Demographic changes are set to have a significant impact on the world economy in the coming decades, as we have discussed on a number of occasions ( All The People, So Many People: Most Of The Growth In Emerging Markets, Either The Demographic Bond Models Are Broken, Or Yields Are Headed To 10%). After a 40-year bull market in bonds with yields trending in one direction, might we see a pivot given the demographic outlay ahead? A discussion for another day, but for now, let’s look at whether all is as it seems on the surface. Last month’s Deutsche Bank report[1] on the market impact of demographic changes to 2030 got me thinking about this a bit more. These demographic challenges are particularly the case in developed market economies (DM) and notoriously in China following the One Child Policy. As populations mature, this brings strains on government spending, as budgets for healthcare and social security payments swell to meet the needs of older people. At the other end of the spectrum, tax receipts decrease as there is a smaller proportion of working age people to fund this increased spending.. So far, so challenging. How are we going to resolve this? Well, the answer may already be with us. Although people are living longer, they are also working longer and are in better health. Emerging market economies (EM) have ever improving education systems, producing people who can fill skills gaps. We are also in a world of significant technological advancement. Might AI save the day?

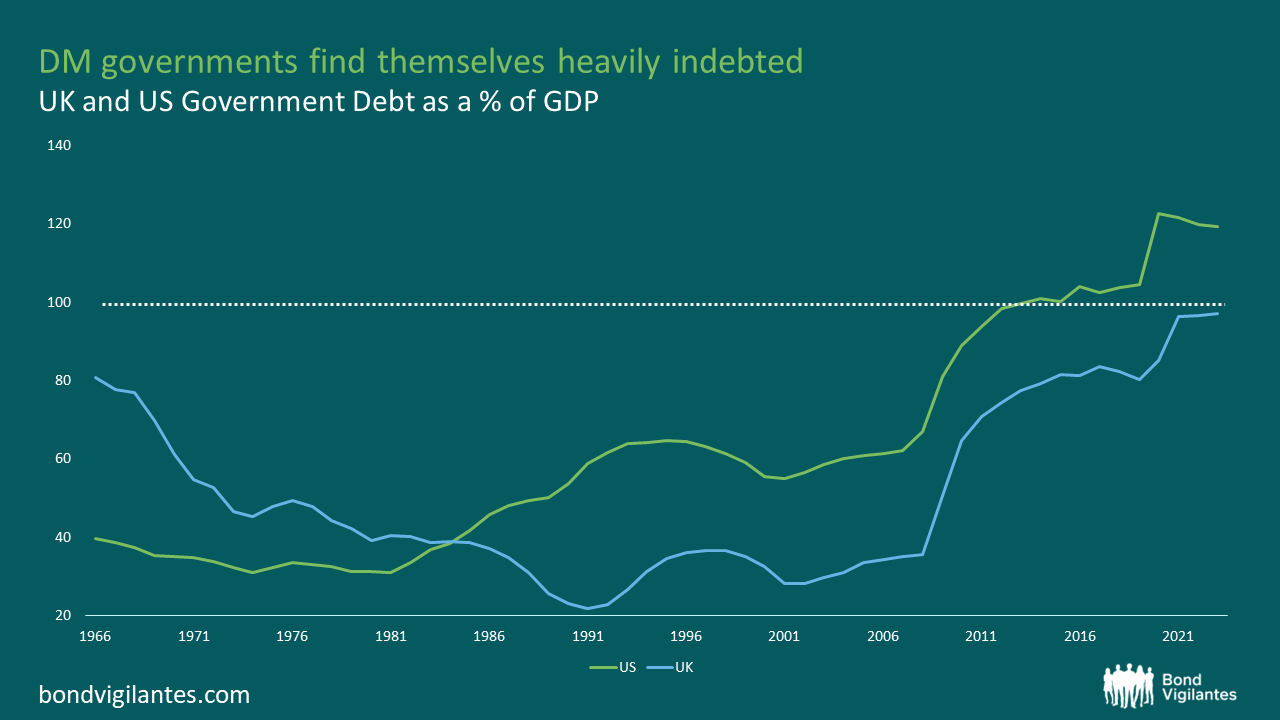

Many DMs are already facing significant debt challenges. The UK and US both find themselves in the unenviable positions of triple figure debt-to-GDP levels, having steadily climbed since the 1990s.

