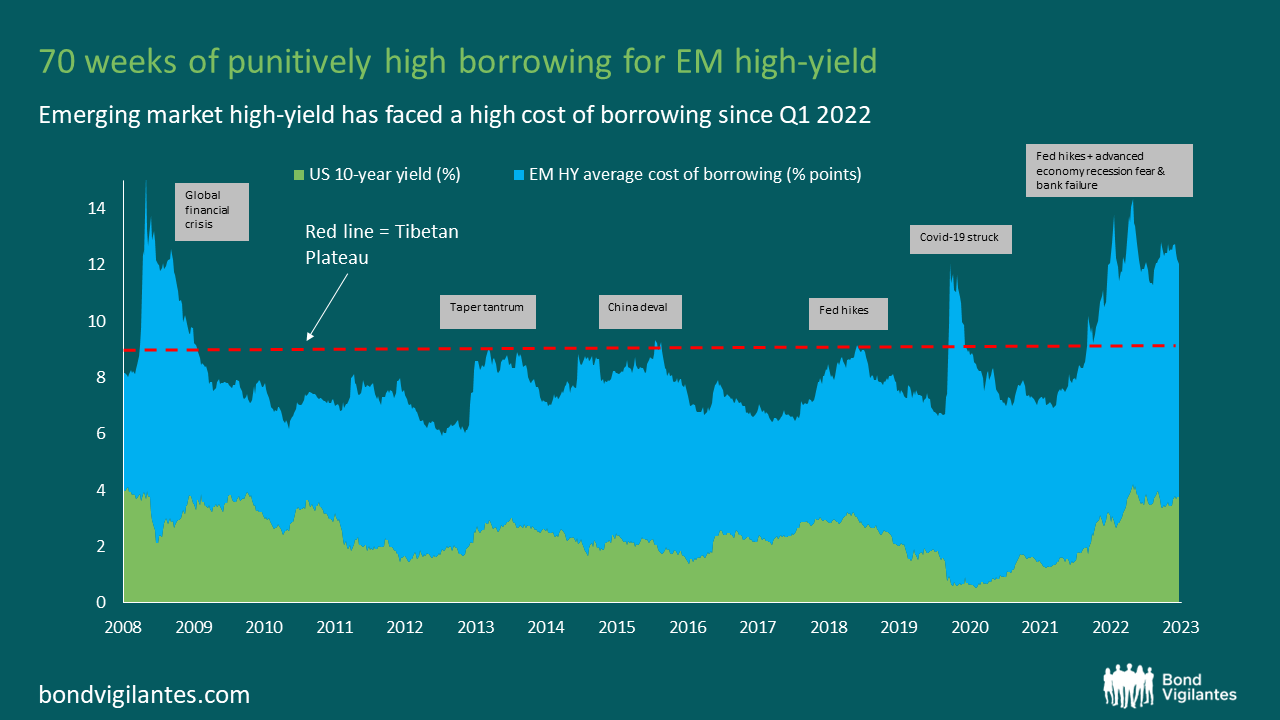

During this Fed hiking cycle emerging markets have been split into two camps. The first group includes sovereigns with investment grade credit ratings, plus the stronger double-Bs (for example, Morocco), whose spreads have not been elevated. They’ve enjoyed market access as and when they need it, albeit at a slightly higher cost than in previous years. The second group includes high-yield emerging markets, a.k.a. the ‘frontier’, who have experienced Himalayan high spreads for well over a year.

This group summited and endured the death-zone, but instead of returning to the green valley, they have instead spent 70 weeks on the Tibetan plateau of high spreads. This has meant being either shut out of the eurobond market, or having been forced to pay well over the odds to refinance eurobonds.

In July 2022, I wrote about these Himalayan high spreads, at a point when we’d had 22 weeks of prohibitively high indicative borrowing costs – for the purposes of this blog, I have defined the Tibetan Plateau as 9% or higher on a 10-year Eurobond. In June 2023, despite a recent rally, the tally had reached 70 weeks. Eclipsing the 14 weeks spent at altitude in 2020 when the pandemic struck, and even the 43 weeks in 2008 and 2009 as a result of the global financial crisis.

Source: Bloomberg, June 2023

Despite being in the death-zone, we’ve only had one additional sovereign default since July 2022 – Ghana’s over-borrowing finally caught up with them. Otherwise, there has been incredible resilience up on the plateau.

A number of sovereigns have managed to meet maturities despite the hardships. Survival strategies have included refinancing or buying-back bonds, using foreign exchange reserves (Pakistan and El Salvador), paying over-the-odds to issue (Turkey and Egypt), tendering bonds with no new debt issuance (Mongolia), or by getting the narrative right and issuing at less than astronomic cost (Cost Rica).

Despite the resilience, at these altitudes many sovereigns remain vulnerable. Those looking clearly like they have acute mountain sickness include Tunisia, Pakistan and Egypt. Each have tried to call in the IMF helicopter, but bad weather has meant there has not yet been a proper rescue.

