In the latest of our editorial series, Link, AIQ brings members of Aviva Investors’ investment strategy, equity and debt teams together to discuss the prospects for financial markets and the world economy in the face of the coronavirus epidemic.

In the latest of our editorial series, Link, AIQ brings members of Aviva Investors’ investment strategy, equity and debt teams together to discuss the prospects for financial markets and the world economy in the face of the coronavirus epidemic.

On December 31, China alerted the World Health Organisation (WHO) to several mysterious cases of pneumonia in Wuhan, a sprawling city of 11 million people and capital of the central province of Hubei. The majority were linked to the city’s main seafood market, which has a thousand stalls selling not only fish, but chickens, venomous snakes and even bushmeat.

A week later, officials announced they had discovered a new virus, which they named 2019-nCoV and was identified as belonging to the coronavirus family, which includes Severe Acute Respiratory Syndrome (SARS) and the common cold.

By the end of January the virus had spread to all 31 Chinese provinces as well as 25 other countries. As of February 17, there were over 71,000 confirmed cases of the virus globally, the vast majority in China – nearly nine times as many as were infected by SARS. Almost 1,800 people are known to have died.

Wuhan, one of the country’s biggest manufacturing hubs, is not alone in being in virtual lockdown. Authorities in Shiyan, another city in Hubei, are reported to have instituted “war-time measures,” with only those actively involved in fighting the virus allowed to leave their homes.

Beijing is now faced with weighing the trade-off between containing the virus and keeping the economy running. The decision has been complicated by the timing of the outbreak as millions of people had already travelled to their hometowns to celebrate Lunar New Year. Given various levels of lockdown currently being enforced in most provinces, and with numerous roadblocks, travel restrictions, and bans on the reopening of factories, offices and shops in place, a high proportion of these individuals now find themselves stuck.

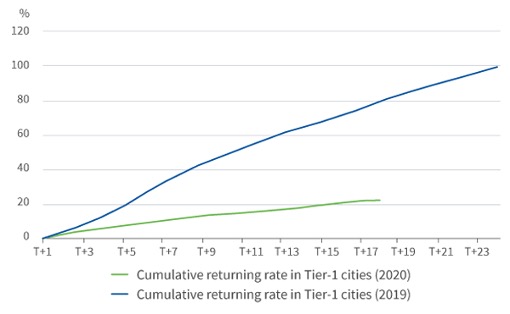

Figure 1: Cumulative return rate of workers in Tier-1 cities

Note: First day of Lunar New Year defined as T. Source: Nomura

At this stage, with little hard data to go on, markets are struggling to weigh up the near-term outlook, let alone the longer-term consequences of the epidemic. However, with many businesses having now been closed for an extended period, combined with reduced consumer footfall, there is a clear risk economic growth in China will have all but evaporated, and potentially even contracted, in the first quarter, relative to the previous three months. That is on the assumption the virus is brought under control quickly. Should that not be the case, the economic hit could be much worse.

While the price of Chinese shares and other selected financial assets has fallen in the wake of the outbreak, the majority of asset prices elsewhere have been remarkably stable. The MSCI World Index of global equity markets remains within touching distance of a record high hit on February 12. The prevailing view seems to be the virus will be brought under control relatively quickly in China, is unlikely to turn into a global pandemic, and that easier monetary policy in China and elsewhere will help repair much of the short-term economic damage.

Whether that is too optimistic an assessment remains to be seen. Aside from manufacturing, retail and tourism are likely to be among the sectors worst affected.

With China now accounting for around 16 per cent of global output, the economic damage resulting from coronavirus could ripple far and wide even if other countries are successful in limiting its spread. On February 11, Federal Reserve chairman Jay Powell said the US central bank was “closely monitoring” the risks to the US economy; two days later the European Commission labelled it a “key downside risk”.

China has in recent years become an increasingly important market for a host of multinational companies. French drinks giant Pernod Ricard has slashed its forecast for full-year profit growth by about half, largely as a result of the virus.

The crisis is proving especially problematic for automakers, many of which now boast operations in China. Japan’s Honda has been forced to shutter operations at one of its two Chinese plants, in Wuhan, while a raft of other automakers – including Nissan, Volkswagen, BMW and PSA – have also halted production.

Apple is another company that is being affected. It warned on February 17 “worldwide iPhone supply will be temporarily constrained”, while store closures have hit sales within China. Foxconn, which supplies iPhones, has yet to reopen its largest Chinese factory in Shenzhen's Longhua district. And according to reports, with three other suppliers having also been forced to close plants, Apple’s plan to ramp up production of AirPods, one of its best-selling products, could be delayed.

