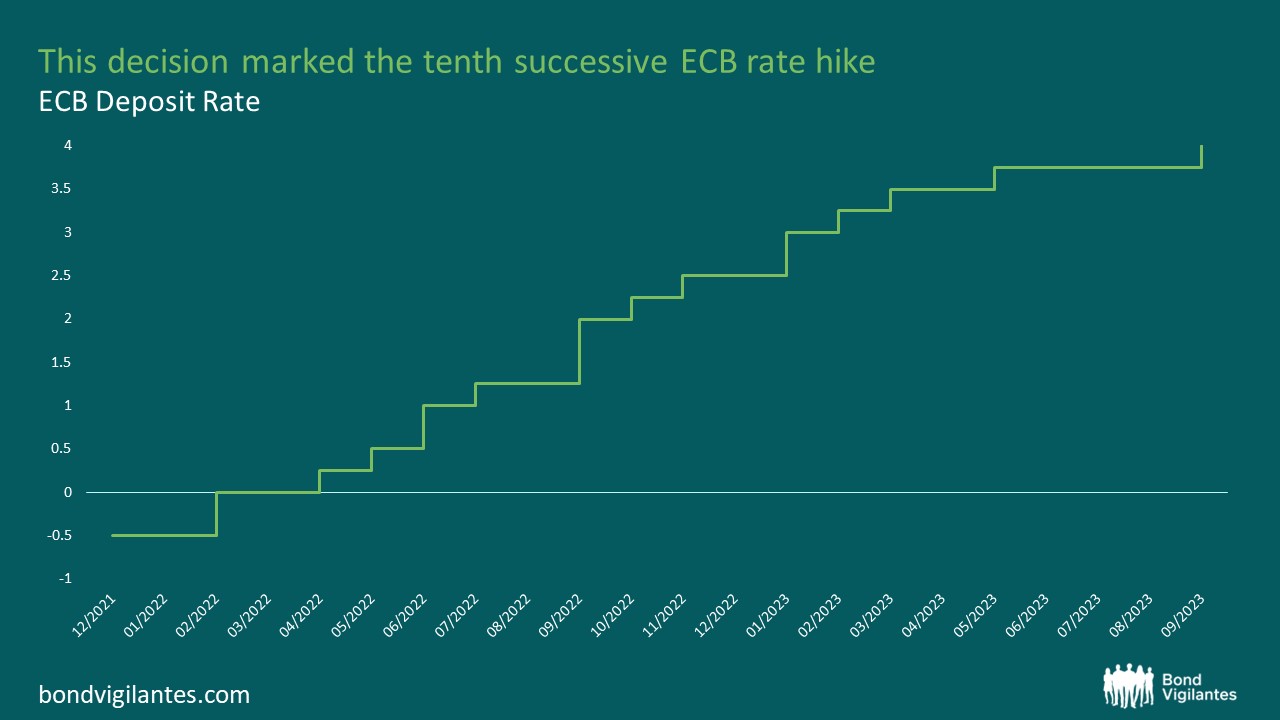

Against the backdrop of stubbornly high – albeit receding – European inflation, the ECB’s Governing Council decided yesterday to raise its policy rates by yet another 25 basis points. This marks the tenth consecutive hike and lifts the ECB’s deposit rate, which had been at -0.5% only in mid-2022, to a whopping 4%. The burning question on many investors’ minds is, of course, was this the final hike of the cycle?

