"When we look around the world, differences in stock market returns at a country level so far this year seem far more to do with the balance of sectors within each market than a particular country’s GDP."

Stuart Canning

M&G Investments, Episode, 20 August 2020

Last week it was announced the UK had suffered a bigger GDP decline than any other major European economy in Q2 2020. Though this will prompt the usual political point-scoring, many had already anticipated that the UK would be one of the worst hit, simply due to the shape of the economy:

The OECD chief economist also emphasised that it was difficult to be precise in the current situation and that the UK contraction would be similar to Spain, France, and Italy which had imposed similar lockdowns in activity.

However, the UK equity market has also been one of the weakest performers in Europe:

It would be easy to suggest that the weaker stock market is a result of the weaker economy. But we know that GDP doesn’t always tell us about corporate profits, let alone stock returns.

And if markets have illustrated anything since the end of March, it is that stock markets need not move in lockstep with economic data. Instead we need to dig beneath the headlines to unpick the sources of UK underperformance.

Errors of Composition: the role of sector weights

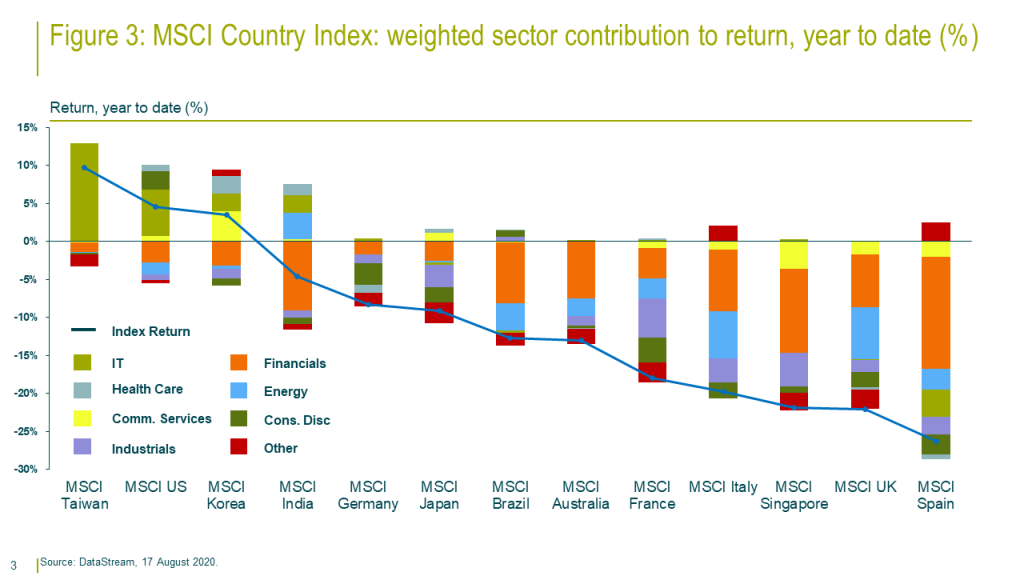

When we look around the world, differences in stock market returns at a country level so far this year seem far more to do with the balance of sectors within each market than a particular country’s GDP.

Figure three shows the contribution of various sectors to the total performance of national MSCI indices (shown by the blue line) so far this year.

Taiwan, the USA (in case you hadn’t heard), and Korea are all up so far this year, and all have seen their positive returns driven by the IT or Communication Services sectors:

Among the weaker performers, a large negative impact from financials is a common theme. In some cases domestic growth may play a role in weak bank performance, but perhaps more important will be the decline in interest rates around the world.

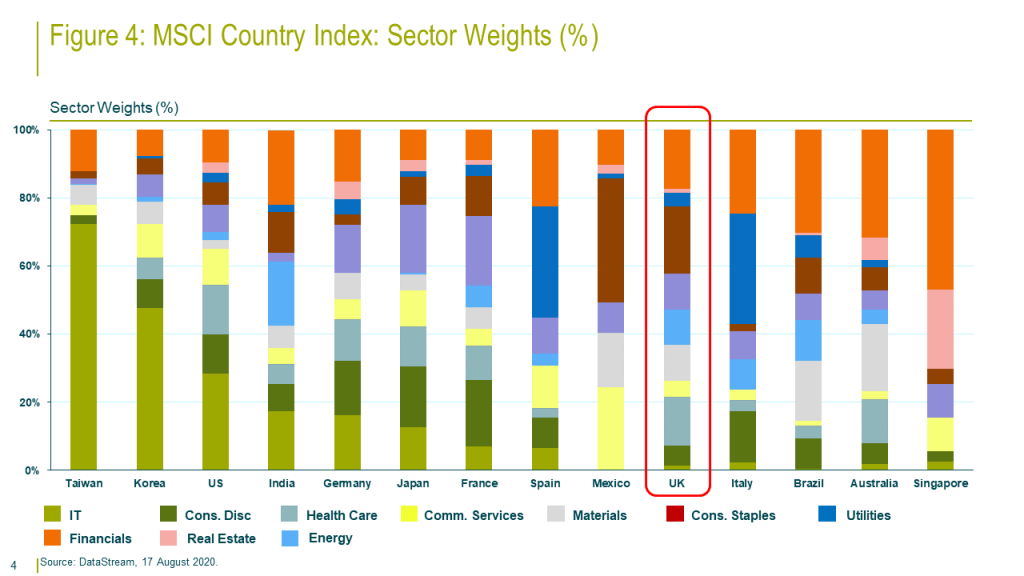

Looking at the sector weights of various stock markets below, it seems far more significant that the UK has very little IT in the index and large chunks of financials and energy:

