Evidence that a company wields pricing power in its industry is the best indication of a sustainable competitive advantage, argues Giles Parkinson.

Evidence that a company wields pricing power in its industry is the best indication of a sustainable competitive advantage, argues Giles Parkinson.

“Not everything that counts can be counted, and not everything that can be counted counts,” wrote the sociologist William Bruce Cameron.1This maxim is worth pondering as the fallout from the coronavirus pandemic prompts many of us to reconsider how we spend our money.

During challenging times, we seek to quantify value. In some rare cases, we may find ourselves willing to pay more for a company’s product or service than we currently do. The cost of some luxury fashion items has risen during the pandemic, while studies show that when stranded at home under lockdown, subscribers would pay more for technology platforms such as Spotify than the current fee, despite the availability of cheaper alternatives.2

“If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business,” as Berkshire Hathaway chairman and CEO Warren Buffett once put it. “And if you need a prayer session before raising the price by a tenth of a cent, you’ve got a terrible business.”3

Buffett is right: pricing power is the best indicator investors have of a long-term competitive advantage. But it is not always easy to spot.

In assessing whether a company is likely to prove successful over the long term, investors need to consider many factors, such as the quality of its management and potential for growth.

Some investors also rely on measures such as high returns on invested capital. While this is a useful metric, it can be distorted: returns can be inflated by temporary cyclical conditions, for example. And many companies now tend to focus their capital outlays on intangible assets such as software and design, making it more difficult to quantify returns on investment than was the case when companies invested mostly in physical assets and equipment.

In this context, pricing power comes into its own as a practical and reliable index of a company’s competitive advantage. In microeconomics, the concept is broken into two categories: nominal pricing power and real pricing power. Nominal pricing power refers to a company’s ability to raise prices in line with inflation, allowing it to cover input costs and preserve profits. This is useful, but real pricing power is more interesting from an investment perspective, as it refers to a company’s ability to raise prices above inflation. Many investors view nominal and real pricing power as synonymous, but there is a subcategory of firms with real pricing power that can consistently and sustainably raise prices faster than the rate of inflation.

This has significant implications for equity valuations, which are usually calculated on the basis of discounted cashflow (DCF). The DCF model assumes that after the explicit forecast period, a company will continue to generate cashflows at a constant rate in perpetuity; this is known as terminal value. As inflation is a factor in calculating terminal value, the figure should be higher for a company with real pricing power; this, in turn, is likely to imply a higher valuation for the business today.

So, what does pricing power look like in the real world? The first thing to say is that pricing power can exist on a sector or company level. Sometimes it emerges as a consequence of the specific dynamics of a particular industry.

Take spirits, a product where pricing power is partly a quirk of tax policy. Because alcohol is highly taxed, the manufacturer’s share takes up a smaller component of the retail price of a bottle than is the case for other products. This means marginal price rises can yield a proportionally higher increase in profits for the manufacturer.

Or consider credit ratings. In many cases, bonds must have a minimum credit rating from two of the three main ratings firms to satisfy the requirements of regulators and investment mandates. If a bond has such a rating, the issuer can therefore sell the debt with a much lower interest cost than would be the case for an unrated bond, because there are more buyers for it. But what the rating agencies charge is only a fraction of the overall “value”. The difference between the price charged and the value created gives the rating agencies considerable pricing power.

Elsewhere, pricing power reflects the more indefinable characteristics of a product or brand. The price of luxury handbags, for example, has historically risen far in excess of inflation. According to research from Boston Consulting Group, which tracked the median price of a luxury handbag across seven brands between 2002 and 2012, prices increased at an annual rate of 14 per cent in the US, significantly outpacing the average inflation growth rate of 2.5 per cent over the period.4 Brands such as Louis Vuitton and Hermès have hiked prices in 2020.5

