The latest US inflation report came in softer than expected, with headline inflation now at 7.7% YoY and core inflation at 6.3% YoY. Inflationary pressures eased a touch as the deceleration in CPI was generally broad-based. Core goods inflation turned negative for the month while core services ex-rents inflation decelerated (this was partially due, however, to a technical change in insurance inflation). Rents generally remains elevated, but will likely soften going forward reflecting the current state of the housing market.

Overall the report was positive, reinforcing the idea that inflation has peaked and is starting to lower. However, it provided us with very little comfort as to where inflation is going to settle. While there is clearly some positive news on the inflation front, which will help inflation trend lower next year, there are still some negative factors which will likely prevent inflation from falling back to 2% anytime soon.

In today’s blog I want to highlight four pieces of good news around inflation and four pieces of bad news to keep an eye on in 2023.

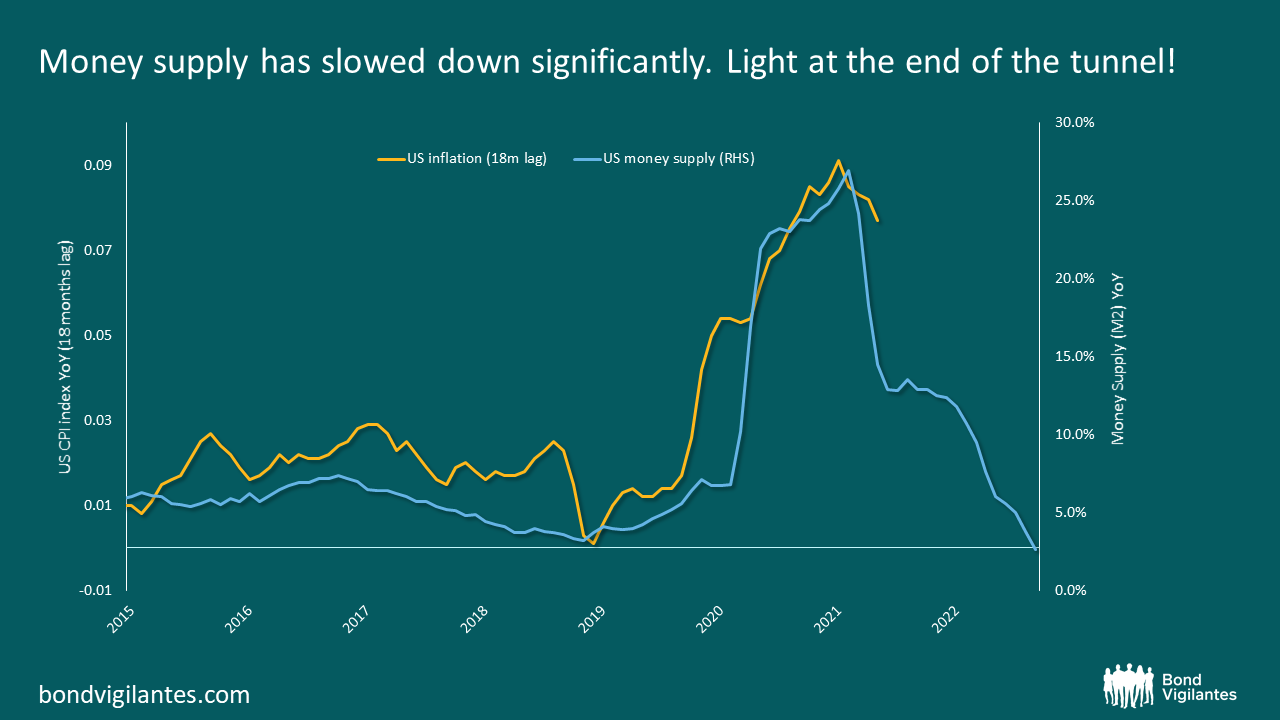

1. Money supply

The huge injection of money since the beginning of Covid is what caused inflation, but since then money supply growth (as measured by M2) has slowed down significantly and is now at a level consistent with 2% inflation.