Source: ONS, St Louis Fed, M&G (September 2023)

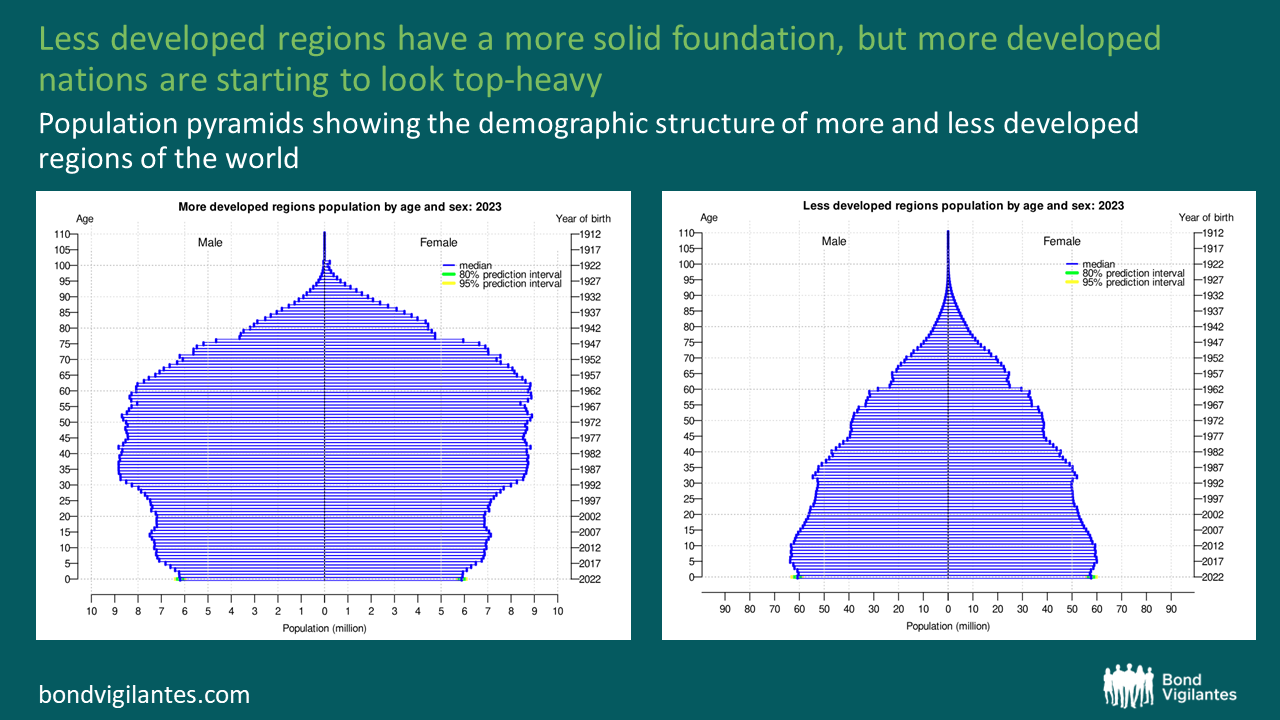

This threatens economic stability, as increased healthcare expenses, rising pension costs and the prospect of diminished tax receipts will soon pile on the pressure as the baby boomers advance into their 70s and 80s. The demographic challenge ahead was a (small) contributing factor in Fitch’s downgrade of the US Government in August. This is a problem shared by Western European nations and famously, Japan. Imagine the population pyramids below are buildings. A building with a nice solid base and firm foundations does not give cause for concern. It will happily stand there and be fine. But a building that is little thin on the bottom and chunky on top might be a worry in the event of a strong breeze!