Source: Bloomberg (15 September 2023)

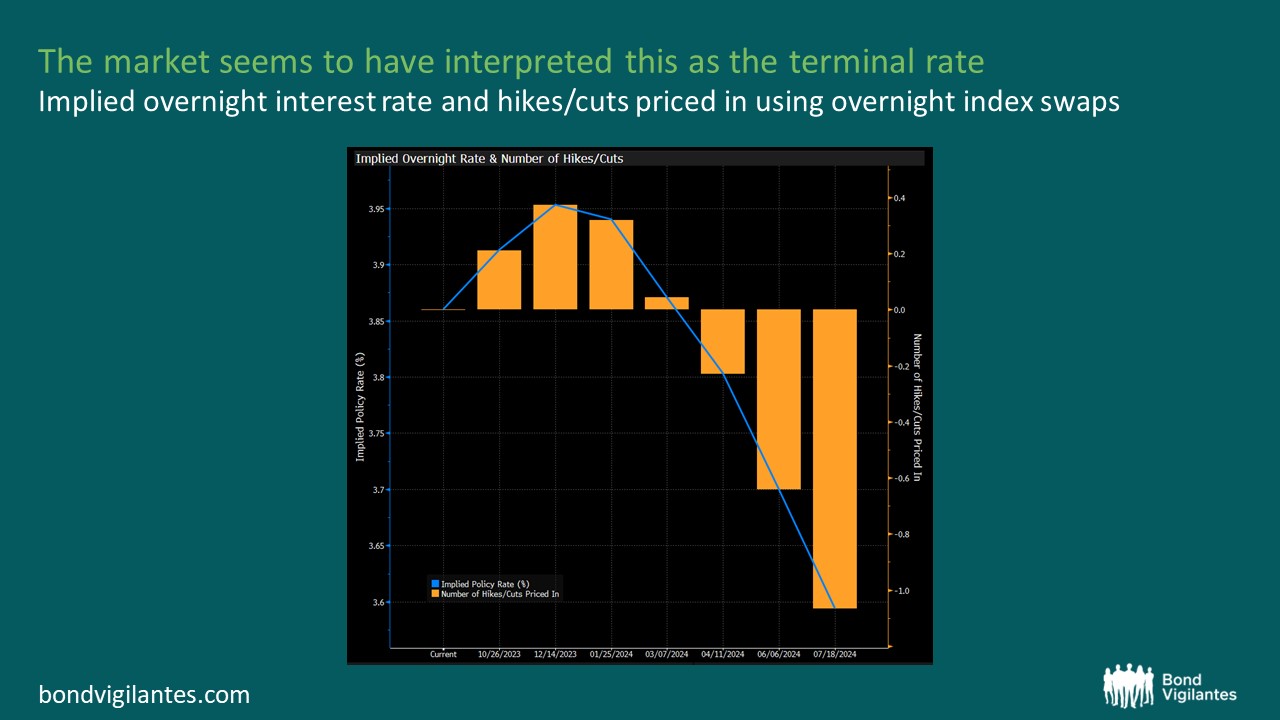

The answer is most likely yes. Admittedly, ECB President Lagarde carefully avoided any definitive statement. Otherwise, she would have needlessly given up optionality. But the passage, “key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target” in the official press release is probably as explicit as it gets in the world of intricate central bank speak. Unless European inflation stages an unexpected resurgence, the ECB has reached its terminal rate. That’s how bond markets interpreted the ECB’s decision, which was widely regarded as a “dovish hike”, sending bond yields lower across the board.

Source: Bloomberg (15 September 2023)

There are two good reasons for the ECB to take the foot off the gas. Firstly, it is estimated that it can take up to 18 months before the economic impact of interest rate decisions is actually felt. With European core inflation beginning to ease off, it might be prudent for the ECB to pause and observe the effects of its ten consecutive rate hikes unfolding over the coming months. Secondly, the macroeconomic outlook is getting noticeably bleaker. The ECB acknowledged that tightening financial conditions have dampened domestic demand in Europe. In combination with the weakening international trade environment, this has prompted the ECB staff to lower their economic growth projections significantly. Going forward, the euro area economy is expected to grow anaemically by 0.7% in 2023, 1.0% in 2024 and 1.5% in 2025. There is only a fine line between fragile growth and a “hard landing”, of course, a scenario which the ECB would like to avoid. Holding fire on rates for now might be the best course of action as delivering further hikes could push (parts of) the euro area into a recession.