Source: M&G, Bloomberg, 31 October 2022 (latest data available)

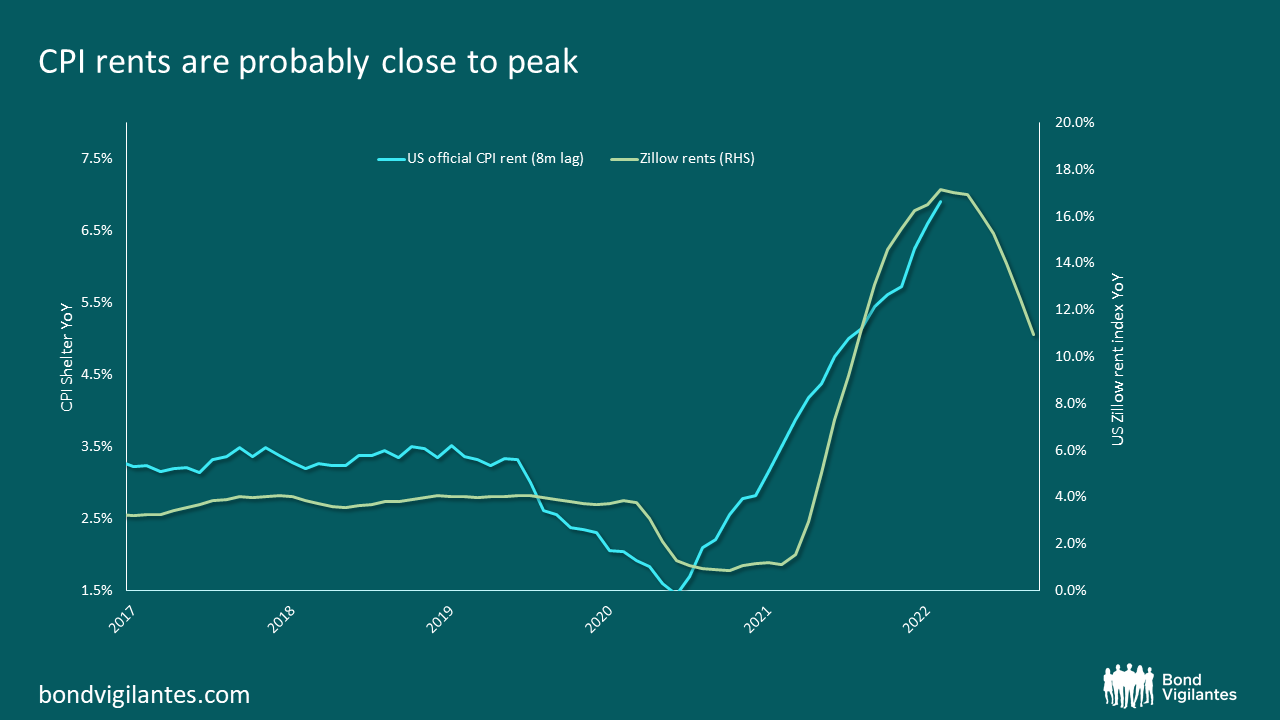

2. Rents

Rents are key in forecasting US inflation as they represent a big part of the index (c. 30% for headline CPI and c. 40% for core CPI). Rents have been rising for most of the year, helping push inflation higher, but we now might be close to a turning point. Rents in the CPI index is usually a lagging indicator, due to the way it is constructed (for example, data for official rents is collected only twice per year in order to capture a larger sample). There are, however, more timely – albeit arguably less accurate – rents indicators and they all are suggesting a slowdown in rents growth. This slowdown will likely start to be reflected in official measures too over the next few months.

