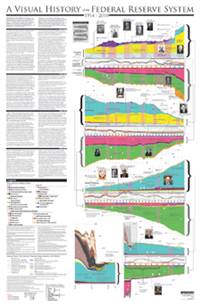

The Visual History of the Federal Reserve System, 1914-2010 portrays the Fed's balance sheet from founding to the present, as well as interest rates, reserve requirements, recessions, chairmen, US presidents, major events, and more. This is the first time this data has ever been compiled and portrayed in a single graphical display.

Financial Graph & Art

John Paul Koning

Much of the past decade's history of the Fed remains to be written, but it includes the largest expansion in the Fed’s balance sheet to date, dwarfing the WWI growth of discounts, the 1934 gold revaluation, and the WWII expansion. The expansion’s effect on employment, GDP, credit, and confidence in the dollar continue to play out.

Much of the past decade's history of the Fed remains to be written, but it includes the largest expansion in the Fed’s balance sheet to date, dwarfing the WWI growth of discounts, the 1934 gold revaluation, and the WWII expansion. The expansion’s effect on employment, GDP, credit, and confidence in the dollar continue to play out.

Several changes to the Federal Reserve Act are notable. In 1999, prior to the year 2000 date change, Section 10a and 10b advances were made eligible to serve as collateral for Federal Reserve notes, increasing the Fed’s ability to issue notes should the new century start in crisis. This was superseded in 2003 when any asset held by the Fed was made eligible as collateral for notes, removing from the Act the last vestiges of the “real bills” doctrine which originally limited eligibility to short term commercial bills. Finally, the Fed was given a new monetary tool in 2008 when it was authorized to pay interest on reserves for the first time.

The cumulative changes to the Federal Reserve Act have given the Fed the ability to act in ways it never would have been capable of in times past. When solvent banks’ demand for liquidity exploded, it was able to create facilities like TAF to meet this demand. But loans to Maiden Lane I-III, authorized under Section 13.3, have supported the questionable assets of insolvent non-banks Bear Stearns and American International Group. Section 13.3 is also the legal basis for loans made by a myriad of facilities, including the CPFF, AMLF, PDCF, and TALF (see notes in legend for definitions). At the same time, Fed purchases of government debt have fallen. Not since the early 1920s has the Fed held such a large proportion of private sector debt on its balance sheet.

On the liabilities side of the balance sheet, the low level of reserves encouraged by the 1994 introduction of sweeps, in which banks “swept” cash from checking accounts into savings accounts each night to take advantage of lower reserve requirements on the latter, has dramatically reversed. Uncertainty and a lack of confidence have led banks to accumulate huge quantities of excess reserves at the Fed rather than lending these funds out. This uncertainty has yet to be dispelled.

View Chart

A Visual History of the Federal Reserve System, 1914 -2009

John Paul Koning

Financial Graph & Art

www.financialgraphart.com