AS INFLATION EASES THIS YEAR, IT WILL BE TEMPTING TO THINK WE ARE RETURNING TO THE OLD NORMAL.

But the ancien régime of low inflation and free money is over. The adjustment process – already so painful for many investors – has further to run, and there is plenty of scope for mishaps as liquidity continues to drain from the system. The market dreams of a Goldilocks scenario, just right for risky assets. But will the bears be kept at bay?

THE DON MCLEAN CLASSIC FEELS LIKE THE PERFECT MOOD MUSIC FOR THIS YEAR’S RUFFER REVIEW.

It has been described as a song about “the nostalgia that comes with closing a chapter in time. A chapter that was good, youthful and innocent.”

When it comes to crypto, we might leave out ‘good’ and ‘innocent’. But 2022 certainly seems to mark the end of a period of exceptional growth for US markets since the 2008 global financial crisis, when falling discount rates on long duration and fantasy cashflows, large buybacks and flows from overseas favoured tech heavy US equity markets, swelling their share of the global equity pie.

BUT FEBRUARY MADE ME SHIVER

In a few years’ time, we may look back on February 2022 as the peak of US financial exceptionalism. The global system dynamic is shifting from being deflationary biased towards being more inflationary biased. The old regime was a convenient exchange, primarily between America and China: between the western desire for inflation stability and emerging markets’ desire for rapid industrial development.

This exchange had side effects: a massive monetary overhang in China, with a bloated banking system vulnerable to its unproductive assets; and hyper-financialisation in the US, with the economy over-reliant on a financial sector optimised for secular stagnation and sustained low interest rates. In other words, intolerant to inflation and higher interest rates.

Paradoxically, this intolerance to inflation generates inflation volatility and policy reactions which ensure an inflationary endgame. The more Volcker-like the appetite of the Federal Reserve (Fed) to crush inflation now, the more likely it breaks something in the financial system and the economy. That then forces a monetary and fiscal response which validates the new underlying inflationary system dynamic.

This will mean a bumpy journey, with inflation volatility. In 2022, we felt the force of a heavyweight inflation punch. Now, we’re starting to experience the recoil.

SINGING, “THIS’LL BE THE DAY THAT I DIE”

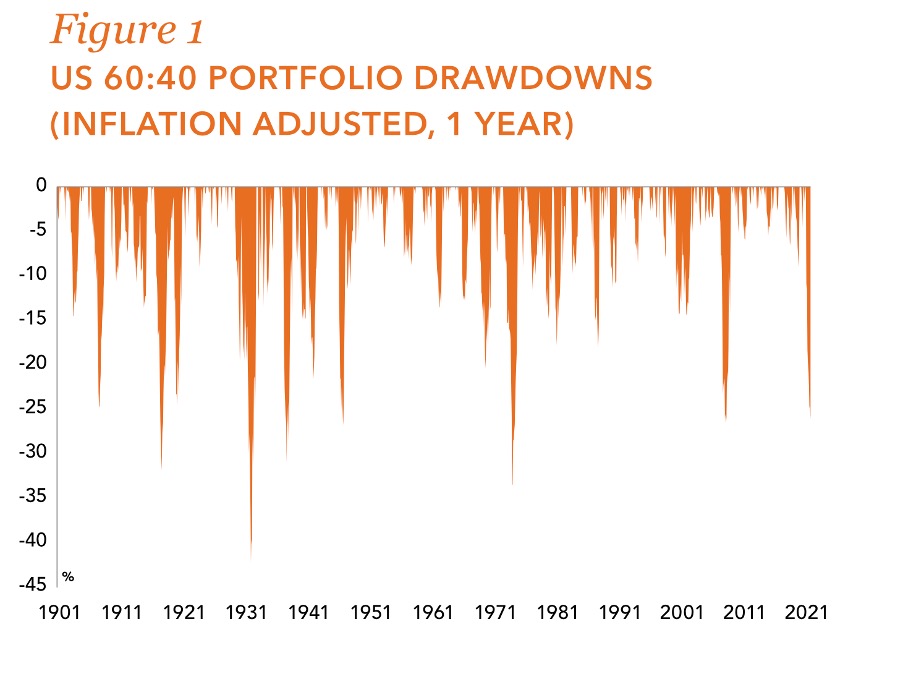

The frailty of the 60:40 portfolio (60% equities, 40% bonds) was finally exposed, as Figure 1 shows. Rather than offsetting one another, bonds and equities fell in tandem as the Fed raised rates aggressively.

US bonds failed comprehensively to protect US equity investors. It turns out that bonds protect unless they cause the equity bear market. Then 60:40 is doomed.

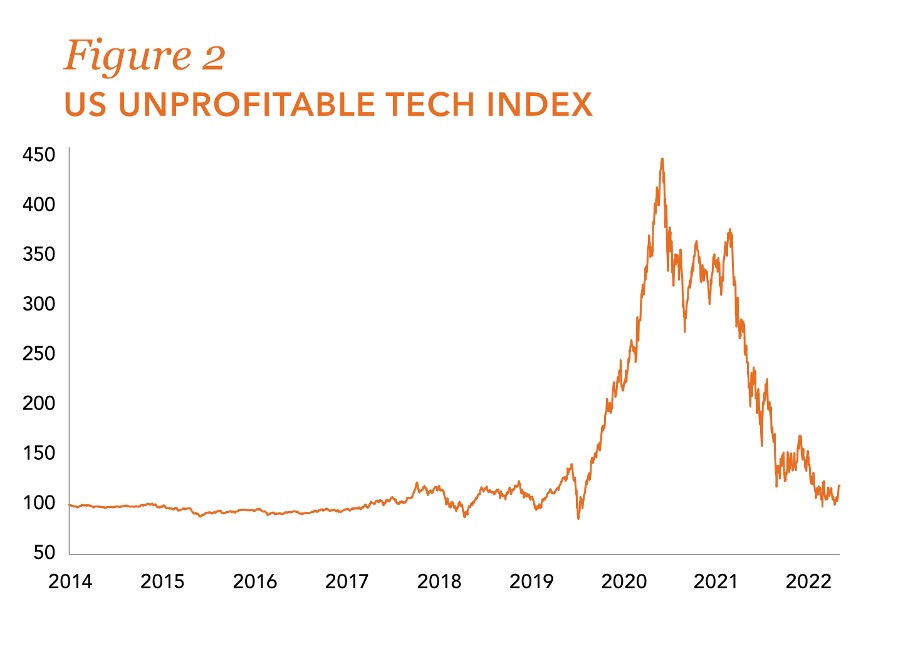

But mainstream equities and bonds weren’t the epicentre of the pain. Last year, our thematic suggestion was to be ‘short narcissism’, with narcissism proxied by ‘profitless tech’ companies. Figure 2 shows an index for profitless tech. The music definitely died for these stocks in 2022.