Source: United Nations (November 2023)

The team at Deutsche Bank, as part of their Demographics Report looking at the market impact to 2030, raise a particularly interesting point in respect to the shape of the US population. The US has an advantage in the strength of its upcoming cohort of 30-44 year olds towards 2040. This group drive the ‘carpet market’ – the multiplier effect created when people move house and buy new carpets, furniture, decorate and all these other things that make a house a home. This group are also progressing in their careers, often seeing increasing salaries and thereby contributing more in tax receipts. This should help to buoy the US through the period when the boomers will begin to draw more on government spending. This highlights the significance of looking through to key age groups within the pyramid and not only the general shape.

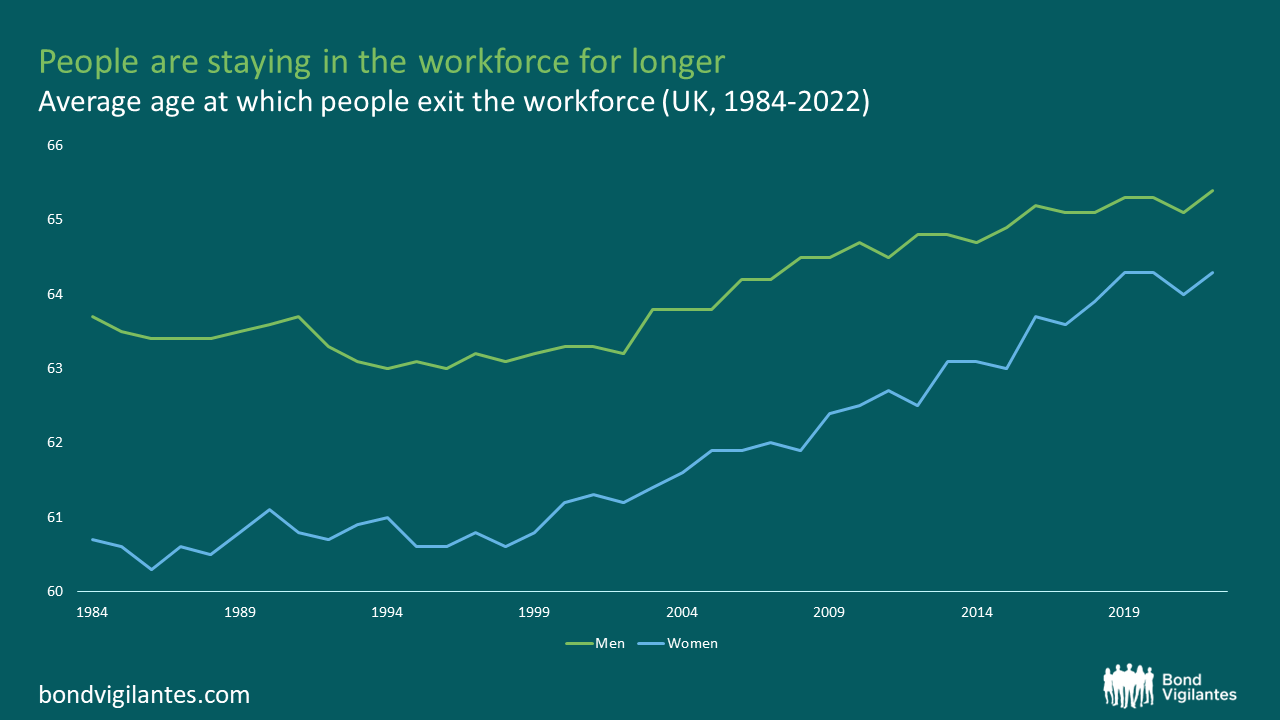

Life expectancies in the world’s most developed nations have increased by more than 10 years since 1970, with those born today expecting to live past 80 in many cases.[2] Consequently, retirements are lasting longer, which means pensions and social security are paid out over a longer period. However, in the same period the average age at which people are leaving the workforce has increased. In the UK, this has steadily grown over the past 40 years (see graph below) having previously declined as standard of living increased in the post-war period. This trend holds true across the OECD. This somewhat offsets the effects of the ageing population as people continue to contribute to the economy from both a tax and consumption perspective. The ONS even posed the question ‘is age 70 the new age 65’ in 2019. We can think of someone who is 60 today as ‘younger’ than a 60 year old in 1990. The perceived pressure on the economy may not be quite as bad as we think.

Source: ONS (September 2022)

