Increasing valuations have been the main driver of stock market returns since Covid-19, but when we look over the past five years, we find a different set of drivers.

Sean Markowicz, Strategist, Research and Analytics

Schroders, 24 July 2020

Since the outbreak of Covid-19, markets have climbed a wall of worry, despite cuts to corporate earnings, forecasts and dividends.

Increasing valuations have been the main engine of returns in all markets so far this year but looking back over the past five years, we find a different set of drivers.

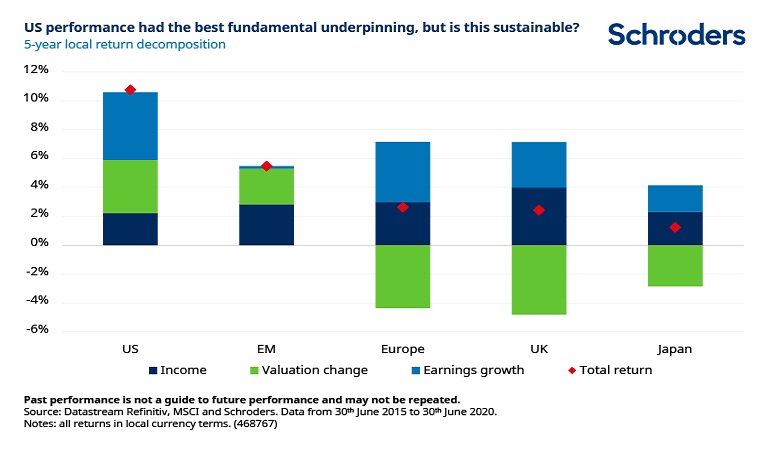

US equity market performance driven by earnings growth

The chart below breaks down local currency returns into their key components up until 30 June 2020:

- Income (dark blue bar) – dividends

- Earnings (light blue bar) – how fast have companies grown their earnings?

- Valuations (green bar) – how has the price/earnings multiple changed? Does the market now value companies more or less, for a given level of earnings?

The sum of these components equals the annualised total return of the stock market, which is shown with a red diamond.

There are several features that stand out:

- US equities have generated the highest earnings growth of all markets shown, which investors have rewarded with higher valuations. In this sense, the US had the best fundamental underpinning over the last five years.

- Emerging market equities generated the second highest total return (in local currency terms), but almost half of this came from just rising valuations while earnings growth has been next to nothing. The collapse in commodity prices and global trade are partly to blame.

- UK and European markets have been driven by a combination of modest earnings growth and dividends. Yet, the market has failed to reflect these fundamentals in valuations, which have collapsed. Brexit fears, US-China trade frictions and the pandemic have all contributed to this decline over the past five years.

- Although the US is not immune to any of these headwinds, its lower sensitivity to global trade and concentration of tech companies has meant that it has not been materially affected.

- Japanese markets achieved the lowest return. Earnings growth has been meagre while valuations have fallen against the backdrop of a sluggish economy.

Don’t forget the contribution of currency returns

When investing in overseas markets, investors take on exposure to foreign currency movements. This can add to or detract from portfolio returns. Although this is excluded from the above analysis, it can sometimes have a material impact on equity investments abroad.

For example, over the past five years, a weakening pound lowered UK equity returns for US dollar investors by 5% a year. By the same token, however, it lifted US equity returns by 5% for sterling investors.

Similarly, a strengthening dollar lowered emerging market equity returns by 2% for US dollar investors, while boosting US equity returns by 2% for emerging market investors.

Currency returns are a zero-sum game. Investors who wish to avoid such uncertainty can hedge their foreign currency holdings at a cost that is known in advance.

Rebalancing of return drivers may be on the horizon

Looking ahead, previous one-time boosts to US earnings such as corporate tax cuts are unlikely to reoccur. In fact, we may even see this policy reversed if Joe Biden, the Democratic presidential nominee, gets elected to office in November. Without this underlying earnings tailwind, US equity valuations are vulnerable to a correction.

Emerging markets also appear to be on shaky ground, as valuations have been doing most of the heavy lifting for returns. On the other hand, countries such as China, Taiwan and South Korea, which represent roughly 60% of the emerging markets index, have largely reopened their economies with minimal disruption, following several months of stringent lockdown measures. If this trend holds, a rebound in earnings could be on the cards.

Dividends have provided a solid base for UK and European equity returns, which have been supported by earnings growth. However, the global recession has forced many companies to drastically cut dividends by at least 20% or more, while analysts have cut long-term earnings forecasts. Although this has removed a key layer of support for future returns, much of this is already reflected in current valuations, which have room to recover.

As for Japan, analysts are sanguine about corporate profits over the coming years, as expectations of a swift economic recovery have surged. For example, over the past month, the forecast for long-term earnings growth has almost tripled from roughly 4% to 11% a year. If investors have conviction in this profit recovery, the potential for positive contributions from all factors remains possible.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.