Source: Ruffer, Global Financial Data

Source: Bloomberg, Goldman Sachs

A GENERATION LOST IN SPACE

It was even worse in crypto land.

By the end of 2021, it had become a space where a younger generation, disadvantaged by low interest rates and high asset prices, were speculating to accumulate wealth.

In 2022, we felt the force of a heavyweight inflation punch. Now, we’re starting to experience the recoil

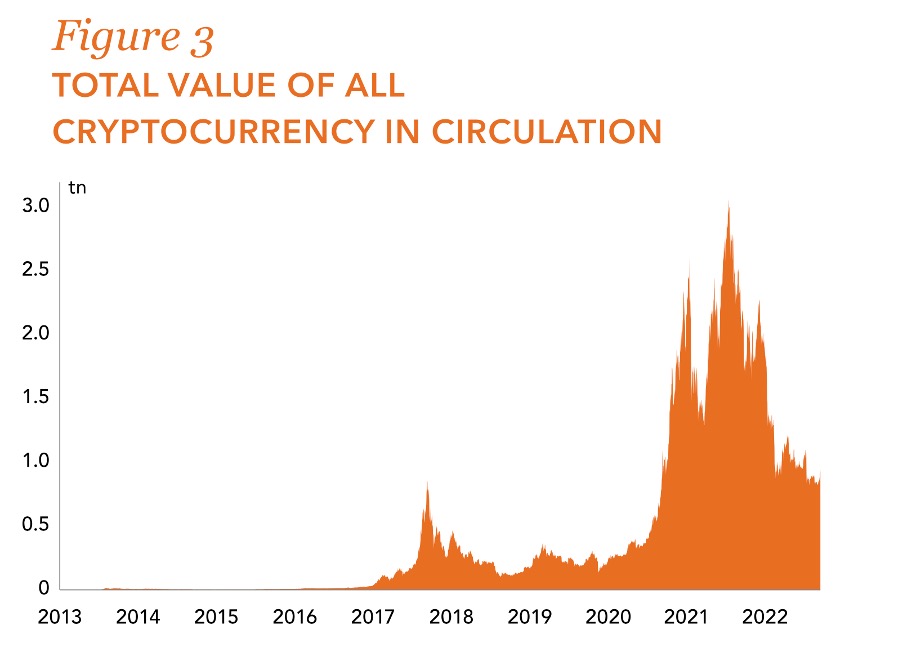

In 2022, cryptocurrencies collapsed, with the market cap of all coins in circulation plunging from $3 trillion to $850 billion (Figure 3).

Source: CoinGecko

The fireworks ignited in May when the Terra-Luna token crashed into terra firma, precipitating the failure of various leveraged players. 3 Arrows Capital got shot, Voyager never returned, and Celsius network discovered the meaning of absolute zero. Crowning all of these was the extraordinary bankruptcy of FTX. CEO Bankman-Fried: did what it said on his tin.

JACK BE NIMBLE, JACK BE QUICK

In 2022, the passive strategies which worked for so long failed, and investors were forced to flick the switch off autopilot.

Long-only investors had few places to hide. Cash, preferably non-sterling, was one, but it was subject to the decay of interest rates lower than inflation. Otherwise, you had to concentrate in specific equity sectors like energy or in individual commodities, which is highly risky.

You needed the ability to shift asset allocation nimbly and to hedge aggressively at the right moments. To illustrate the point, 2022 was the first year in Ruffer’s history when our options protection made the biggest positive contribution to the portfolio’s annual performance.

But let’s look at something that didn’t go so well: our core portfolio asset.

JACK FLASH SAT ON A CANDLESTICK

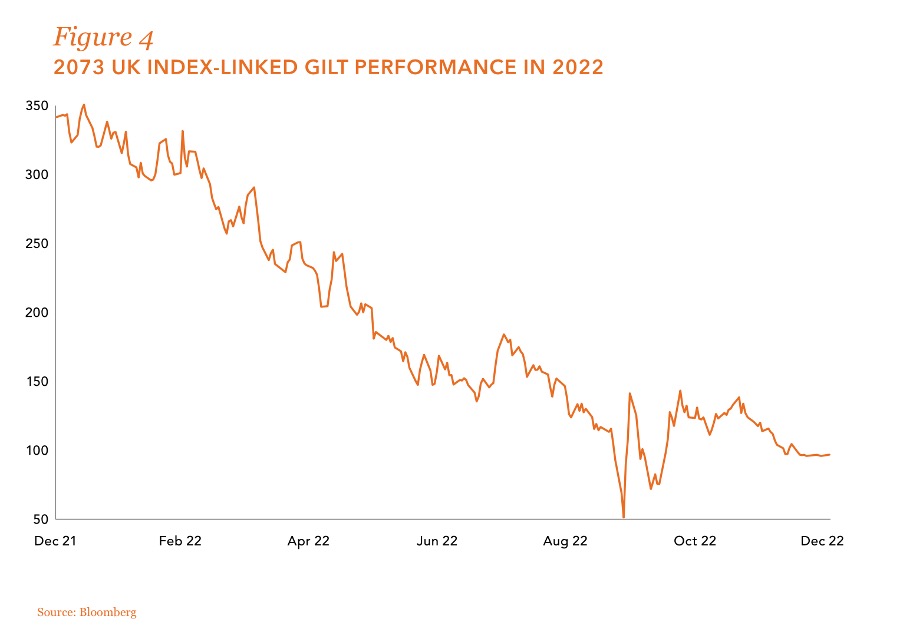

We have held UK long-dated index-linked bonds for many years. Our thesis: financial repression will be a key feature of the emerging regime, and the most powerful tool of financial repression is a negative real interest rate (ie below the rate of inflation).

But the market never allows you to hold the assets you need to survive financial crises without extreme discomfort. We were braced for volatility as the linkers transitioned from trading as long duration government bonds in the old environment to trading as real assets in this more inflationary regime.

Even so, the price action was breathtaking (Figure 4).

When inflation appeared, it was deemed transitory. When it persisted, there was a pause of disbelief. Then everyone lost their nerve.

‘CAUSE FIRE IS THE DEVIL’S ONLY FRIEND

Perhaps, fire and leverage. Markets have a knack of exposing over-leveraged positions. That’s what happened in the UK.

Former Prime Minister Liz Truss and Chancellor Kwasi Kwarteng will carry the can in the history books. However, the UK gilt market would not have dislocated so spectacularly in September but for leveraged LDI strategies. We had analysed the risk from the strategies, but we had not realised the extent of smaller pension funds’ outsourcing of derivative exposures to Irish funds with far greater leverage than would have been employed if the pension funds had done the hedging directly within the fund.1 When bond prices plummeted, the pension funds were asked to post more collateral, but they were unable to sell assets quickly enough to meet these demands. Hence, the third party funds were forced to deleverage abruptly, creating a vicious circle.