Source: M&G, Bloomberg, 31 October 2022 (latest data available)

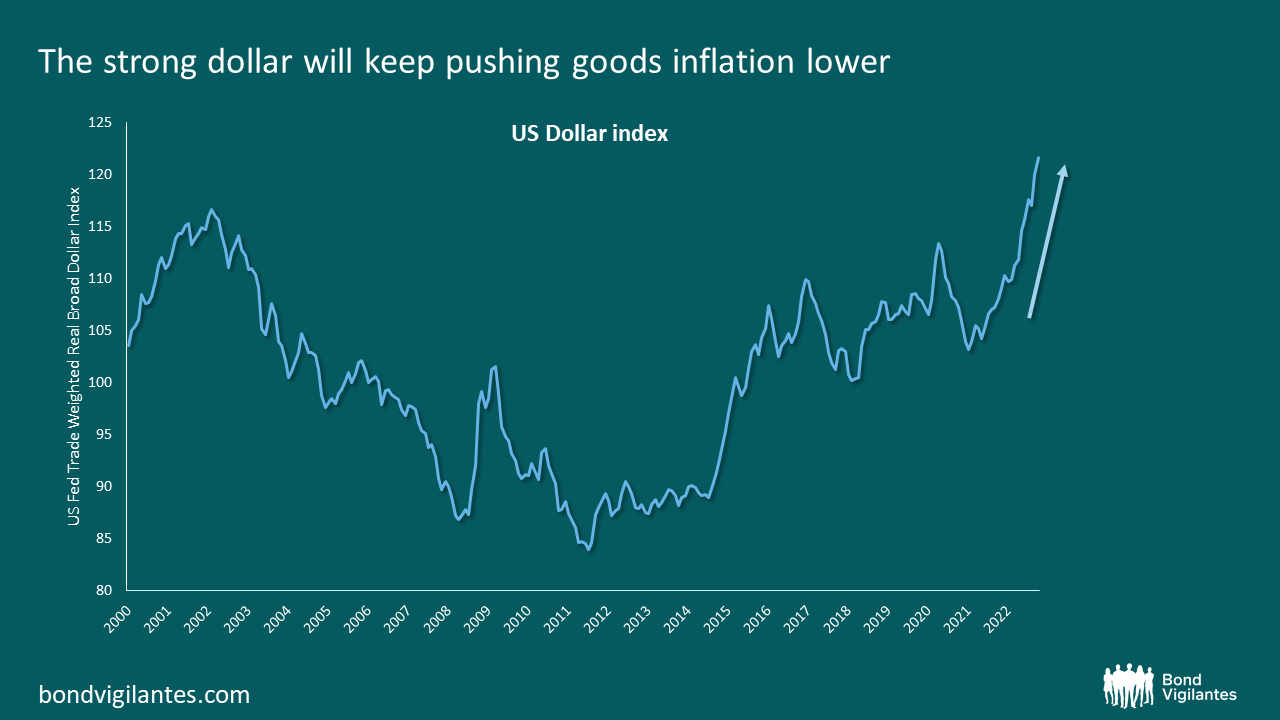

3. Dollar

The US dollar has been rising sharply this year and this has impacted and will continue to impact inflation, particularly goods inflation. As most of goods are imported, a strong US dollar will likely results in lower goods prices.