If it’s really going to be all quiet on the rates front, what’s next for the ECB? I’d expect the focus to shift towards the asset purchase programmes. While I wouldn’t necessarily assume that actively selling bond holdings Bank-of-England-style will be seriously considered in Frankfurt, questions around reinvestments will continue to bubble up. As a reminder, the size of the ECB’s asset purchase programme (APP) portfolio is shrinking as, from July 2023 onward, the Eurosystem no longer reinvests the principal payments from maturing securities. This does not apply to the pandemic emergency purchase programme (PEPP), though. The ECB intends to carry out reinvestments of principal payments within the c. €1.7 trillion PEPP bond portfolio at least until the end of 2024.

Being asked about PEPP reinvestments at the ECB press conference yesterday, President Lagarde was quick to dismiss any speculations about a potential change of tack. And, from her point of view, a certain reluctance of scrapping reinvestments, which would shrink the PEPP’s size and importance, is understandable. Unlike the APP, which imposes strict capital key-based rules on how to allocate bond purchases across the euro area, the PEPP offers the ECB much higher degrees of freedom. Created against the backdrop of mounting pressures for the European periphery at the height of the Covid-19 pandemic, PEPP investments can, for example, be disproportionally directed towards peripheral bond issuers. If push comes to shove, the PEPP offers the ECB, in theory, enough flexibility and firepower to prevent the spread between peripheral and core European bonds from diverging beyond reason. In this sense, the ECB understands the PEPP as a spread management tool. It’s hard to let go of such a powerful instrument and see it slowly fade away by a discontinuation of reinvestments.

That being said, I still think the PEPP’s days are ultimately numbered. The dark days of the “pandemic emergency” – the clue is in the name – are long behind us. Carrying on with PEPP reinvestments feels like an anachronism. And it contradicts the ECB’s pivot away from an ultra-loose to a much tighter monetary policy stance in light of euro area inflation numbers running well above target, thus creating potential credibility issues. I, for one, would be surprised if PEPP reinvestments would really take place until the end of 2024.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

For Investment Professionals only. Not for onward distribution. No other persons should rely on the information contained within this blog. This blog provides commentary and views on bond markets. Prepared by M&G’s bond team, this information is aimed at investment professionals wishing to supplement their understanding of these markets. Information shown on the blog should not be taken as advice or a recommendation to make an investment decision.

This weblog does not represent the thoughts, intentions, plans or strategies of M&G plc or any associated companies. They are solely the author’s personal opinion.

Inappropriate comments will be deleted or edited at the author’s discretion.

This blog may contain, or be linked to, advice or statements from third parties. M&G make no representation as to the accuracy, completeness, timeliness or suitability of such information and we have not, and will not, review or update such information and caution you that any use made of such information is at your own risk. Some of the information contained on this blog may also have been prepared or provided by third parties and may not have been verified by us. M&G hereby exclude any liability arising out of any preparation or provision of such information for this blog and make no warranty as to the accuracy, suitability or completeness of any such information.

With the exception of iviewtv.com, the links we provide from this blog to other websites are provided for information only. We do not assume any responsibility or liability with respect to any website accessed via our blog. We do not monitor or review any of the websites accessible through these links. Once you have used these links to leave this blog you should note that we do not have any control over that other website. We therefore cannot be responsible for the protection and privacy of any information that you provide whilst visiting such websites and such websites are not governed by our Terms & Conditions. You should exercise caution and look at the privacy statement applicable to the website in question.

The presence of any advert on this blog is not an endorsement by M&G of the goods, services or website advertised.

No liability is assumed for any use, or misuse, of the information presented on this blog.

As you are probably aware, internet email cannot be guaranteed and is not secure. We recommend that you do not send any confidential information to us by email. If you choose to send any confidential information then you do so at your own risk. Instructions sent by you via email, and to this blog, are processed exclusively at your risk.

Whilst M&G uses every reasonable effort to maintain the availability of this blog we cannot guarantee this. This blog may also change from time to time and we cannot guarantee the continuation of the services offered through it.