EIGHT MILES HIGH AND FALLING FAST

Ironically, just as the UK Retail Price Index showed inflation above 12%, with interest rates stuck at 2.5%, the asset specifically designed to protect against negative rates fell more than Bitcoin.

Thankfully, our hedges on interest rates, equities and credit offset the losses from the index linkers. This allowed us to trade the extreme volatility in the bonds. The end result: over the year, the interest hedges we held more than offset the loss on our linker holdings.

FOR TEN YEARS WE’VE BEEN ON OUR OWN

Until 2021, our view that the West would end up with an inflation problem was considered eccentric. It was ‘obvious’ that the forces of secular stagnation were too powerful.2 So, when inflation appeared, it was deemed transitory. When it persisted, there was a pause of disbelief. Then everyone lost their nerve. Now, the idea of a more sustained problem, even if inflation falls this year, has become consensus.

However, the paradox of our view is that it will be the instability of both inflation and policymakers’ views of it which will lead to higher average levels of inflation in the years ahead. The inevitability of inflation is likely to stem from inflation volatility.

1 Small pension funds which didn’t have the derivative counterparty paperwork in place got their leveraged bond exposure through funds which were leveraged 3-5x

2 The forces of secular stagnation: debt, demographics, peace dividend and disruption/technology

THE HALFTIME AIR WAS SWEET PERFUME

We’re at the halftime mark in the first wave of the inflation volatility story. We’ve had the up; next comes the down.

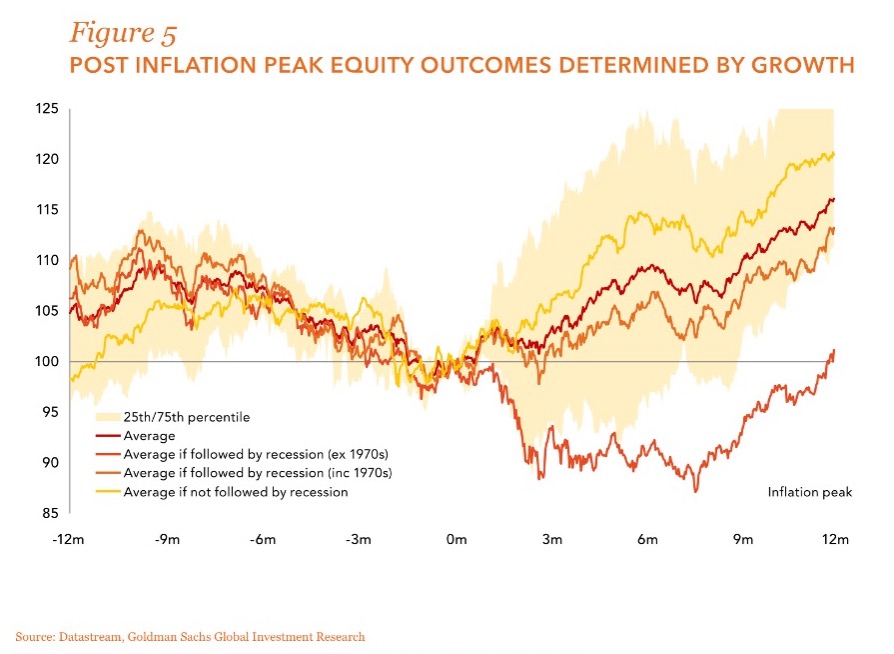

It started with sweeter smelling November 2022 CPI data than expected. Equities and bonds rallied sharply on this news. The historical justification for the rally is synthesised in Figure 5. Typically, after inflation peaks, markets rally. But the chart also shows that, if a recession follows the peak in inflation, markets continue to suffer – except during the 1970s.

If the recession is mild in nominal GDP terms because inflation (though falling) is still elevated, that supports markets, because earnings are driven by nominal GDP. Obviously, the hope is for a similar result in 2023: inflation will fall convincingly, so the Fed will not have to drive the economy into a recession. Earnings declines will be softened by nominal growth, which slows but is not deeply recessionary, and equity multiples will find support through falls in bond yields, credit spreads and the dollar. In short: a goldilocks soft landing for the economy and risk assets.

NO VERDICT WAS RETURNED

While the market appears to be pricing this goldilocks narrative, market commentators remain bearish. The yield curve is inverted, and leading economic indicators are turning down, confirming economists’ consensus of an oncoming recession. Logically, therefore, earnings estimates remain way too high.

So why did markets rally from their October 2022 lows? The rally was probably driven by portfolio repositioning by the systematic investing community.3 These buying flows would have been triggered by the first signs of cooling US inflation and labour markets, reducing uncertainty about how high US rates will rise. With less uncertainty on rates, volatility can fall, and falling volatility drives flows into risky assets. Once these flows raise asset prices and change price trends, trend following investors start buying mechanically, blind to the recession’s impact on earnings.

So what should investors pay attention to? This question gets to the heart of the hyper-financialised system. Investment flows, driven by statistics like volatility and moving averages, appear more fundamental than actual fundamentals, such as earnings outlooks. After many years of stimulus and cheap money, the prospects for cheap money and investment flows now outweigh the prospects for profits.

So, to invest in today’s markets, an investor needs to understand and anticipate changes in flows. And this requires judgements on the size and composition of balance sheets in the financial sector, particularly commercial and central banks.

3 These quantitatively driven funds tend to adjust their portfolios according to volatility and trend signals

BAD NEWS ON THE DOORSTEP

Last year, we argued that liquidity pressures posed a growing threat to financial markets and risky assets.

Central to the argument was that changes in the size and composition of the Fed’s balance sheet would be a headwind for asset prices. Quantitative tightening (QT) was shrinking the size of the balance sheet, and the growing scale of the Fed’s reverse repurchase (RRP) facility was shifting its composition; the net effect was falling commercial bank reserves. Meanwhile, regulation was constraining commercial banks’ appetite to expand their balance sheets, and strong nominal economic growth was shifting the composition of the balance sheet towards activities which support the operations of the economy and away from activities which support the liquidity of financial markets.

When inflation appeared, it was deemed transitory. When it persisted, there was a pause of disbelief. Then everyone lost their nerve.

