Before a bubble comes froth. I have been seeing froth in the domestic Chinese A-share market since May, which has since spilled over into Greater China and Korean markets.

In some sectors this froth is now turning into an outright bubble in my view, as prices appear to have risen to unsustainably high levels.

There are parallels with the TMT (technology, media and telecoms) bubble of 1999/2000 and I’m calling this one “BEVI”.

What do we mean by BEVI?

Despite all the talk of froth, BEVI is not to be confused with “bevvy” which is slang for an alcoholic beverage in my native Scotland. It’s so-called because it appears to be concentrated on stocks related to the following sectors:

- B – Biotech and any associated pharma stocks – ideally those with no revenues and just a pipeline of hopes and dreams.

- EV – Any stock that makes a widget, valve, semiconductor, battery that might be used in an electric car – and of course particularly a Tesla. It doesn’t matter if they have orders, just as long as they can talk about potential ones at an indeterminate date in the future.

- I – Internet and any tech companies that can claim they have an internet, cloud, e-commerce, working from home, mobile gaming angle. Ideally, you want companies where losses are still expanding, ideally even faster than revenues and where the model is “new” and untested, but just bound to be loved by Generation Z.

What’s inflating this bubble?

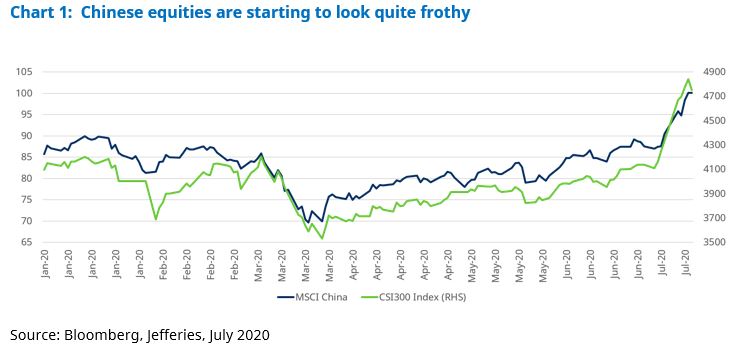

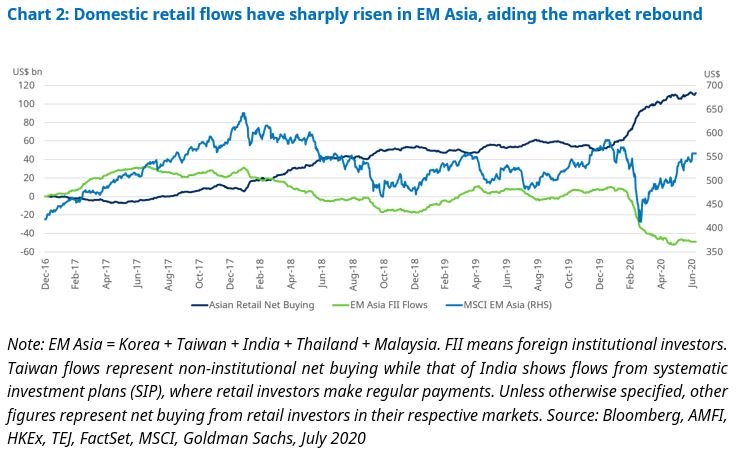

The driver of the recent moves in China and North Asia has principally been domestic retail investor flows. You can see the extent to which Chinese shares have risen in the chart below, using two different Chinese indices: the MSCI China and the Shanghai Shenzhen CSI 300 Index.

The turnaround in domestic retail sentiment in Asia has been quite dramatic and the punter on the street really has got the bit between their teeth.

On top of this, in China and Korea we’re seeing a sharp rise in margin financing (whereby brokers take equities as collateral for loans). Meanwhile, initial public offerings (IPOs, when companies sell their shares publicly for the first time) in Hong Kong are back to being oversubscribed by 200-300 times.

It’s fair to say the traffic lights are very much flashing amber – caution is warranted.

China has added further fuel to the rally, with the state-owned China Securities Journal publishing a widely-circulated article entitled “Fostering a “healthy” bull market after the pandemic is important”. This was the trigger for a dramatic increase in speculative trading earlier this month.

