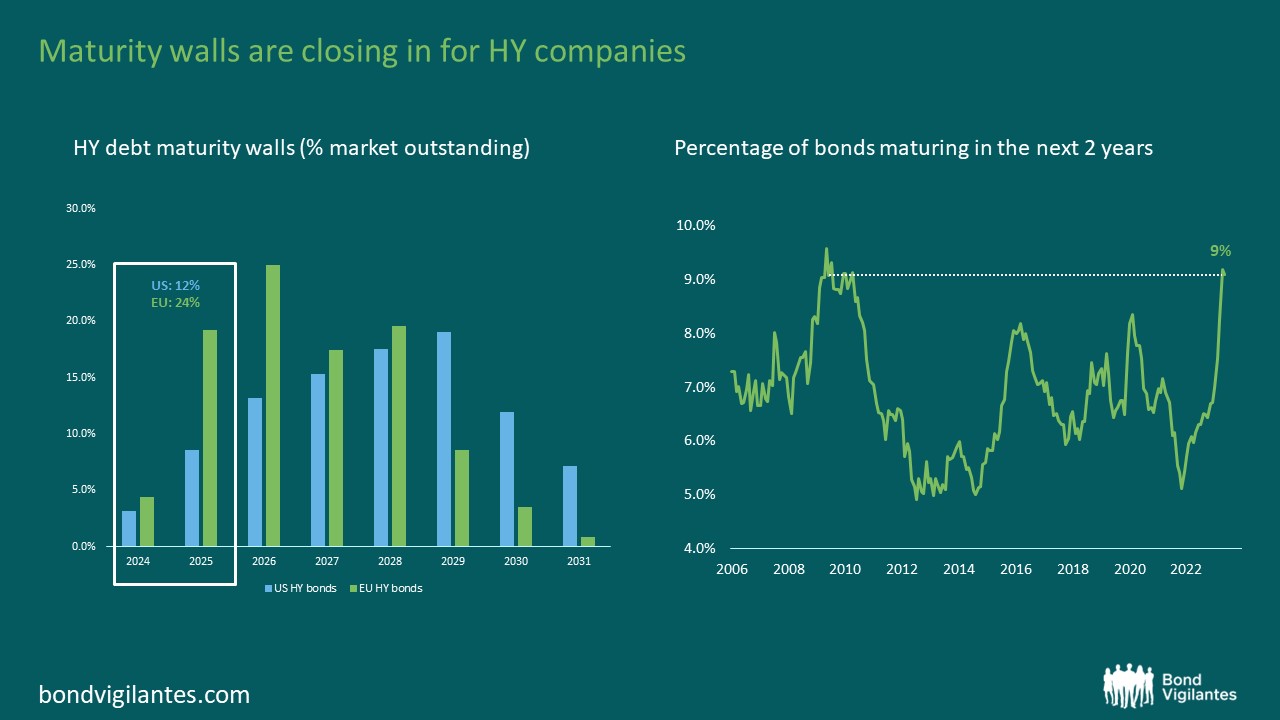

We are now 18 months into the Fed’s tightening cycle and many market participants, including us, have been surprised by the resilience of credit spreads, particularly in the high yield (HY) market where the option-adjusted spread for the Global HY index has dipped to the low 400s (bps), one of the tightest levels of post Global Financial Crisis observations.