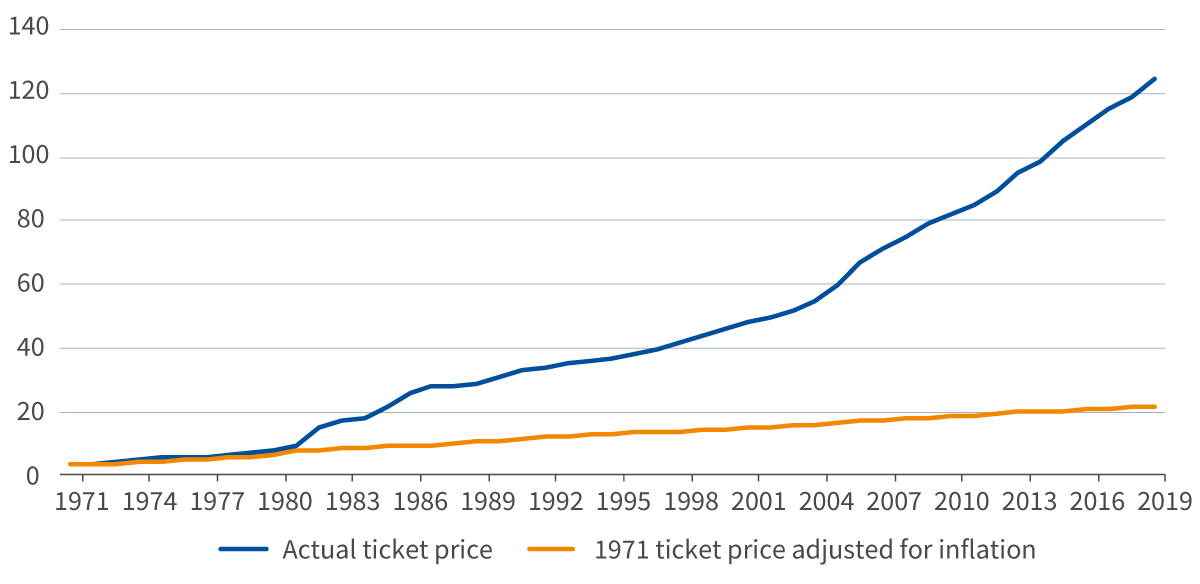

Another good example is the price of Disney theme park tickets. Figure 1 shows the price of a single ticket to Walt Disney World in Orlando, Florida, from its opening in 1971 to 2019, compared with the original price ($3.50) as adjusted for the year-on-year rate of inflation. If the price had simply risen in line with inflation, the current cost of a ticket would be around $22; the actual cost in 2019 was $125. This is evidence of pricing power that has persisted for almost half a century.

Figure 1: Price of a single ticket to Disney World

Source: Bureau of Labor Statistics, GoBankingRates, 2020

Companies that can raise prices consistently while retaining customers have a formidable competitive advantage. In an equity portfolio, such firms can help drive resilient returns over the long term. The challenge is how to identify them ahead of the wider market.

Consumer surveys can give investors a sense of a company’s pricing power before it raises prices. Take Netflix. A survey of 2,500 US consumers in May 2020 showed 55 per cent would be willing to pay more for Netflix than they currently do, up from 47 per cent in December 2019.6 This reflects how the company’s pricing power has increased in the current circumstances (though it has yet to raise the subscription fee).

Usage data can also provide an indication of tech companies’ pricing power. For example, Comscore data shows Google Maps has more users on iPhones than Apple Maps, even though the Google app is no longer pre-installed on the device. Moreover, those who prefer Google Maps spend almost ten times longer using the app, on average, than Apple Maps users. Similarly, Google-owned YouTube is now downloaded on 90 per cent of iPhones, despite not being pre-installed.7 This suggests users consider Google products to be superior, giving it scope to further monetise its platforms and potentially providing some insulation against regulatory risk – an important consideration in light of the ongoing Department of Justice antitrust lawsuit against parent company Alphabet.

Consumer surveys do not always provide a full picture of the factors behind pricing power, however. Take luxury handbags, where ownership is associated with such intangibles as self-worth; in this case, the desirability of the item also increases along with the price. As for Disney, one reason it has been able to raise the price of its theme park tickets over time is that a trip to the Magic Kingdom has a deeply ingrained cachet for American families. In this case, pricing power is based on a mixture of brand loyalty and cultural prestige over five decades.

In gauging the sustainability of a company’s pricing power, investors will need to make judgements based on these kinds of qualitative factors, as well as surveying the company’s revenue history and current consumer sentiment.

Unlike quantitative metrics, which tend to get dropped into a Bloomberg spreadsheet and quickly arbitraged away, assessing qualitative factors is more challenging – and therefore more rewarding for assessing value. In other words, pricing power counts, but the factors driving it cannot always be counted. And that brings opportunities for equity investors seeking to build robust portfolios over the long term.

References