We are now 18 months into the Fed’s tightening cycle and many market participants, including us, have been surprised by the resilience of credit spreads, particularly in the high yield (HY) market where the option-adjusted spread for the Global HY index has dipped to the low 400s (bps), one of the tightest levels of post Global Financial Crisis observations.

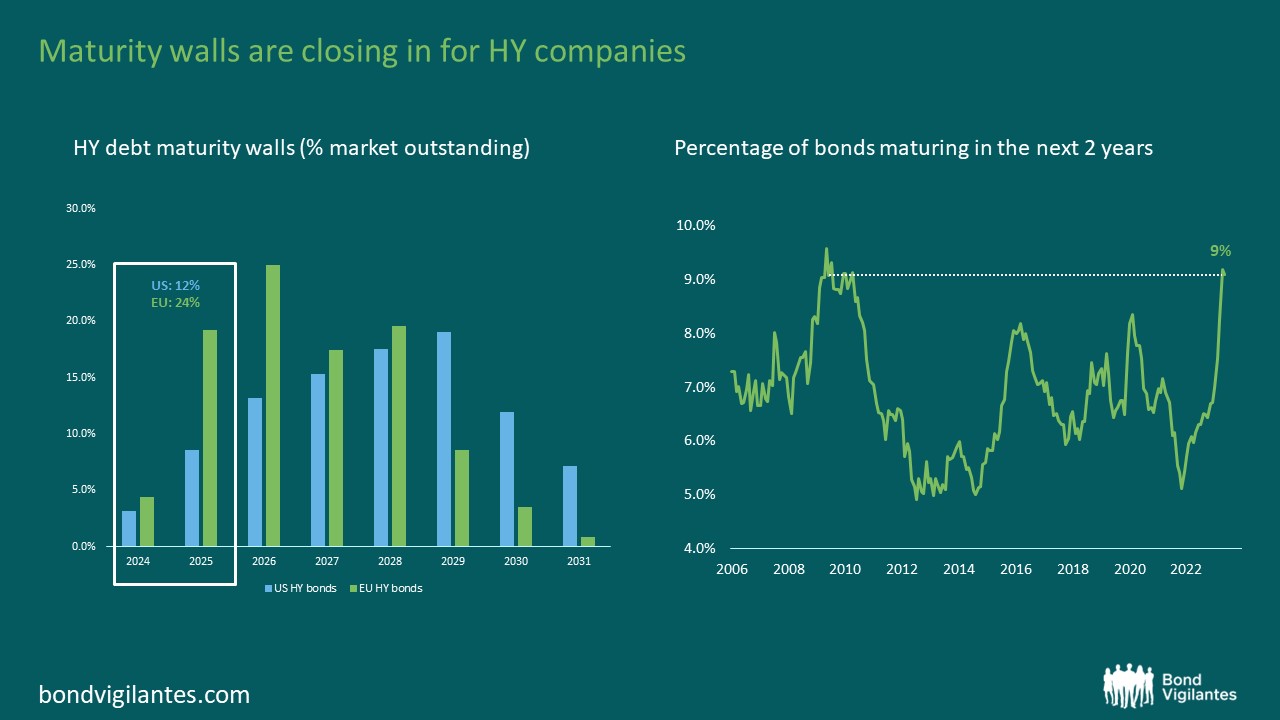

Two converging technical forces have supported HY credit spreads so far: a) the relentless hunt for yield in fixed income and b) a very light issuance calendar as companies have refrained from borrowing amid rising funding costs. Little refinancing in the last few years means maturity walls are now closing in for HY companies. The chart below shows the substantial amount of debt to roll over in the next 2 years with $127bn, or circa 12% of the market’s outstanding debt, being due for US HY companies. In Europe, maturity walls are even steeper, with €97bn of debt (23% of the index) maturing in 2024/2025. Add in 2026 maturities, and the refinancing wall shoots up to just to under 50% of the market. Historically speaking, this is likely to become the largest refinancing effort for HY issuers since the GFC (2008), and while some companies have already begun doing their homework, we expect it to become a key theme in 2024, particularly if base rates and borrowing costs remain elevated.

Source: Bloomberg, BofA Merrill Lynch, M&G (August 2023)

However, contrary to the GFC experience, there are a number of silver linings today that could well soften the impact of such a challenging refinancing environment.