Source: M&G, Bloomberg, 31 October 2022

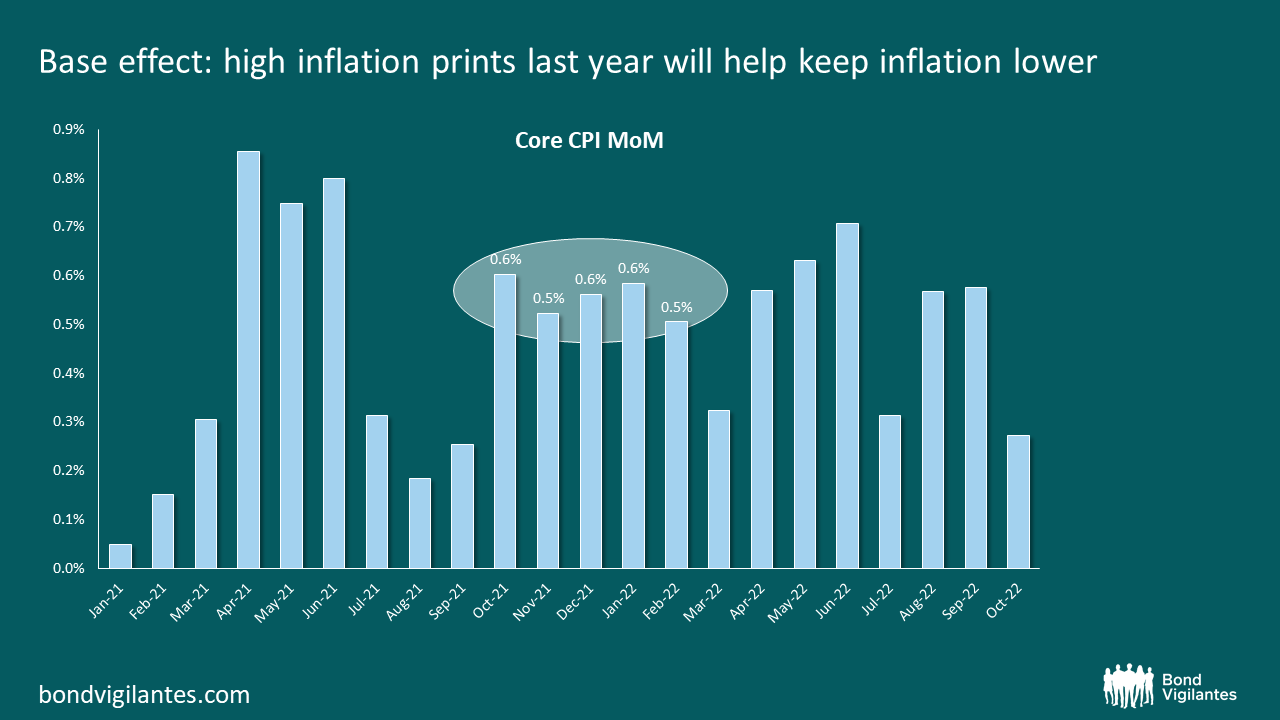

4. Base effect

This is more of a short term effect which might help to push YoY inflation lower. Last year, from October to February, core CPI was fairly high averaging almost 0.6% MoM. This means that, for core inflation to keep rising YoY, we need to see some fairly high MoM numbers over the next 5 months: possible, but tough given that core goods inflation is decelerating while rents growth will likely start to moderate soon.