The AIQ editorial team brought together head of investment strategy and chief economist Michael Grady (MG) and Alistair Way (AW) and Liam Spillane (LS), heads of emerging market equities and debt respectively, to discuss the dangers posed to China’s and the world economy and to try to assess whether the risks are fully priced into financial markets.

AIQ: How big an impact is this likely to have on both the Chinese and world economies? And what about financial markets?

MG: At this stage, nobody really knows the answer to those questions as we don’t have any hard data to look at. Probably the first sense we’ll get is when we see the Chinese PMIs for February, which will be in the last week of February. How far they decline is anyone’s guess at this stage, but they could be down significantly.

Most people are currently assuming this is a short-lived event, with the worst of the economic impact seen by the end of the first quarter. Over the calendar year as a whole, the impact at this stage is expected to be fairly minimal, with most analysts having only shaved 0.2-0.3 percentage points off their estimates for China’s growth rate over the year as a whole.

There is a possibility that the situation is far worse than we think, or that the spread of the virus gets much worse before things start to improve. Either would rightly be taken badly by markets.

AW: With so much of China having been shut down for Chinese New Year, it is challenging to ascertain how much damage there is. But we are blessed with lots of anecdotal company contact and broker observations, and it does feel like there has been a major impact on economic activity. With two-thirds of department stores having been shut and travel down dramatically, it feels like the impact will be bigger than some people expect.

While some of this lost activity can be clawed back, some of the consumption, or service or travel-related activity, has gone for good. We’re seeing a demand impact on Chinese retail, but also a massive supply impact. There’s not much slack. It strikes me that compared to the SARS episode, when the peak-to-trough equity market reaction was about the same, supply chains are now much more sophisticated, integrated and sensitive.

That said, many shares in China and other emerging equity markets have discounted an awful lot of bad news. If you look at some of the Chinese companies most directly exposed to travel, retail, or gambling activity, they are down more than 15 per cent. That looks excessive because even if activity declines to virtually zero, I’m convinced the long-term value of many of these businesses remains intact.

LS: The reaction in emerging debt markets has been relatively muted, albeit conditions have been more volatile than usual. But that is perhaps not so surprising given uncertainty as to the eventual impact. In one or two cases we have seen some froth removed from markets. But investors are already talking about that having created buying opportunities, and are not just seeing the risks, especially where the economic fall-out is expected to be small.

MG: If you look at baskets of emerging market currencies, they have held up remarkably well.

LS: That’s true, although it masks a fair amount of divergence between currencies. The Mexican peso for instance has performed very well, particularly as it is typically seen as one of the higher beta (riskier) currencies. On the other hand, the likes of the Thai baht have been impacted more, reflecting the fact Thailand is a popular destination for Chinese tourists.

IQ: To what extent has accommodative monetary policy mitigated the impact on global markets?

MG: The market was certainly looking for China to respond in all ways possible – not just in containing the spread of the virus, but in ensuring they are supporting the economy. If they hadn’t injected the liquidity they have [in early February, the People’s Bank of China announced almost US$250 billion of liquidity measures], I suspect we wouldn’t have markets where they are today.

LS: The policy reaction has been pretty swift and broad across Asia. You’ve seen the Philippines, Thailand, Singapore, India, all either making policy adjustments or suggesting they will. And that comes after China’s liquidity provision, acceleration of infrastructure based fiscal stimulus and policy rate cuts over the last couple of weeks. So the direction of travel is obvious and broad across the region, and that is directly related to concerns around the virus.

AIQ: The reaction in developed markets has been relatively muted. Are people right to be looking past any short-term pain, or are investors too complacent?

AW: Apple’s share price has doubled over the last year, which is incredible for such a mega-cap company. Until its profit warning, there had seemed to be a disconnect between Apple’s share price and that of its suppliers. Take Taiwanese group Hon Hai, otherwise known as Foxconn, which is the world’s biggest manufacturer of iPhones, and indeed phones overall. Their plants are located in Zhengzhou province, just above Wuhan. When the share price reopened after Chinese New Year it was down ten per cent in one day. It hasn’t really recovered since then.

Even though it has production facilities in Wisconsin and India, there is no way Apple can shift iPhone production easily. Likewise, across other parts of the smartphone and headphone supply chain in China, we have seen a pretty savage reaction. On the whole, I’d be still optimistic many of these companies can get back on track. As the company itself told us, it was lucky this happened in February rather than October, because for consumer electronics it is a quiet time of year.