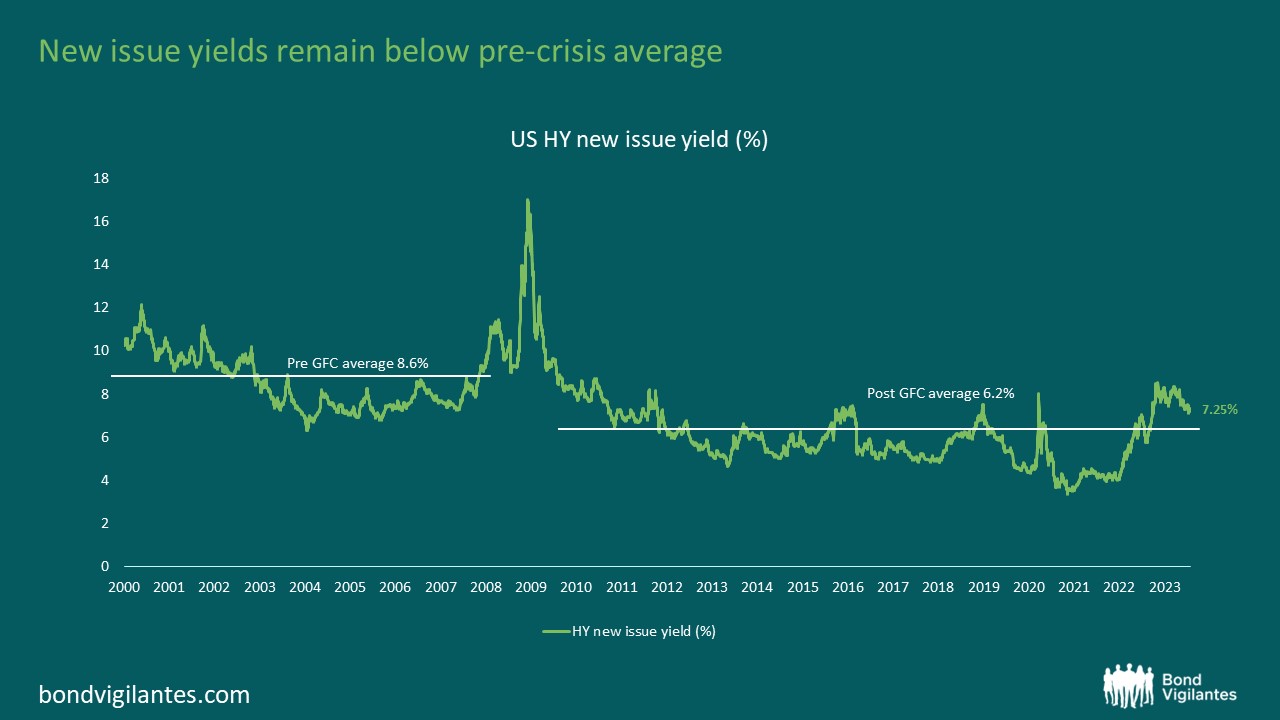

Firstly, as next chart shows, while the recent increase in borrowing costs over the last 18 months has been nothing but steep, new issue yields still remain well below the pre-GFC average. Put in historical context, yields have risen but from an extremely low base. Funding costs of 4-5% are arguably an exception in the recent history of high yield markets. Well-run companies with stable free cash flow (FCF), moderate leverage and healthy interest cover ratios may well be capable of affording the higher bill.

Source: Bloomberg, M&G (2 October 2023)

