The emergence of data infrastructure was a defining theme in the last decade. As the sector matures, Laurence Monnier explains why further expansion, consolidation and the development of a secondary market are likely.

The emergence of data infrastructure was a defining theme in the last decade. As the sector matures, Laurence Monnier explains why further expansion, consolidation and the development of a secondary market are likely.

The transmission and storage of data support essential public needs, making these assets infrastructure-like by nature. Yet data infrastructure, which includes data centres, fibre-optic towers and mobile phone antenna, has characteristics that sets it apart from more traditional infrastructure assets such as power or transport. This is creating opportunities for investors, although capturing them is not straightforward.

Fast-changing technology and demand, coupled with less regulation, make it difficult to assess long-term demand for specific assets. This explain why long-term investors are likely to focus on assets benefiting from contracted revenues or high barriers to entry, situated in a jurisdiction with clear regulation, and with good ESG credentials.

Here, we set out the themes likely to drive the next phase of the sector’s development.

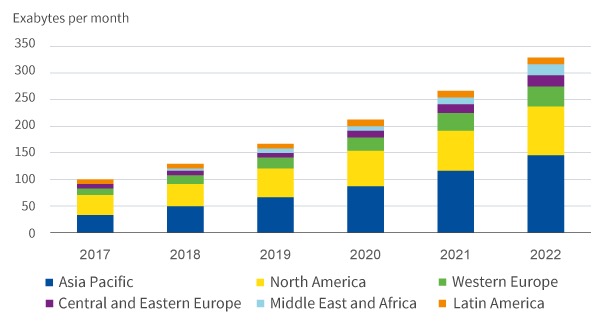

The world’s appetite for data is voracious, driving the need for new infrastructure to transport and store it. Driven by new applications, this trend is likely to continue. Based on Cisco’s forecast, data traffic will grow at an annual rate of 27 per cent between 2017 and 2022.

Figure 1: Growth in data

Source: Cisco VNI, 2019

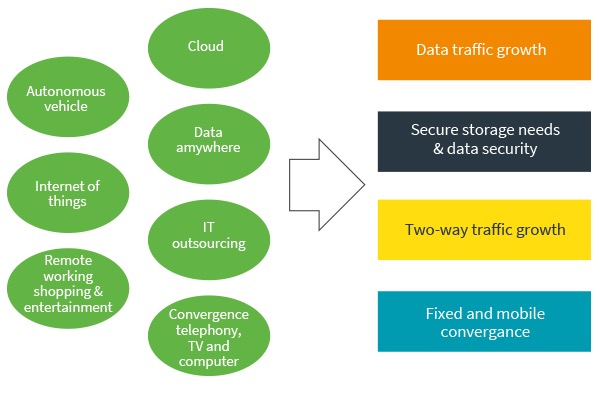

No longer limited to the corporate world, data is now needed to support most aspects of human lives. The breadth of uses is continually growing: from online dating to video streaming, from homework to working from home, from payments to fitness, the flow of data transfer keeps evolving. Data is not only supporting, but also changing the way we live. These major societal changes have profound implications for the infrastructure required to move it.

Figure 2: A breadth of uses

Source: Aviva Investors

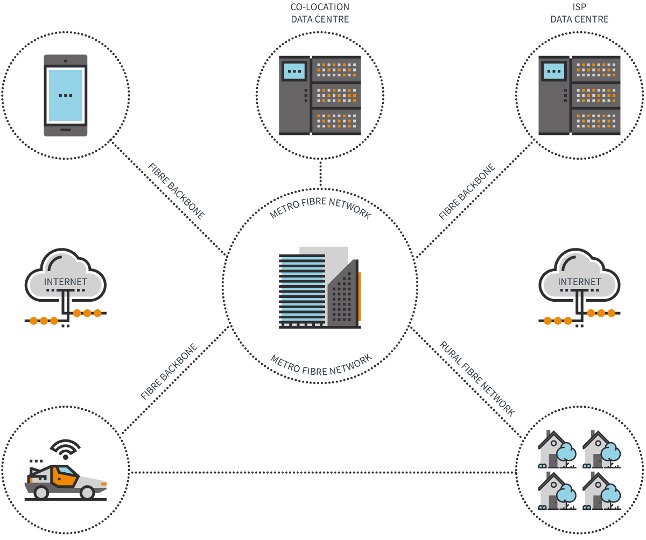

One thing is clear: significant investment in new network infrastructure is needed – including in fibre optic cables, mobile cells, and data centres.

Figure 3: The data ecosystem

Source: Aviva Investors

Yet, as the market matures, we also predict more consolidation among networks, and a growing secondary market.

Resilient and fast access to data is no longer a nice to have: it is an essential public service. In that sense, data transmission and storage assets have infrastructure-like characteristics, just like water or power networks. Infrastructure investors have taken notice: a 2019 survey of European infrastructure investors commissioned by global law firm DLA Piper found debt and equity investors expected to increase their exposure to data centres by 33 and 18 per cent respectively.1

Investors typically allocate to infrastructure assets for stable, long-term cash flows. But, as previously stated, data infrastructure has characteristics that set it apart from traditional infrastructure sectors.