Nevertheless, it is interesting investors in the companies that make these products are more concerned about the short-term supply chain impact than investors in Apple itself. After all, there is no easy way Apple can shift iPhone production away from Hon Hai because it is so efficiently set up with customised facilities. Moreover, demand in China for iPhones and indeed all phones has dried up, so we’re looking at a big impact on both the supply and the demand side.

Supply chains are so integrated and efficient these days, there is less flex when there is an issue in one part of the world. So that backs up the point that the short-term economic impact will be worse than has been pencilled in so far. Whether that matters – i.e. if it’s a short-term thing and we get back on track – is another point.

MG: If you look at the European market, the sectors that have been hardest hit are, first, commodities, which is obviously because China is a massive consumer. So resource stocks and oil and gas stocks have been hit hard. Travel and leisure companies have been hit, as have autos. Not surprisingly, sectors that are not really exposed to China – utilities, real estate, healthcare, telecoms, insurance – have outperformed.

AIQ: As investors, how do you approach these situations from a psychological perspective?

AW: Every investor is poring over this on a daily basis. We have to look at opportunities for mispriced assets and also assess whether an existing view might have changed. The interesting thing is it feels like the pain has been more severely felt in equities than in bonds or currencies. We have some cash in our equity funds, so we have been looking to put it to work in shares that have been badly affected on fears over the virus. We have increased exposure to Macau, for example, buying more of Hon Hai, and investing in some of the more cyclical companies like Indorama and SK Innovation.

LS: At the start of the year, we had expected slightly stronger economic growth, which was encouraging greater risk taking. I suspect many investors are now looking to construct slightly more cautious portfolios. That could mean looking more closely at countries where fundamentals are better, putting on more relative-value type trades, and ensuring portfolios are built to mitigate more downside risk.

Some markets we invest in, such as Russia and Mexico, have done reasonably well. We have increased exposure to the rouble as we think valuations are attractive and real yields compensate you for the risk. It is hard to gauge where valuations look right or wrong, but there are opportunities as well as risks being created. Having said that, big directional calls are much more difficult to make until we get more clarity.

AIQ: Is there a danger markets are overreacting? After all, there have been almost two million people infected with flu this winter, and over 10,000 deaths.

MG: Thankfully the mortality rate for regular flu is pretty low, it’s around 0.1 per cent, which, rightly or wrongly, authorities don’t deem sufficiently high to prevent the spread through methods other than immunisation. This virus appears to have a mortality rate of between one and two per cent, which is materially higher; that’s why when these things happen, authorities feel they have to put in containment procedures. That’s what causes the disruption: the containment, not people getting the virus.

Economically, it is the prevention of business as usual that can have an effect. That’s why it should be a temporary phenomenon, provided they can get it under control quickly.

LS: We say this frequently, but investors don’t like the uncertainty of the coronavirus, while the flu is a known issue. Without any historical precedent – SARS was different for a number of reasons – that uncertainty plays into the market psyche. That said, while investors don’t like uncertainty, markets have so far been relatively insulated. But it is too early to take any comfort from that, given all that we don’t know.

AIQ: Some commentators, perhaps veering into hyperbole, have described this as a potential Black-Swan event for markets. Are they right to have done so?

LS: I wouldn’t use that language. But what I would say is most investors are very aware that valuation levels in some risk assets, such as global equities, are high by some metrics and have been for some time. And while I wouldn’t agree it could be a Black-Swan event, we have to recognise capital has flowed into slightly riskier parts of global markets, such as high yielding, hard currency emerging market debt, in reasonably significant levels over recent years. Some of those valuation metrics might not offer much compensation for risk given current uncertainties. So this is happening at a time when some of those asset markets potentially look a little vulnerable.

AW: The market reaction would probably have been a bit less severe if this had happened at the start of 2016, as there are different assumptions for earnings growth now being priced into emerging market equities, and indeed global equities. It felt on the equity side, you could tell by the market pattern there was a degree of profit taking, in terms of the types of things that were falling, rather than just the direct virus-sensitive companies that bore the brunt of the initial sell-off.

LS: Emerging-market debt has been a favoured trade for many investors for a couple of years, especially in hard currencies. It is fair to say valuations don’t give you much wiggle room for these kind of events, but again it is too early to be sure given those growth uncertainties.

Contributors

Michael Grady

Head of Investment Strategy and Chief Economist

Alistair Way

Head of Global Emerging Market Equities

Liam Spillane

Head of Emerging Market Debt and Portfolio Manager, EM Local Currency