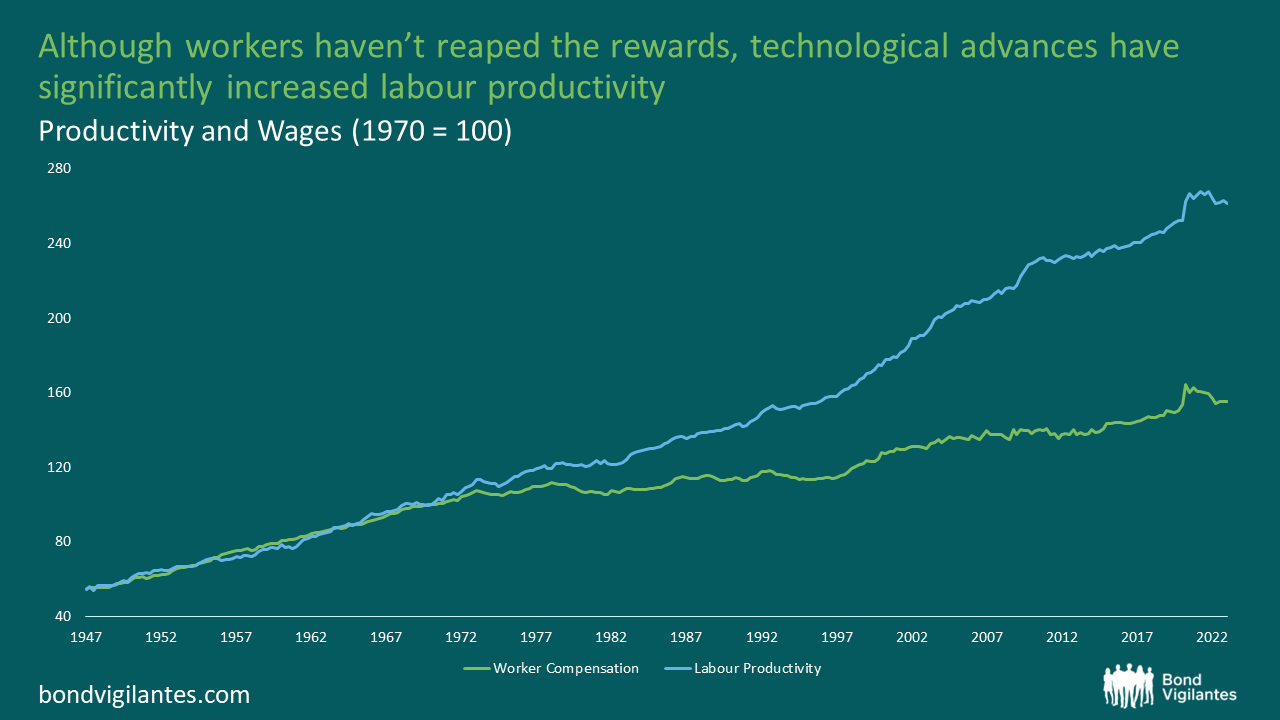

Technological advances in the last 50 years have meant that the labour force now produces more with less, albeit the workforce may not be seeing its fair share of the proceeds! The striking chart below shows the divergence between labour productivity and worker pay since the 1970s, roughly the time at which we have begun to see significant technological advances in machinery and computer systems. From the end of the Second World War to the early 70s, this relationship was very tight and both saw steady growth. This was also the era of the decline of trade unions and worker power, the advent of the neoliberal state form and increasing inequality of wages between executives and employees. These changes are firmly established and form part of the status quo. With the recent developments in AI, much tipped to change the world, I expect this divergence to continue over time as technology supplements a declining workforce. As a result, economic growth will continue as technology picks up the slack.