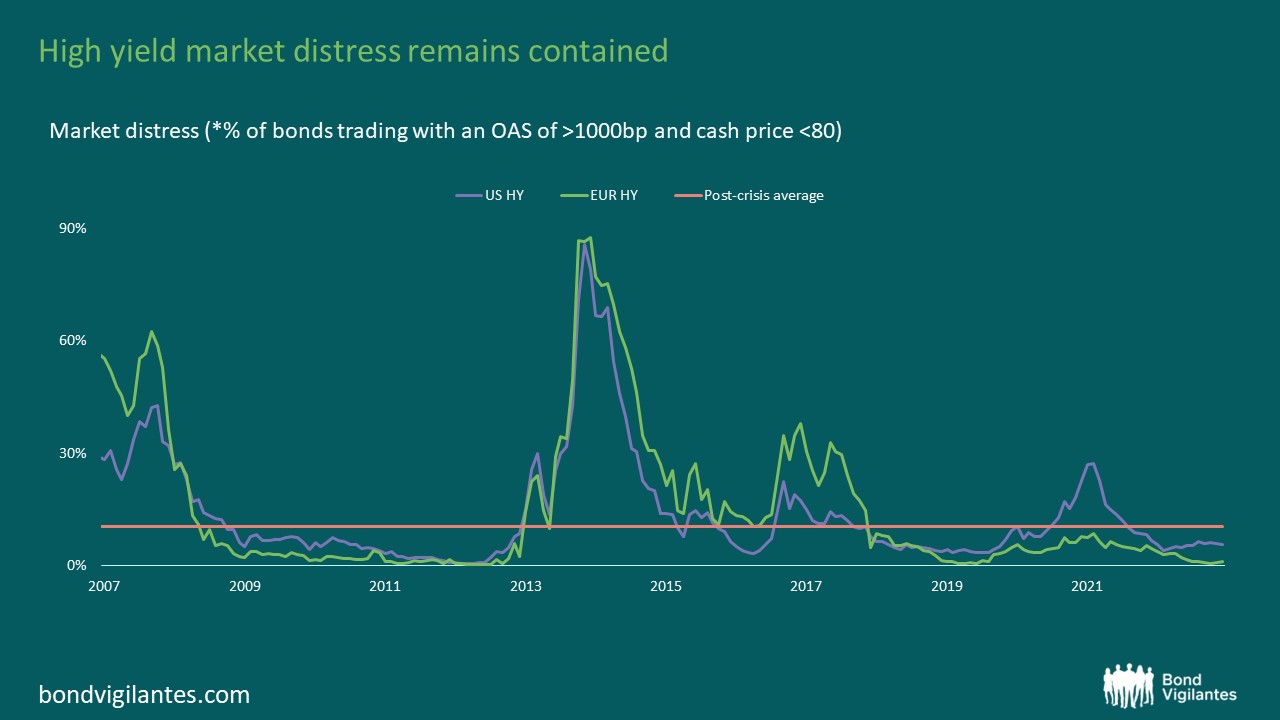

Secondly, albeit less active today, new issue markets remain very much open and functioning for companies to come and refinance. Market distress, usually a good proxy for credits that have lost market confidence in their ability to refinance, remains well below its post-crisis average for both the US and EU HY markets. When compared against past default cycles, current distress levels (7-8%) are not signalling a huge spike of defaults to come, and remain congruent with a soft economic landing.

Source: Bloomberg, BofA Merrill Lynch, M&G (August 2023)