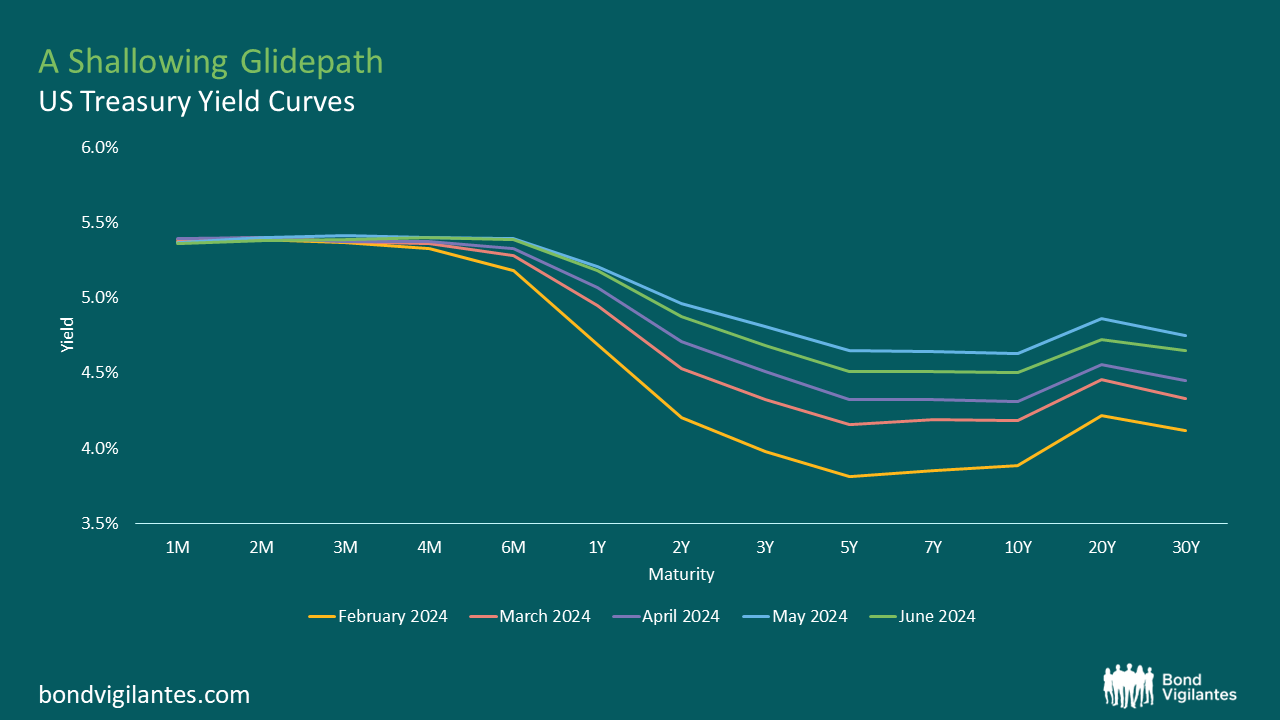

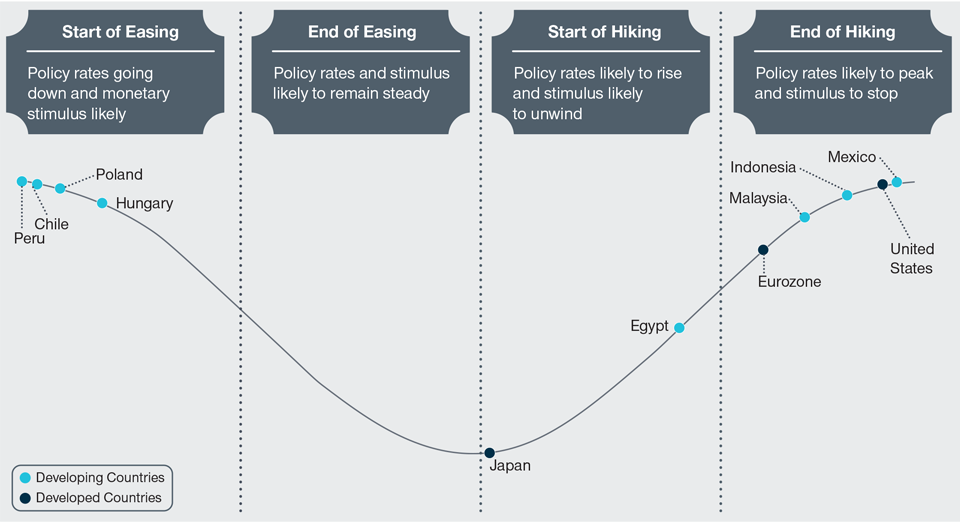

Central banks set to kick off easing cycles as inflation cools