The importance of sector mix, rather than the impact of the domestic economy will be particularly true in the UK. It is well known that the aggregate UK equity market is primarily driven by companies with global earnings bases rather than a domestic focus, with over 70% of revenues coming from overseas.

The above higlights some of the questions that the concept of ‘passive’ investing raises. Is the passive position for a UK investor to have very little exposure to IT, like their domestic index, or a very large exposure like the US (and therefore the global index)?

Insult to injury: Currency moves

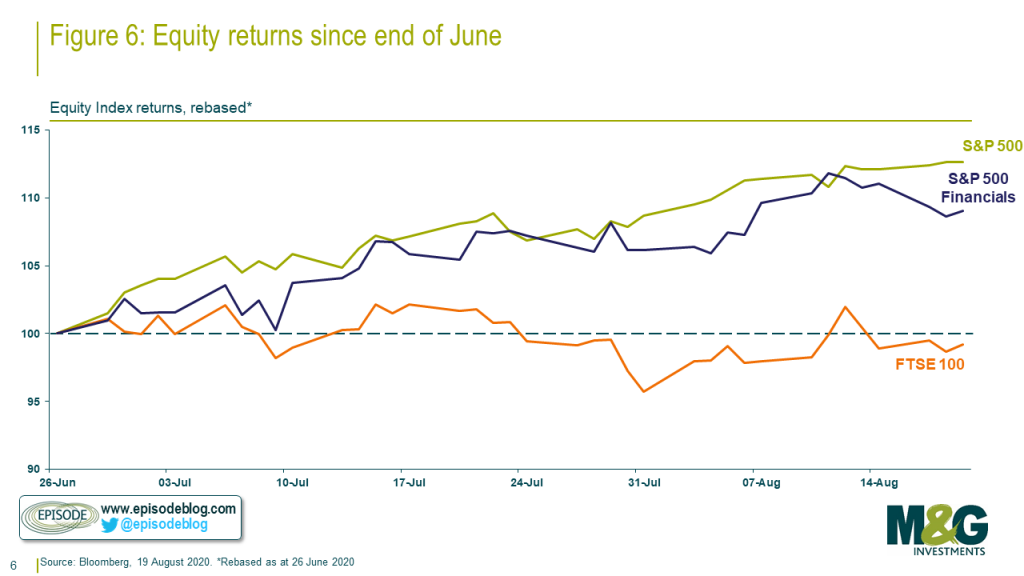

When we compare similar sectors around the world there is far less divergence than with country aggregates. Perhaps unsurprisingly, the returns on the FTSE 100 closely resemble those on the S&P 500 Financials sector this year:

However, while the FTSE 100 and US Financials have ended up at a similar place year to date, there have been phases of significant divergence. The most recent of these phases underscores the role played by another driver of UK underperformance: currency moves.

Since the end of June US financials have actually been strong but the UK market flat:

This phase coincides with the dynamic we have noted on Twitter, in which a period of material Dollar weakness has coincided with divergence in performance between the US and other equity markets (as well as the well-publicised run up in Gold).

The role of overseas earnings means that a strong domestic currency has weighed on the UK as well as markets like Germany while supporting large parts of the US.