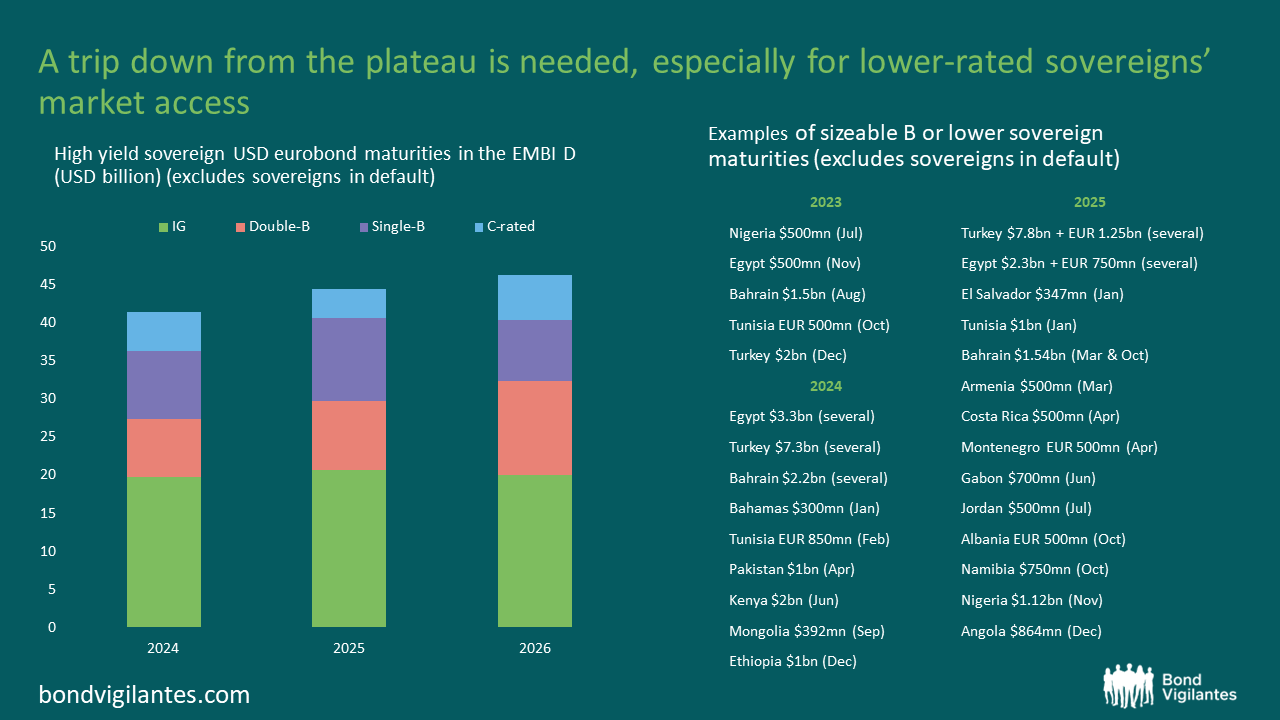

Ultimately, the only way to survive altitude sickness is to descend. More high-yield emerging market bonds will need refinancing in 2024 and 2025. This will require better weather, the Fed ending its hiking cycle and shifting gear towards lower global interest rates. Furthermore, countries that are clearly implementing reforms will have lighter loads and descend much faster.

Source: Bloomberg (May 2023)

70 weeks shouldn’t turn into 7 years in Tibet as cyclical risk-off periods thankfully don’t tend to last that long. Despite the recent hardships many frontier economies remain in good shape. While the descent from plateau will be tricky, there is opportunity in careful selection of those with lighter-loads and for whom the rescue helicopter can land.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

For Investment Professionals only. Not for onward distribution. No other persons should rely on the information contained within this blog. This blog provides commentary and views on bond markets. Prepared by M&G’s bond team, this information is aimed at investment professionals wishing to supplement their understanding of these markets. Information shown on the blog should not be taken as advice or a recommendation to make an investment decision.

This weblog does not represent the thoughts, intentions, plans or strategies of M&G plc or any associated companies. They are solely the author’s personal opinion.

Inappropriate comments will be deleted or edited at the author’s discretion.

This blog may contain, or be linked to, advice or statements from third parties. M&G make no representation as to the accuracy, completeness, timeliness or suitability of such information and we have not, and will not, review or update such information and caution you that any use made of such information is at your own risk. Some of the information contained on this blog may also have been prepared or provided by third parties and may not have been verified by us. M&G hereby exclude any liability arising out of any preparation or provision of such information for this blog and make no warranty as to the accuracy, suitability or completeness of any such information.

With the exception of iviewtv.com, the links we provide from this blog to other websites are provided for information only. We do not assume any responsibility or liability with respect to any website accessed via our blog. We do not monitor or review any of the websites accessible through these links. Once you have used these links to leave this blog you should note that we do not have any control over that other website. We therefore cannot be responsible for the protection and privacy of any information that you provide whilst visiting such websites and such websites are not governed by our Terms & Conditions. You should exercise caution and look at the privacy statement applicable to the website in question.

The presence of any advert on this blog is not an endorsement by M&G of the goods, services or website advertised.

No liability is assumed for any use, or misuse, of the information presented on this blog.

As you are probably aware, internet email cannot be guaranteed and is not secure. We recommend that you do not send any confidential information to us by email. If you choose to send any confidential information then you do so at your own risk. Instructions sent by you via email, and to this blog, are processed exclusively at your risk.

Whilst M&G uses every reasonable effort to maintain the availability of this blog we cannot guarantee this. This blog may also change from time to time and we cannot guarantee the continuation of the services offered through it.