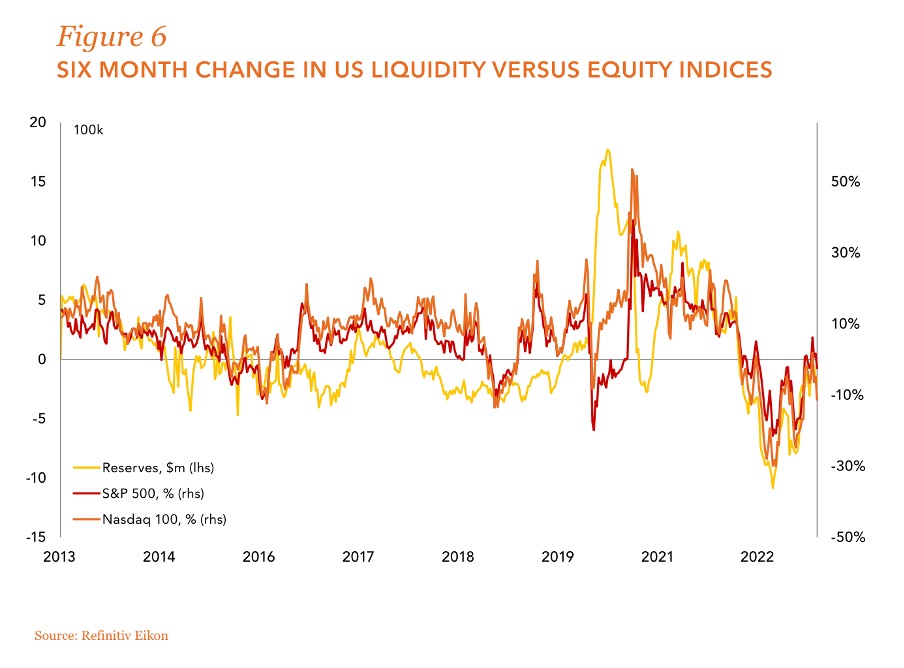

Figure 6 captures the key relationship. Changes in commercial bank reserves held at the Fed – a function of changes in the size and composition of balance sheets – have a close relationship with equity returns.

But why? Bank reserves result from commercial banks deciding to deposit money at the Fed rather than deploying it into riskier activities like loans. In theory, they should not influence asset prices. Yet, in practice, they seem to.

A paper presented at the Fed’s 2022 Jackson Hole conference suggested one explanation.4 It argues that, during QE, banks may seek to increase fees by expanding claims on their balance sheets, such as lines of credit. However, while banks tend to expand these claims during QE, they do not seem to shrink them during QT. This leaves them with less spare liquidity at stress points – for example, when a pandemic causes businesses to draw down all available credit simultaneously.

In essence, reserves are not nearly as abundant as the headline numbers suggest. So, as monetary tightening drains reserves, this bites on market liquidity sooner than expected. Precautionary demand for reserves can then amplify the tightening liquidity dynamic because reserves are considered the highest quality liquid form of collateral to meet margin calls from central counterparty clearing houses and derivative exposures when markets become stressed. This creates a ‘dash for cash’ liquidity doom loop, like in March 2020.

4 Kansas City Fed (Aug 2022), Why Shrinking Central Bank Balance Sheets is an Uphill Task

In essence, reserves are not nearly as abundant as the headline numbers suggest. So, as monetary tightening drains reserves, this bites on market liquidity sooner than expected.

THEM GOOD OL’ BOYS WERE DRINKING WHISKEY AND RYE

If your eyes are glazing over, here’s an analogy: even if the party doesn’t need more punch, you can’t drain the punchbowl, because too many partygoers have intravenous drips connected to it. Faced with the excess liquidity created by QE, the financial system has adapted in ways which make it hard to tighten monetary policy without causing financial stress.

‘Eureka!’ Don’t we have an Archimedes’ principle for financial markets? If we can predict how liquidity will behave, we can anticipate the direction of financial markets.

Sadly, predicting reserves is not straightforward. The relationship between bank reserves and markets seems to have two-way causality.

Exogenously driven changes in reserves impact markets; but market movements can also drive changes in reserves. And the relationship is even less predictable in the current monetary policy framework. That’s because the RRP facility can either dam up or release liquidity, depending on what different agents in the financial system are doing.

At times, one side of this relationship will prevail over the other. For example, if exogenous news is not supportive of markets, Fed shrinking of reserves via QT is likely to be a headwind for equities. The challenge is predicting the behaviour of the many different agents.

Even if the party doesn’t need more punch, you can’t drain the punchbowl, because too many partygoers have intravenous drips connected to it.

Depositors (retail and institutional) – will they move money from low yielding bank deposits to much higher yielding money market funds (MMFs)?

- MMFs – will they seek to invest in very short duration assets like the Fed RRP or longer duration assets like 3-12 month T-bills?

- Other investors of various flavours – will non-bank risk takers be willing to pay a premium over the Fed’s RRP rate to secure funding from MMFs, thus reducing the RRP balance sheet?

- US Treasury – how will it manage the balance of its Treasury General Account (TGA) held at the Fed? Might it engage in a treasury buy-back operation in the bond market?

- Commercial banks – will banks want to expand their gross or risk weighted assets, given current regulatory constraints?

- Regulators – will they ease the supplementary leverage ratio (SLR), which could increase banks’ balance sheet flexibility?

- The Fed – will it continue quantitative tightening into a slowing economy?

In the medium term, we think the Fed will convince markets it intends to keep rates restrictive for longer than expected while maintaining its QT policy. So bank deposits will steadily migrate to MMFs in search of higher yields. As a result, RRP balances are likely to grow or remain at high levels. The Treasury is currently running down the TGA as the debt ceiling looms but will rebuild it during 2023. And commercial banks don’t have capacity to aggressively expand their balance sheets, particularly since they are currently facilitating rapid commercial and industrial lending. All these tendencies argue for reserves to fall.

The main offset to this reserves drain comes from an increase in the risk taking appetite of non-bank financial players, which either invest their cash balances or leverage their balance sheets via private funding markets. Many are systematic investors, and this is what appears to be driving markets and reserves higher from the lows of October, triggered by the first signs of inflation and labour markets cooling.

This makes for an unstable liquidity dynamic. Liquidity can seem fine until risk appetite wanes – then suddenly it isn’t. And many more agents now influence changes in reserves than before 2008. So, when the Fed wants to adjust monetary policy, it cannot be sure how it will affect the supply of and demand for reserves.

I SAW SATAN LAUGHING WITH DELIGHT

What’s worse, the Fed can no longer rely on the US treasury market as a source of stability at moments of stress.5

In the September 2019 and March 2020 crises, the treasury market became dysfunctional, requiring the Fed to step in. This is extremely concerning, as the market is supposed to be deep and liquid, representing the global risk-free reference point for free-market capitalism. If it keeps ‘bugging’, that not only makes it hard to operate monetary policy but also unsettles the core of the capitalist system.

There are two elements to the problem, the chronic and the acute. The chronic problem results during monetary tightening in an ample reserves regime when nominal GDP growth is high and commercial banks feel constrained by regulation. Main Street lending crowds out Wall Street financing. In effect, monetary tightening discourages banks from engaging in low margin, more leveraged activities, like treasury repo and FX swap markets.