How big is the bubble?

The bubble is quite big in pockets and appears to be spreading.

For those readers who can recall the 1999/2000 period, the current environment will bring back memories. And of course, true to form, the ever-creative sell side are creating new valuation measures and challenging each other to come up with sillier price targets for many stocks in these sectors.

The bubble-like conditions in these sectors are quite big for some individual stocks. Biotech stocks are probably the silliest. There are plenty of examples, but a couple have stood out for us. One has quadrupled its market cap since its IPO in mid-June; it is a company that has no revenues and just a pipeline of which only one or two drugs look potentially material as of today.

There is another biotech firm in the region whose share price has risen 22 times so far this year. We’ve struggled to find much information about it, but this firm with a market cap of $6 billion appears to have 60 employees and no revenues.

How dangerous is this bubble?

Up until early July, the excesses were mostly concentrated in second tier companies, rather than the biggest players, so we were reasonably relaxed that the downside risk to the overall main indices was not huge.

However, we are getting increasingly concerned about the internet sector, particularly in China. China is c.40-50% of most of the standard benchmarks used by Asian funds and internet stocks on their own are around 40-45% of the MSCI China index. So a bubble spreading to this sector does create risks of significant market falls.

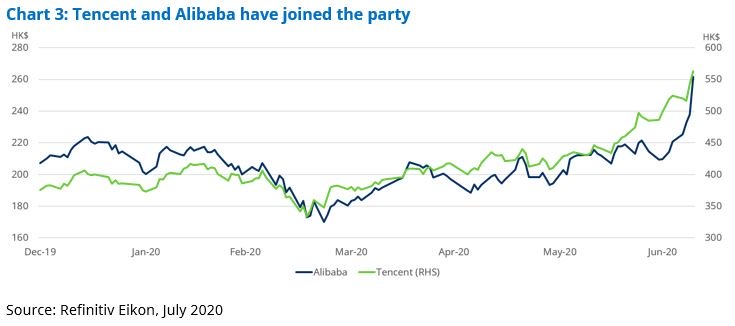

Initially, with Chinese tech giants Alibaba and Tencent not participating in the froth, we felt relaxed that overall market risks weren’t serious, but these two have now joined the party.

Fun stat of the day: in the first week of July Alibaba’s share price rose by more than the total market value of HSBC bank.

So, alarms bells are ringing. At least for Alibaba and Tencent, the network effects and investment strategies of these companies may justify some of the recent strength in their share prices.

For many other internet names, though, a clear speculative fervour has taken hold. We question whether network effects that you clearly get in e-commerce, online media etc. are really anywhere near as strong in bike sharing, taxis, food delivery, hotel booking, group buying and so on.

Certainly in the US it is very much the case that “not all internet stocks are created equal”. Will China be so different?

Going back to the rest of the market, many other sectors are moribund. ASEAN markets are struggling, Australia is doing nothing; property, banks, cyclicals, industrials, oil & gas remain very out of favour. This again is very similar to the TMT bubble. The retail investor only wants to chase hot themes and stories.

So how worried should we be and how long might these conditions last?

As highlighted above, with the froth spreading to wider areas of internet and the technology space, we are now concerned about risks to the downside for Asian markets. Our feeling, purely based on past experience of retail bubbles in Asia, is this will get bigger before it bursts.

We would expect, however, the bubbly conditions to remain pretty confined to the BEVI sector.

For those willing to look away from the herd, opportunities in Asia are to be had, such as in great bank franchises or quality resource stocks offering a 7% dividend yield…

This information is not an offer, solicitation or recommendation to adopt any investment strategy.

Any references to securities, are for illustrative purposes only and not a recommendation to buy.

Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions.

The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. To the extent that you are in North America, this content is issued by Schroder Investment Management North America Inc., an indirect wholly owned subsidiary of Schroders plc and SEC registered adviser providing asset management products and services to clients in the US and Canada. For all other users, this content is issued by Schroder Investment Management Limited, 1 London Wall Place, London EC2Y 5AU. Registered No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.