Rapid technological change brings obsolescence risk

The means of transporting data have evolved rapidly. Copper networks have existed for over 100 years, co-axial cable for 50 and broadband for 20. In this accelerating world, this poses difficult questions: how long term is data infrastructure; could today’s fibre-optic cables and telecom towers become tomorrow’s copper?

Despite this, demand for fibre-optic cables, mobile towers and data centres appears set to continue for the foreseeable future, although the characteristics of the network will no doubt evolve.

In 2020, 5G development is expected to start in Europe. This technology can compete with fibre to provide data to the home. The high frequency used in 5G requires more micro cells to be installed close to buildings – rather than relying on more distant masts used by 3G and 4G macro cells. This shift could bring increased competition to existing fibre-optic and tower networks, but also new opportunities for investors: more cells will need to be installed, and more fibre will be needed to connect them.

Given the high investment costs, there could be infrastructure sharing between operators, increasing the revenue potential for new sites. Furthermore, the cost of installing many cells means deployment in less densely built areas already connected to broadband is a long way off, affording some protections to rural broadband investors. In the UK for instance, the government has ambitions for 50 per cent of the population to be covered by 5G signals by 2027.2

The longer-term picture is less clear, however. Technological changes could make alternatives ways to relay data (for example satellite or aircraft borne) less costly and more efficient. They may also allow mobile devices to be used as repeaters or transmitters of data, instead of independent cells. These technologies could complement existing networks – much like Wi-Fi or satellites complement fibre and towers today – or could make part of the network obsolete.

Longer-term investors will seek assets with long-term contracts and will also need to be rigorous in their analysis of future demand and rent renewal risks.

From network to cloud

There is only one water pipe that brings water into homes. In the digital world, data anywhere is making demand and competition difficult to pinpoint. For example, mobile streaming means demand for online video impacts the usage of both mobile and fixed data infrastructure.

The advent of autonomous vehicles and internet of things also mean the number of points needing two-way data traffic will expand and transform rapidly. In a world where new applications create new demand, the lack of clarity over what piece of infrastructure is used to transport different data types is not a concern. However, the configuration of data networks needs to adapt faster to support evolving demand than other infrastructure networks.

Regulation is critical

In most cases, data infrastructure assets do not have a monopoly, and therefore no regulated revenue. Demand is high, but the price of data has been shown to drop rapidly once the network is built if competition increases.

Regulation plays an important role in setting the pace of competition. By protecting a market for a period (via concessions for instance) or facilitating competition (through mandating access for new entrants to incumbents’ rights of way), regulators and legislators play a key role in determining how a market evolves.

Governments can also speed up the adoption of new technologies. For example, France has encouraged the development of rural broadband networks by allocating subsidies for specific concessions. Europe has many different models, and it is critical to understand the framework in each market to assess demand.

Faster and more secure data has been proven to support economic growth by helping businesses and consumers connect.

Access to data can also have significant social benefits. For example, connecting a rural community to fast broadband gives residents better access to such services as health, education and banking. It can also encourage a younger population to settle by facilitating remote working. A 2018 report by the Department for Digital, Culture, Media and Sport3 found connection to superfast broadband to be beneficial to people in rural areas, providing a wellbeing uplift equivalent to £222.25 per year per premises upgraded.

These benefits provide a clear economic and social investment case for broadband, particularly where new communities can be connected by high-connection speeds.

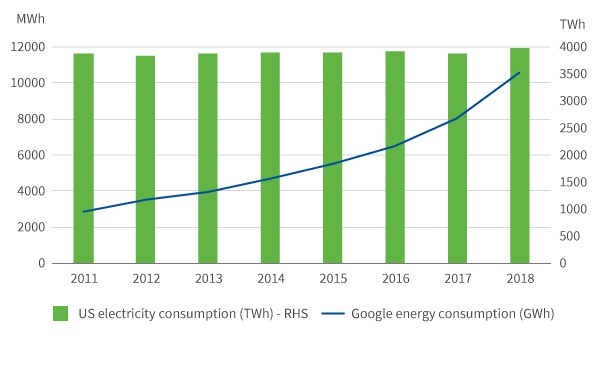

Figure 4: Energy consumption – Google

Source: Statista, enerdata

In environmental terms, data can also play a positive role – for example, by helping regulate energy consumption around times when clean energy is available.

However, storing data in hardware-filled, temperature-controlled data centres requires vast amounts of energy, as well as water for cooling.

For example, Google, despite its environmental focus, last year consumed over 10,000 GWh of power.4 This is the equivalent to the consumption of 3.4 million average UK households5 – and appears to be rising exponentially.

A 2017 study estimated data centres consumed 3% of world’s energy and could use one fifth of all electricity in the world by 2025.6 Investors should therefore carefully analyse the environmental credentials of their assets - such as the source of the electricity and water consumed, and the energy efficiency of the building – to reduce the environmental impacts. Within the data infrastructure sector, data centres are most susceptible to be impacted by any regulation aligned to zero-carbon objectives.

Data: The infrastructure of the future?

Data infrastructure is growing and evolving faster than other infrastructure networks. The sheer pace of change creates exciting opportunities for investors, but also difficulties in assessing the long-term business case.

While assets such as data centres, cell towers and broadband networks look to offer resilient cash flows, the shape of future opportunities is harder to predict. Who knows: with the wide availability of data and the advent of blockchain, could data itself become the infrastructure of the future?

References