Why? Because they are balance sheet constrained, banks prefer to focus on higher margin, less balance sheet intensive activities like commercial and industrial lending, for which the growing nominal economy has demand. This reduces the liquidity of the treasury market.

5 To understand why treasury markets have become this sensitive, see Lev Menand (2022), The Fed Unbound, which analyses the shadow banking problem

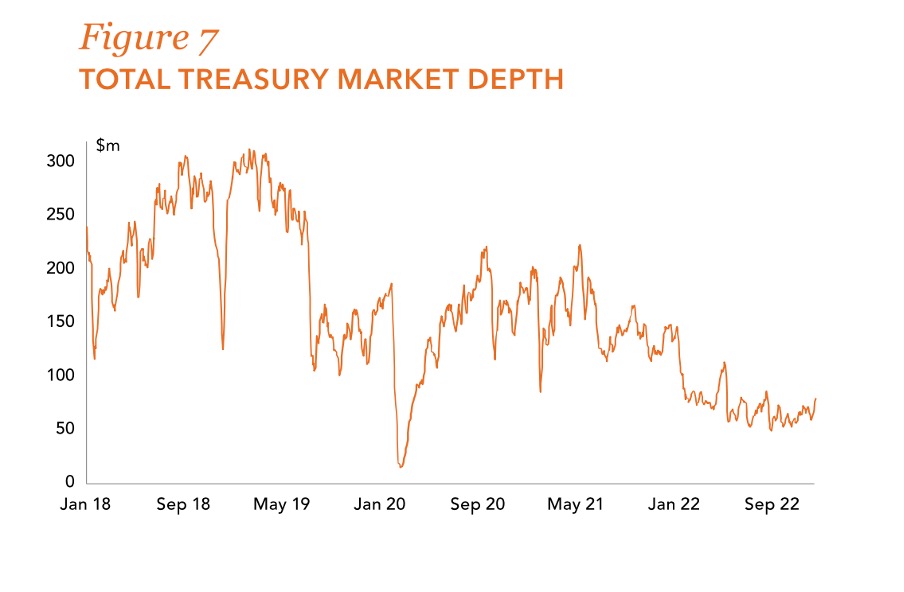

THE LEVEE WAS DRY

The depth of liquidity in the treasury market has declined through time, even as the market’s size has grown substantially (Figure 7).

Source: Goldman Sachs Global Markets Division, UST 10s, average of amount bid and offered within three levels from mid, five day average. Data to 23 Jan 2023

We can also see how the market’s depth decreases during periods of market stress (2018, 2019, 2020 and more gradually in 2022).

The acute problem arises because reserves are considered the highest quality collateral. When markets become stressed, the need for collateral increases dramatically, leading to a dash away from treasuries into reserves.

This outcome is perverse: monetary tightening disproportionately impacts the liquidity and market functioning of the least risky assets in the market, US treasuries. This makes treasuries unstable when riskier assets start feeling the effects of tightening.

So it is tough for the Fed to gauge the appropriateness of its balance sheet policy, as measured by reserves. The UK’s bond market crisis in September brought these fears to the fore once more.

THE KING WAS LOOKING DOWN

This has made the Fed cautious. At his November Brookings Institution speech, Fed Chair Jerome Powell was asked when he will end QT. After noting we were “not close to reserve scarcity”, he warned that “the demand for reserves is not stable and can move up and down very substantially” – a direct reference to March 2020’s hiccup.

The biting point of reserves is a known unknown, and Powell doesn’t want to test it too hard, because the wiring of the financial system has severely undermined his ability to calibrate policy appropriately to secure a smooth landing.

Think of central banks’ problem as like using a stick to slow a bicycle that’s careering down a hill. The Fed realises the only way to brake without putting the stick in the spokes and causing an accident is to rub the stick hard against the spokes. But even placing the stick close to the spokes has become dangerous because the axel of the bike (the treasury market) becomes unstable just as the stick starts to twang against the spokes.

So the Fed has to hope the road ahead changes from downhill to sufficiently uphill. But, because of our hyper-financial system, if it stops braking too soon, the hill may become less steep and not slow the bike enough. Braking both slows the bike and reduces the gradient of the road ahead. Who wants to ride that bike?

Think of central banks’ problem as like using a stick to slow a bicycle that’s careering down a hill.

CAN MUSIC SAVE YOUR MORTAL SOUL?

Can the Fed do anything to help liquidity in the treasury market when it gets stressed?

Yes. If forced to, the Fed and the US Treasury have options to ease stresses without having to stop QT.

The two most prominent

- Exempting treasuries from the calculation of leverage in SLR calculations. In effect, this would allow banks to expand their balance sheets to buy treasuries without having to put up more capital. This would undoubtedly supply a lot of liquidity to the treasury market, but it would probably be seen as helping the banks.

- Issuing short duration T-bills in order to buy back longer duration treasury bonds. By removing duration from the markets, this would probably be viewed as monetary easing, which runs counter to the Fed’s stated ambition of vanquishing inflation.

The effect: a treasury market put.

THAT’S NOT HOW IT USED TO BE

Indeed. Investors have grown accustomed to the idea that the Fed cares about the equity market. The Fed put. But that was in the disinflationary regime when tightening financial conditions would suck any inflation out of the economy fast. If equity prices fell too far, the Fed could ease without risking inflation expectations becoming unanchored.

Today, the economy has more momentum, thanks to the monetary and fiscal stimulus during the pandemic. So, especially given banks’ preference for Main Street lending over Wall Street financing, greater tightening of financial conditions is needed to slow things down.

But, if a proper tightening of financial conditions destabilises the treasury market and threatens financial Armageddon, policymakers will intervene. Hence, the treasury market put. How might this play out?