Source: Federal Reserve Bank of St Louis, M&G (June 2023)

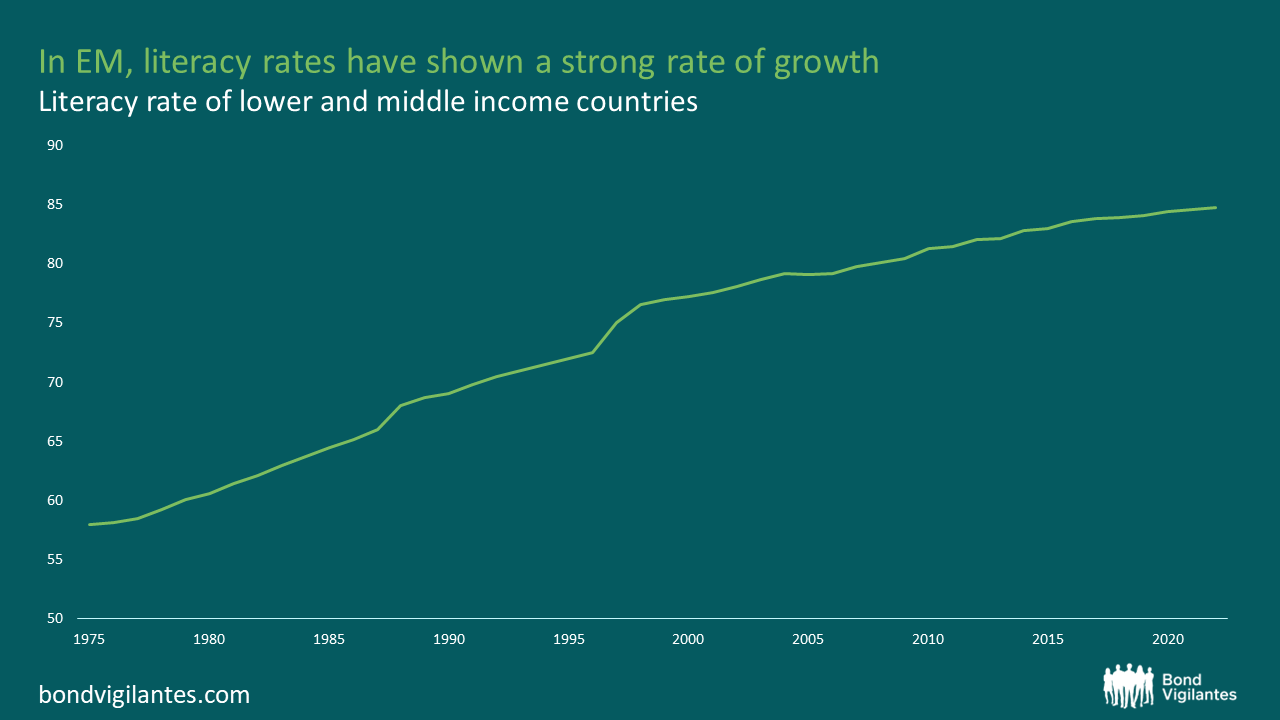

Whilst economic and social indicators continue to improve in DMs, albeit at a slower rate, the rate of improvement on both fronts in EM has been substantial. The data for higher education is slightly patchy at regional levels, so I have taken literacy rates as a proxy. In the lower and middle income nations (as defined by the World Bank), literacy rates have increased from 58% to 85% since 1975. Some of the most educated people from these countries move to DMs in search of a better standard of living. While there may be a shrinking number of people rising through the education system and progressing into the workforce domestically, there is a plethora of well-educated people from EMs who can help fill skills gaps.