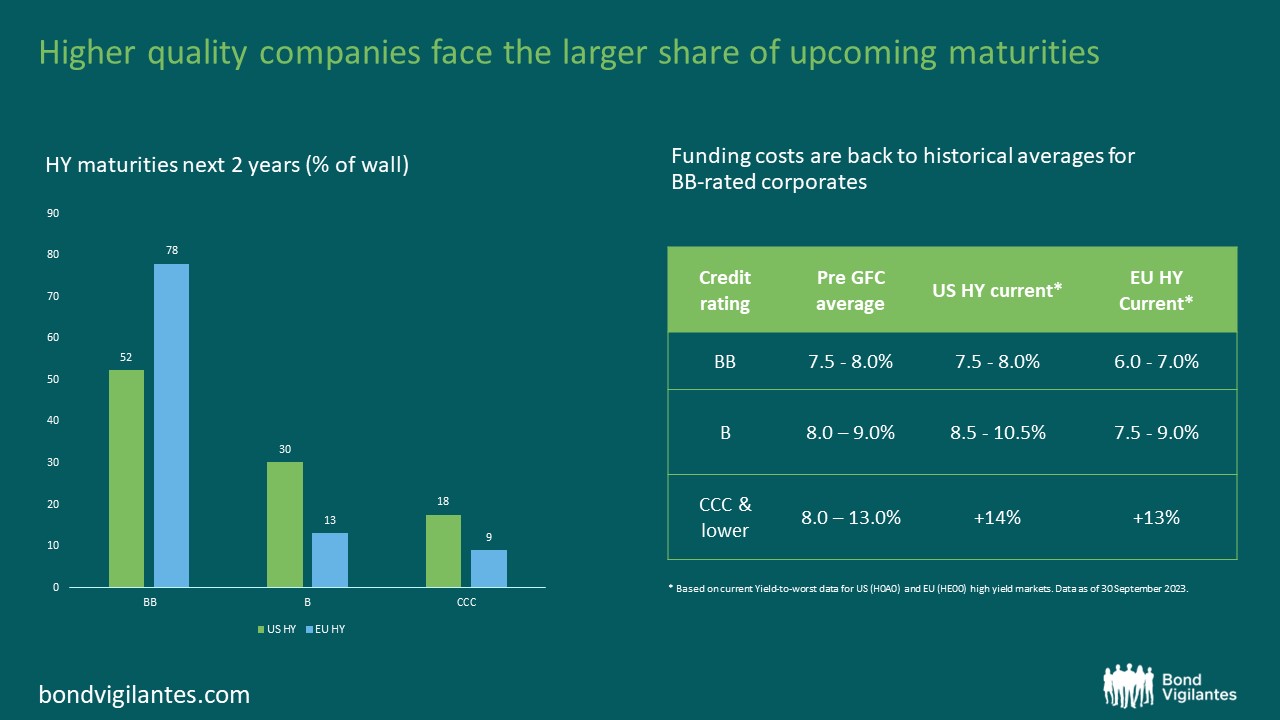

One final point to reflect on is who is set to be most affected by this short-term refinancing pressure. The next chart evidences that it is the higher quality companies (i.e. BB-rated issuers) that face the larger share of maturities coming due in 2024/2025. The BB-community not only tends to have healthier fundamentals, but also benefits from the most benign borrowing costs in high yield markets. As an example, issuing new debt today would cost a BB-rated European HY company about half as much (6.0-7.0%) vs what a CCC-rated issuer would have to pay for borrowing (14%).

Source: Bloomberg, LCD research, BofA Merrill Lynch, M&G (August 2023)

In summary, upcoming debt maturities are likely to increase financing pressures for high yield companies, particularly if elevated interest rates are sustained throughout a simultaneously slowing economy. While weaker credits are indeed likely to struggle to absorb the higher refinancing costs on top of deteriorating fundamentals, it is plausible that higher quality companies remain capable of climbing the steep refi wall. Having said that, doing the credit “homework” becomes all the more essential in the current environment compared to prior default cycles, particularly when it comes to distinguishing the healthier companies with those more at risk of facing refinancing challenges.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

For Investment Professionals only. Not for onward distribution. No other persons should rely on the information contained within this blog. This blog provides commentary and views on bond markets. Prepared by M&G’s bond team, this information is aimed at investment professionals wishing to supplement their understanding of these markets. Information shown on the blog should not be taken as advice or a recommendation to make an investment decision.

This weblog does not represent the thoughts, intentions, plans or strategies of M&G plc or any associated companies. They are solely the author’s personal opinion.

Inappropriate comments will be deleted or edited at the author’s discretion.

This blog may contain, or be linked to, advice or statements from third parties. M&G make no representation as to the accuracy, completeness, timeliness or suitability of such information and we have not, and will not, review or update such information and caution you that any use made of such information is at your own risk. Some of the information contained on this blog may also have been prepared or provided by third parties and may not have been verified by us. M&G hereby exclude any liability arising out of any preparation or provision of such information for this blog and make no warranty as to the accuracy, suitability or completeness of any such information.

With the exception of iviewtv.com, the links we provide from this blog to other websites are provided for information only. We do not assume any responsibility or liability with respect to any website accessed via our blog. We do not monitor or review any of the websites accessible through these links. Once you have used these links to leave this blog you should note that we do not have any control over that other website. We therefore cannot be responsible for the protection and privacy of any information that you provide whilst visiting such websites and such websites are not governed by our Terms & Conditions. You should exercise caution and look at the privacy statement applicable to the website in question.

The presence of any advert on this blog is not an endorsement by M&G of the goods, services or website advertised.

No liability is assumed for any use, or misuse, of the information presented on this blog.

As you are probably aware, internet email cannot be guaranteed and is not secure. We recommend that you do not send any confidential information to us by email. If you choose to send any confidential information then you do so at your own risk. Instructions sent by you via email, and to this blog, are processed exclusively at your risk.

Whilst M&G uses every reasonable effort to maintain the availability of this blog we cannot guarantee this. This blog may also change from time to time and we cannot guarantee the continuation of the services offered through it.