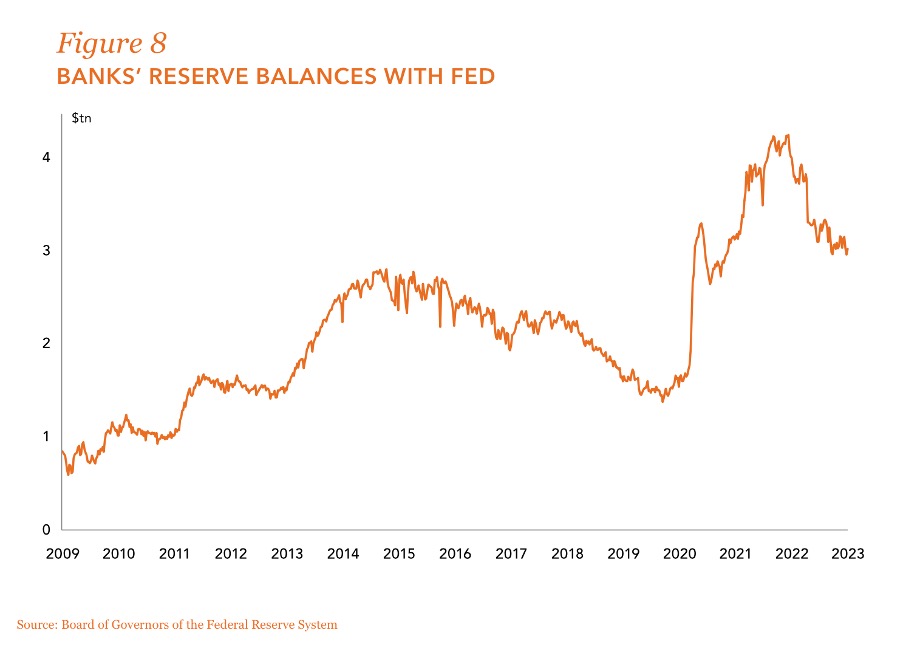

The Fed continues with tight monetary policy and draining of reserves until it gets closer to what it considers the biting point. In 2019, it turned out to be $1.4 trillion, well above the expected $800 billion (Figure 8). Various commentators and ex Fed governors have suggested the biting point today is $2-2.5 trillion. That implies between $600 billion and $1 trillion of reserves drain is still possible before the Fed lifts off QT.

This drain of reserves will put pressure on risky assets. If that starts to unsettle the treasury market, expect to see the treasury market put deployed. While supportive of equity markets, it would be from much lower levels than today, and the prime beneficiary would be treasuries, not equities.

So policymakers are hostage to Goldilocks. Inflation must quickly prove transitory without needing a financial dislocation to make it so.

NO ANGEL BORN IN HELL COULD BREAK THAT SATAN’S SPELL

So policymakers are hostage to Goldilocks. Inflation must quickly prove transitory without needing a financial dislocation to make it so.

The early signs of slowing inflation have allowed the Fed to give the market greater confidence about where the peak in rates might be. But the Fed is at pains not to clarify how long rates will stay at that level. In fact, it assumes it will have to maintain peak rates for longer than the market expects.

Markets have leapt out of the frying pan and into the fire. Unless recession pours water on the flames.

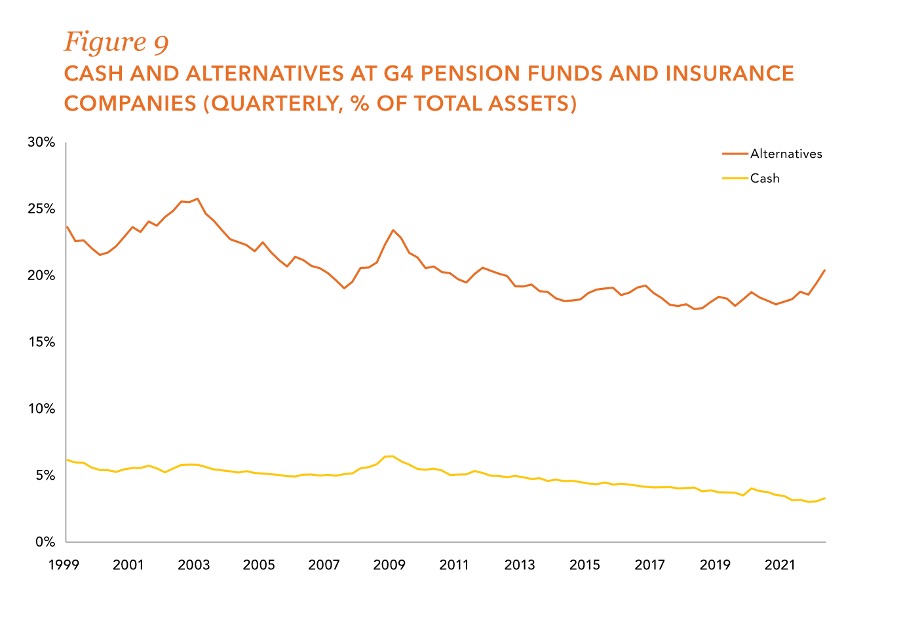

The longer we spend at peak rates, the more policy will drain reserves and the more portfolios’ asset allocations are likely to be adjusted away from risky assets, reinforcing negative investment flows.

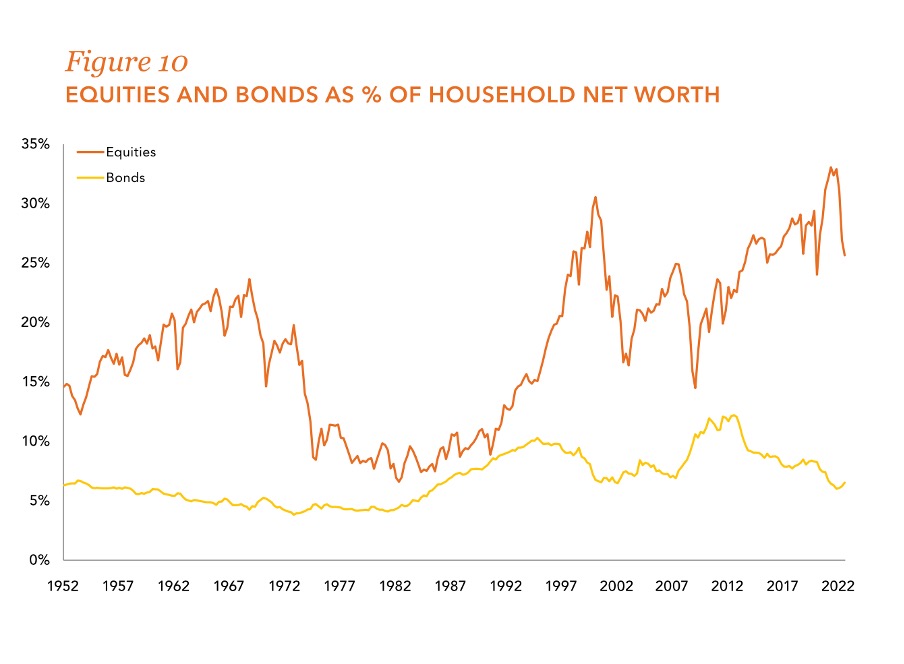

These flows don’t appear to have happened yet (Figures 9 and 10).

Goldilocks still has a lot of work to do to bail out the Fed.

Source: JPMorgan, ECB, BOJ, BOE, Fed

Source: Fed, Ruffer

DO YOU BELIEVE IN ROCK ‘N’ ROLL?

But the market wants to believe. It doesn’t mind the rock of oncoming recession because it looks through to the roll of falling interest rates and a return to cheap money. It’s all positive if recession is coming resolutely but softly in nominal terms, and disinflation (not deflation) is coming fast and loudly. This is reflected in the interest rate cuts already priced in for the second half of 2023.