Source: M&G, Bloomberg, 31 October 2022

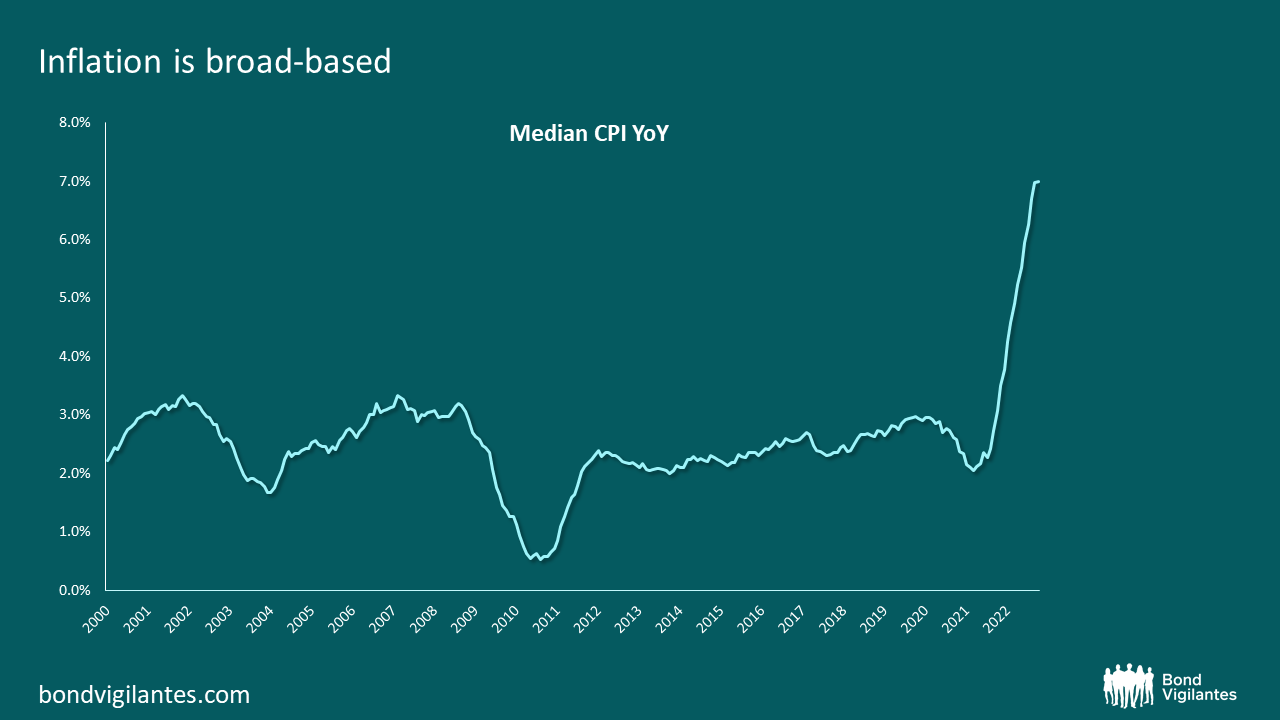

1. Broad-based inflation

Inflation is now broad-based. It is not just a few items driving overall inflation up: most of the items are now seeing prices rising fast. A good way to visualise this is to look at median CPI, which is less impacted by outliers since it focuses on the core of the distribution. Inflation remains very much broad-based.