Source: World Bank

There has also been significant increase in the amount of international students – mostly from Asia – who flock to DMs for the higher education.[3] These are overwhelmingly in Anglophone nations – UK, USA, Canada, Australia. In many cases, these students remain in the country of study and then join the workforce. The above DMs who often become home to foreign students and those from other EMs who come seeking a better life, stand to benefit. However, other DMs, notably South Korea and Japan, have much lower net migration figures (0.358 per 1000 in South Korea and 0.516 in Japan vs 2.240 in the UK).[4] This suggest that these nations are unlikely to see this skills gaps filled.

The DB team points to the claim of the 18th century of economist, Thomas Malthus, who predicted that GDP growth would decline as a result of the quickly rising population at the time. How different the reality has been. Today’s challenges are very real, as is the potential threat. However, people exiting the labour force later in life helps ease pressure, as does future strength in the ‘carpet market’ cohort, which is especially the case in the US. Technological advances and well-educated workers from EM economies filling skills gaps may also stem the tide. On the other hand, if we don’t see any of these mitigating factors come to fruition, then we’ll feel the pain of those dodgy pyramid foundations. Throughout history, ‘things are going to get worse’ has been predicted almost continually. However, we always seem to find a way in the long run, despite the odd blip. I suspect this time will be the same.

[1] ‘Demographics: The market impact to 2030’, Luke Templeman and Olga Cotaga

[2] OECD Library

[3] https://www.lek.com/insights/ar/global-student-mobility-trends-2021-and-beyond

[4] Macrotrends.net

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

For Investment Professionals only. Not for onward distribution. No other persons should rely on the information contained within this blog. This blog provides commentary and views on bond markets. Prepared by M&G’s bond team, this information is aimed at investment professionals wishing to supplement their understanding of these markets. Information shown on the blog should not be taken as advice or a recommendation to make an investment decision.

This weblog does not represent the thoughts, intentions, plans or strategies of M&G plc or any associated companies. They are solely the author’s personal opinion.

Inappropriate comments will be deleted or edited at the author’s discretion.

This blog may contain, or be linked to, advice or statements from third parties. M&G make no representation as to the accuracy, completeness, timeliness or suitability of such information and we have not, and will not, review or update such information and caution you that any use made of such information is at your own risk. Some of the information contained on this blog may also have been prepared or provided by third parties and may not have been verified by us. M&G hereby exclude any liability arising out of any preparation or provision of such information for this blog and make no warranty as to the accuracy, suitability or completeness of any such information.

With the exception of iviewtv.com, the links we provide from this blog to other websites are provided for information only. We do not assume any responsibility or liability with respect to any website accessed via our blog. We do not monitor or review any of the websites accessible through these links. Once you have used these links to leave this blog you should note that we do not have any control over that other website. We therefore cannot be responsible for the protection and privacy of any information that you provide whilst visiting such websites and such websites are not governed by our Terms & Conditions. You should exercise caution and look at the privacy statement applicable to the website in question.

The presence of any advert on this blog is not an endorsement by M&G of the goods, services or website advertised.

No liability is assumed for any use, or misuse, of the information presented on this blog.

As you are probably aware, internet email cannot be guaranteed and is not secure. We recommend that you do not send any confidential information to us by email. If you choose to send any confidential information then you do so at your own risk. Instructions sent by you via email, and to this blog, are processed exclusively at your risk.

Whilst M&G uses every reasonable effort to maintain the availability of this blog we cannot guarantee this. This blog may also change from time to time and we cannot guarantee the continuation of the services offered through it.