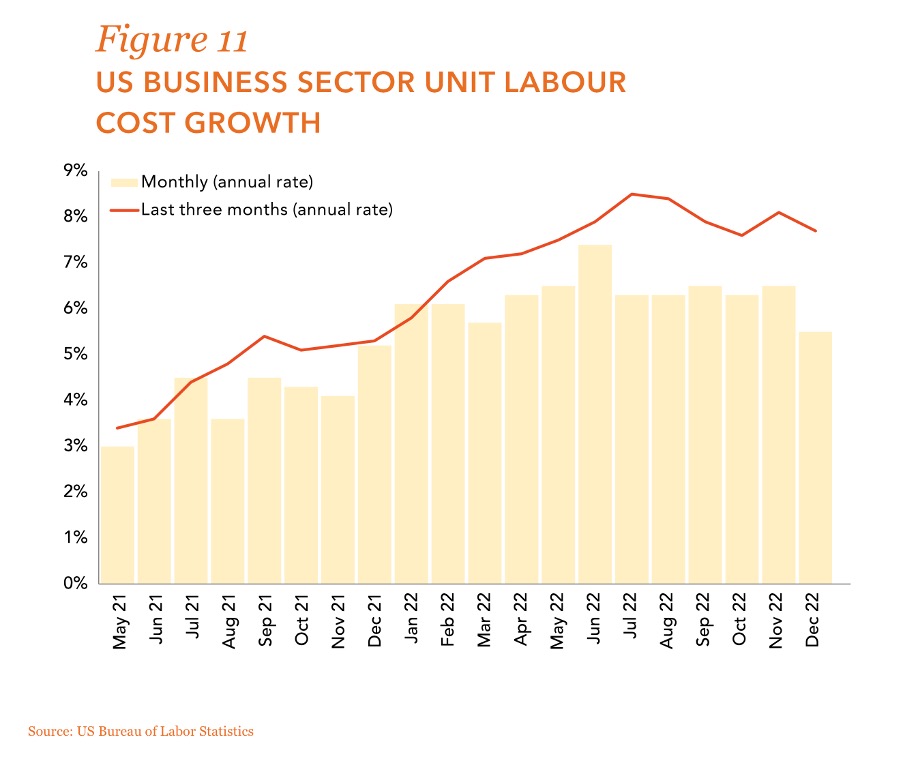

But the disinflationary trends may be slower to emerge, because of the stock effects of the massive monetary easing covid precipitated. Many leading economic indicators suggest slowing growth, but the labour market seems stickier in its hotter state (Figure 11).

So disinflation may be coming too slowly, while a profits recession is coming faster, and the Fed is going to stay restrictive for longer.

Of course, exogenous developments – including a potential resolution to the Ukraine war, the end of yield curve control in Japan and the reopening of the Chinese economy post zero covid – could affect markets for good or ill.

For now, though, the Goldilocks narrative is back. But it seems to be chasing rather than driving price action, which would be consistent with the rally being driven by repositioning and technical factors.

SHE JUST SMILED AND TURNED AWAY

It is hard to have high conviction on any particular pathway. A Goldilocks fairy tale for 2023 can’t be dismissed completely; the data and events could coincide to deliver the ‘not too hot, not too cold’ outcome. But it’s a walk in the dark through a dense forest to get there and, even if we do, a Goldilocks economy does not guarantee a Goldilocks outcome for corporate earnings. ‘Just right’ for the economy might still equate to ‘cold porridge’ for corporate profits if margin pressure bites. And cold porridge won’t keep the bears away.

Liquidity remains a key consideration. It is difficult to call an end to the bear market whilst the Fed is still draining reserves.

This is a function of explicit balance sheet policy, QT and interest rates, which motivate savings to shift from bank deposits into MMFs.

Predicting the short run pathway of reserves is difficult, but we know the effect and intention of policy is to shrink them further. While that remains the policy, risk-on interludes and Goldilocks narratives should be treated with caution. To get bullish, we need to see a proper Fed pivot, not a Fed pause. We need confidence in interest rate cuts and QT being paused. Or deployment of the treasury put.

SINGING, “THIS’LL BE THE DAY THAT I DIE”

In the end, inflation will fall down and play dead in 2023 even if it doesn’t fall fast enough to bail out markets from the Fed’s liquidity drain.

When inflation has fallen, many will think we can return to the pre-covid regime. That would be a mistake. The system is now more capable of generating inflation than the prior regime conditioned us to believe.

Here’s how this might unfold. Fiscal policy has proved effective at stimulating the economy directly, rather than relying on monetary policy to be transmitted via Wall Street, with all the inequality that generated. Unfortunately, the UK’s recent experience has scared governments, so fiscal policy is unlikely to be used pre-emptively. Unemployment will first have to overtake inflation as the political issue of the day.

When stimulus comes, it is likely to take the form of industrial policy, reflecting the growing strategic competition with China. Spending will be targeted at strategic industries, defence and the energy transition.

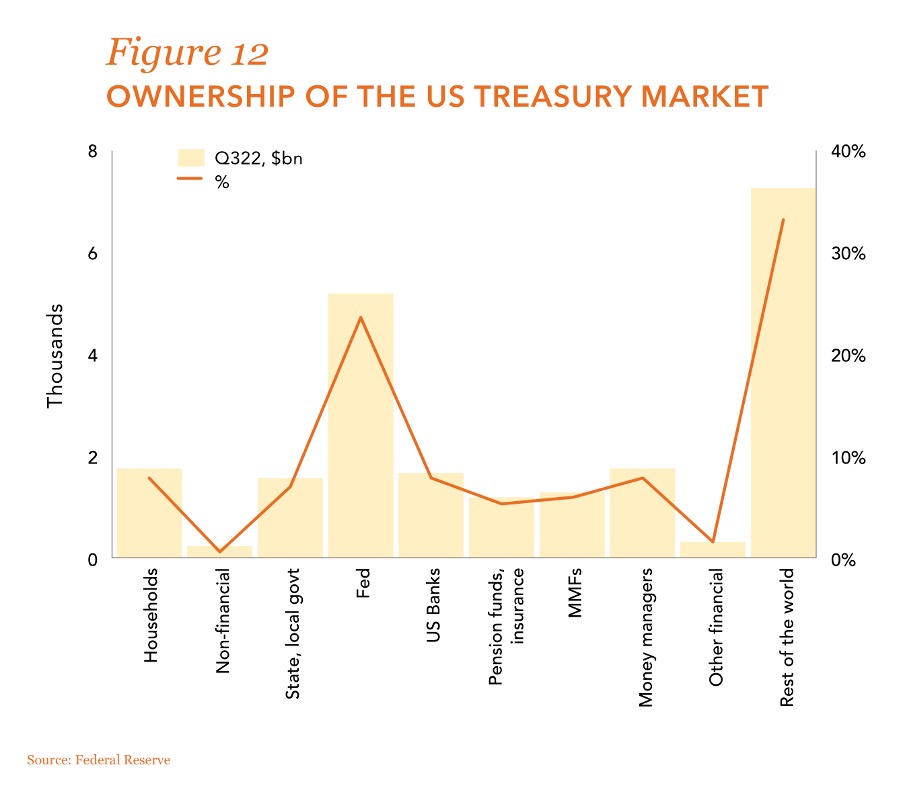

In the US, the treasury market will need to be relied upon as a source of stable funding. Currently, foreign owners dominate the market (Figure 12).