Source: M&G, Bloomberg, Cleveland Fed, 31 October 2022

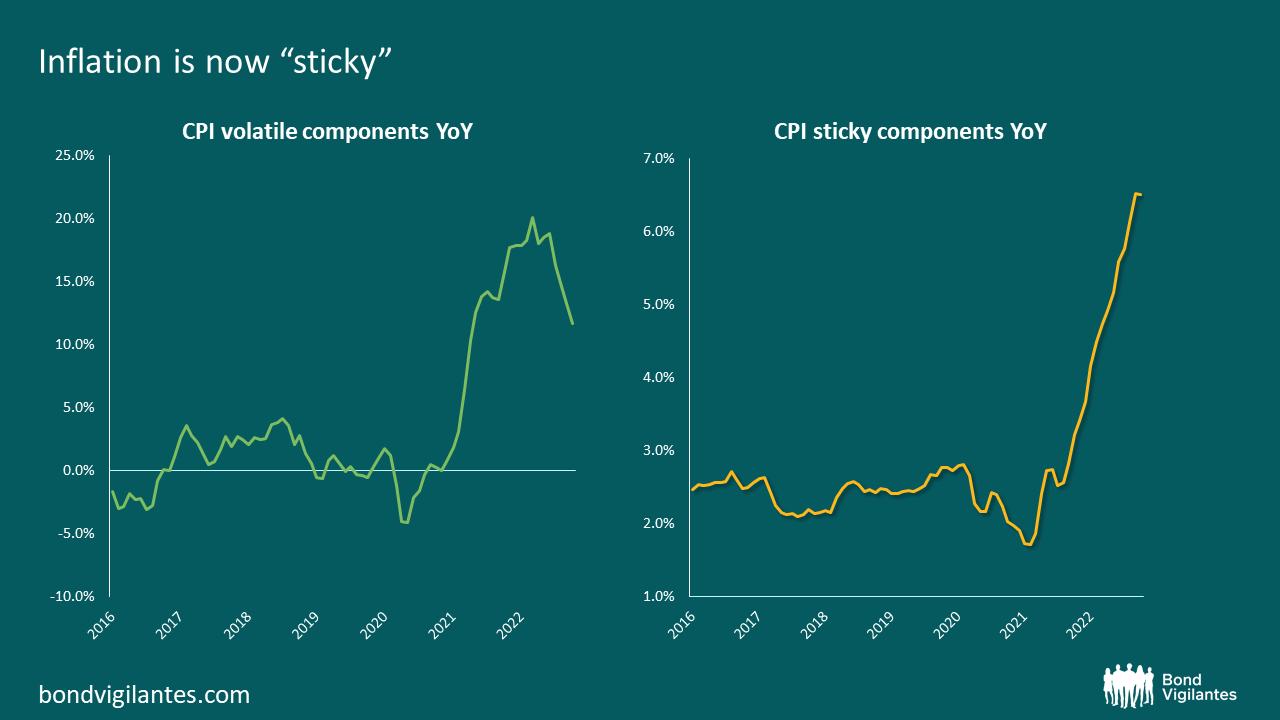

2. Sticky inflation

As economies reopened, people started to shift their consumption away from goods into services. As a result, goods inflation is now decelerating, while service inflation is rising fast. The problem is that service inflation, unlike goods inflation, is usually very sticky. As a result, we might not see a sharp deceleration in inflation anytime soon. Below you can see a chart showing the sticky components of inflation vs the more volatile items. While the latter have started to trend lower, the sticky part of the inflation basket is now on the rise.

Source: M&G, Bloomberg, Atlanta Fed, 31 October 2022

3. Wages

Wages have been rising this year and this is important as wages are the major input cost for most services. If wage growth remains high or even accelerates from here, there is potential for more inflation surprises going forward. Keep an eye on wages and on a potential wage-price spiral as this could completely change the inflation picture for next year.