UK Income on lockdown

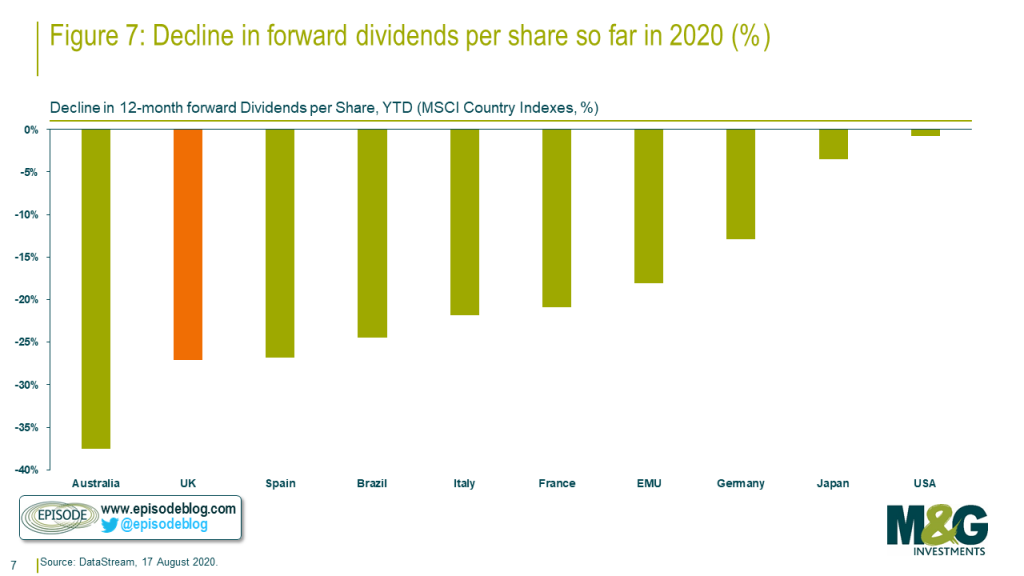

Finally, a tough period for UK investors has been especially damaging if you are on the lookout for income. The UK has seen one of the largest declines in expected dividend payments so far this year:

Clearly (as when talking about declines in GDP) these changes need to be considered in light of the starting point; some markets on that list didn’t have much in the way of dividends to cut, while the UK is traditionally a higher income market.

However, these cuts may have magnified overall equity underperformance. Investors holding for income rather than future growth may have been less prepared to take a long-term view.

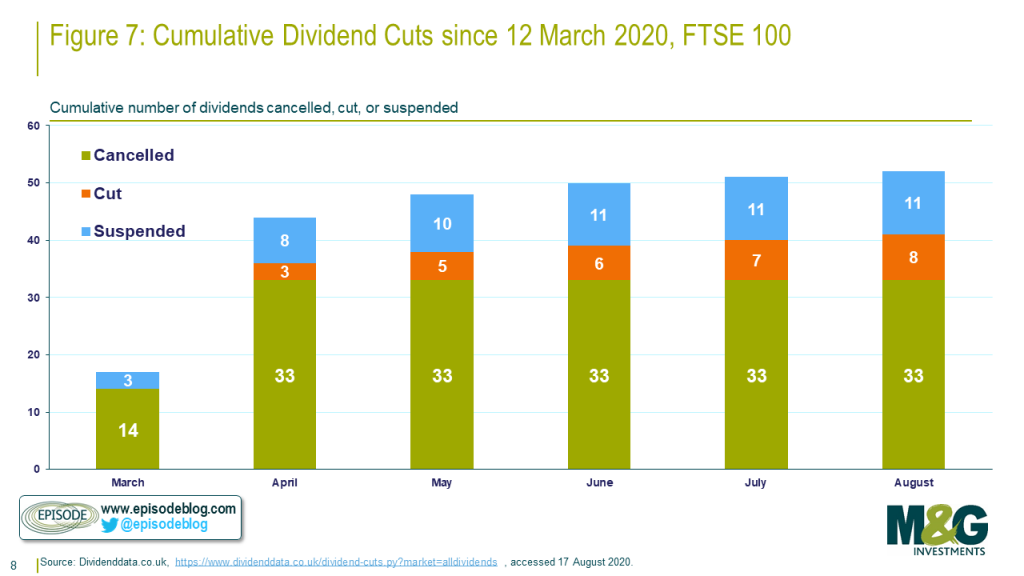

As at 31st July, around £39 billion had been removed from the UK ‘dividend pot’ for 2020 (encompassing the broader market, not just the FTSE 100). By June, the cumulative tally of dividends that had been cancelled, cut or suspended in the FTSE 100 had reached 50 (some companies will have cut more than once):

Again, the UK market will have been hit more than other areas, given the weight in banks who have taken onboard advice from the ECB and UK regulator not to pay dividends and the conditions of the furlough scheme for all companies.

These moves are entirely understandable. But for UK income investors (particularly charities clients), also grappling with Gilt yields at 0.8% before inflation, it can represent a meaningful challenge in terms of meeting short-term cash flows.

Conclusions

Just as the relative weakness of UK GDP is driven by the mix of the economy, so the weakness of the UK stock market is driven by its own composition. However the forces at play in each are not the same.

The unique circumstances of lockdown mean that we are in the unusual situation in which a period of extreme market stress has not resulted in significantly higher prospective returns, particularly for those seeking income in the near term. This represents an extreme example of the new environment for asset allocation that Dave Fishwick discussed earlier in the year (and highlights the need for diverse income sources for income investors).

It also highlights the questions raised by the notion of what ‘passive’ investing really means. Is it a passive decision for a UK investor to hold big exposures to financials, or implicit short exposure to Sterling (nice to have after the Brexit vote, more painful recently)? Or does ‘passive’ mean large exposures to the handful of US companies that dominate the US, and therefore world, indices? As we have seen in the recent strong outperformance of passive equity exposures versus most other strategies, and have experienced painfully in the UK market this year, ‘passive’ does not always mean the same thing as ‘diversified.’

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.