Source: M&G, Bloomberg, Atlanta Fed, 31 October 2022

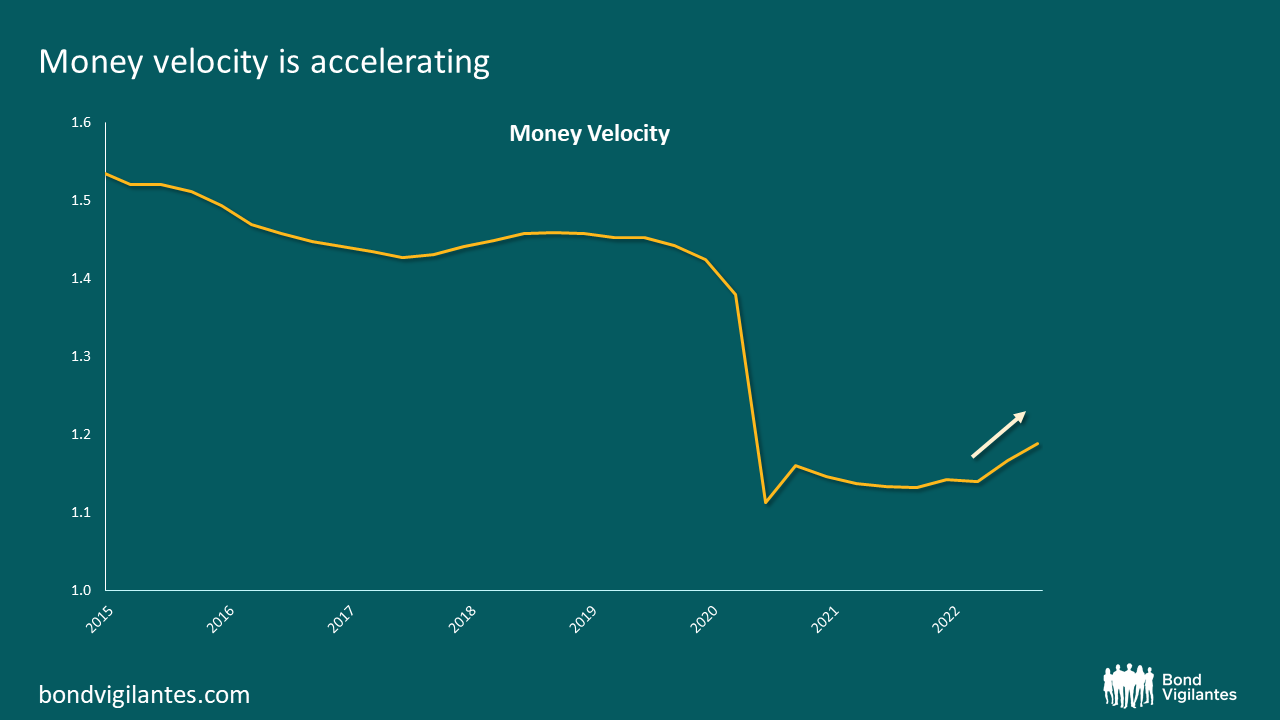

4. Velocity

One thing that hasn’t been discussed much so far is money velocity (how quickly money circulates within the economy). Higher rates usually pushes velocity up as consumers look for opportunities to deploy their cash. Recently, we have seen an acceleration in money velocity. If this continues, inflation might remain elevated even if money supply falls.

Source: M&G, Bloomberg, 30 September 2022

Conclusion:

There seems to be light at the end of the inflation tunnel, particularly as money supply has collapsed down to levels consistent with 2% inflation. Quantitative tightening can accelerate this trend further, potentially pushing M2 into negative territory. Inflation has now become very sticky and broad-based, however, while wage growth is still not consistent with 2% inflation. Moreover, the velocity of money remains a big unknown and could keep inflation high even if money supply falls.

As things stand right now, a further deceleration in inflation seems probable, but a quick return to normality still looks unlikely.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

For Investment Professionals only. Not for onward distribution. No other persons should rely on the information contained within this blog. This blog provides commentary and views on bond markets. Prepared by M&G’s bond team, this information is aimed at investment professionals wishing to supplement their understanding of these markets. Information shown on the blog should not be taken as advice or a recommendation to make an investment decision.

This weblog does not represent the thoughts, intentions, plans or strategies of M&G plc or any associated companies. They are solely the author’s personal opinion.

Inappropriate comments will be deleted or edited at the author’s discretion.

This blog may contain, or be linked to, advice or statements from third parties. M&G make no representation as to the accuracy, completeness, timeliness or suitability of such information and we have not, and will not, review or update such information and caution you that any use made of such information is at your own risk. Some of the information contained on this blog may also have been prepared or provided by third parties and may not have been verified by us. M&G hereby exclude any liability arising out of any preparation or provision of such information for this blog and make no warranty as to the accuracy, suitability or completeness of any such information.

With the exception of iviewtv.com, the links we provide from this blog to other websites are provided for information only. We do not assume any responsibility or liability with respect to any website accessed via our blog. We do not monitor or review any of the websites accessible through these links. Once you have used these links to leave this blog you should note that we do not have any control over that other website. We therefore cannot be responsible for the protection and privacy of any information that you provide whilst visiting such websites and such websites are not governed by our Terms & Conditions. You should exercise caution and look at the privacy statement applicable to the website in question.

The presence of any advert on this blog is not an endorsement by M&G of the goods, services or website advertised.

No liability is assumed for any use, or misuse, of the information presented on this blog.

As you are probably aware, internet email cannot be guaranteed and is not secure. We recommend that you do not send any confidential information to us by email. If you choose to send any confidential information then you do so at your own risk. Instructions sent by you via email, and to this blog, are processed exclusively at your risk.

Whilst M&G uses every reasonable effort to maintain the availability of this blog we cannot guarantee this. This blog may also change from time to time and we cannot guarantee the continuation of the services offered through it.