Domestic ownership of US bonds will probably have to increase, with banks and their broker-dealers needing to own more and intermediate more. So I expect policymakers to reduce balance sheet constraints to improve liquidity and let banks own more bonds.

Because all governments face the same strategic challenges, industrial policies are likely to direct resources at similar things. Consequently, when policy turns stimulatory again, we’re likely to revisit supply side constraints and bottlenecks. Geopolitics will also keep throwing in disruptive curve balls, whether in the South China Sea, the Middle East, Pakistan or around Russia.

Given our experience with inflation over the past two years, we are all now primed – psychologically and behaviourally – to anticipate it. So the inflationary tinder will catch alight much more easily next time conditions are conducive.

This inflationary dynamic will be unique in one important respect. It will be like the 1960s-1970s inflationary dynamic but in reverse: this big initial inflation wave will be followed by waves which are successively smaller but on a rising trend.

We are also likely to see more currency crises. As the UK’s experience shows, currencies will be punished hard when policies are out of synch with US policy and domestic inflation trends.

So the dollar is key to policymaking. If you are a true sovereign – ie control your own printing presses – and the dollar is in a weakening trend, fiscal policy will be an effective means of stimulating the economy with less risk of stress on your currency and bonds. Unfortunately, the Truss government failed to recognise this timing aspect of its growth policy.

In summary, liquidity dynamics are the key driver of the next leg of our inflation volatility thesis. But it is the lens of inflation volatility which should shape portfolio management strategy. So the autopilot stays off. Investors will have to remain active in their asset allocation, imaginative in the tools they use and mindful of a new regime which is corrosive to passively held wealth.

For investors, it means another year when portfolios, like Tesla cars, can’t be fully self-driving.

WE STARTED SINGING BYE-BYE, MISS AMERICAN PIE

Last year, capital preservation became a much higher hurdle.

The inflation punch was hard, forcing the Fed to abandon its transitory framework and consider a new regime where supply shocks are a recurrent feature of the landscape.

So rising interest rates did the damage in 2022. The music died for the 60:40 investment paradigm, built on a system dynamic which was biased towards disinflation but is shifting to one biased towards inflation.

A lot of other hope in markets died too, as a western financial system wired for zero interest rates confronted US rates at 4.5%-5%. In a face-off between inflation and the wiring of hyper-financialisation, the latter will prevail. Falling inflation in 2023 will be the product. Whether this is supportive for markets will depend on the interplay of liquidity and fundamentals. The $2 trillion in the Fed’s RRP facility means ample liquidity is available to the system, but it can easily get trapped in that facility.

We are in a transition from peak interest rate volatility – as the market gets confident about the upper limit on US interest rates – to uncertainty over how long peak restrictiveness lasts.

The first phase of this is bullish for risky assets: declining volatility drives money back into markets, improving price trends, which triggers repositioning buying by trend following investors. In this phase, the market can dream about a Goldilocks narrative for 2023: not too hot on the inflation front for the Fed; not too cold for the nominal economy and corporate earnings; just right for risky assets.

Once this repositioning has happened, though, the dynamics of liquidity – proxied by commercial banks’ reserves at the Fed – are likely to reflect ongoing QT and the need for markets to price in interest rates remaining at peak restrictiveness for longer than currently expected. In short, liquidity headwinds are likely to reassert themselves.

For equities and credit, a positive outlook relies on a Fed pivot, not a Fed pause. Only continued disinflationary surprises could bend the Fed towards the market’s expectations of rate cuts in the second half of 2023. In hyper-financialised markets, cheap money matters more than profits; but profits still matter. Expecting Goldilocks seems a triumph of hope over realism.

More generally, equities and other risky assets face an asset allocation headwind. For investors seeking a nominal return, bonds now offer a risk-free alternative. This should result in a lower allocation to risky assets.

For bonds, tightening liquidity could provoke stresses in the treasury market as risky assets sell off. This would probably result in policy intervention. Conversely, if the data is surprisingly disinflationary, bonds will continue to rally. So, while there might be more volatility ahead, 2023 should ultimately be a good year for bonds.

For investors, it means another year when portfolios, like Tesla cars, can’t be fully self-driving. The terrain ahead will change with the interplay between liquidity and fundamentals, and impactful global developments could dash into the road at any time. Not a journey to be undertaken with passive vehicles.

In the end, wealth is getting reallocated as asset markets reorientate to the new regime.6

Bye-bye, Miss American Pie.

6 This article was drafted in late 2022

Access to Ruffer's original article.

The views expressed in this document are not intended as an offer or solicitation for the purchase or sale of any investment or financial instrument. The information contained in the document is fact based and does not constitute investment research, investment advice or a personal recommendation, and should not be used as the basis for any investment decision. References to specific securities should not be construed as a recommendation to buy or sell these securities. This document reflects Ruffer’s opinions at the date of publication only, and the opinions are subject to change without notice.

Information contained in this document has been compiled from sources believed to be reliable but it has not been independently verified; no representation is made as to its accuracy or completeness, no reliance should be placed on it and no liability is accepted for any loss arising from reliance on it. Nothing herein excludes or restricts any duty or liability to a customer, which Ruffer has under the Financial Services and Markets Act 2000 or under the rules of the Financial Conduct Authority.

Ruffer LLP is a limited liability partnership, registered in England with registration number OC305288. The firm’s principal place of business and registered office is 80 Victoria Street, London SW1E 5JL. This financial promotion is issued by Ruffer LLP which is authorised and regulated by the Financial Conduct Authority in the UK and is registered as an investment adviser with the US Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training. © Ruffer LLP 2023 ruffer.co.uk

For US investors: Ruffer LLC is the distributor for Ruffer LLP, serving as the marketing affiliate to introduce eligible investors to Ruffer LLP. Securities offered through Ruffer LLC, Member FINRA. More information about Ruffer LLC is available at BrokerCheck by FINRA. Any enclosed or attached statements or material is for institutional investor use only and eligible institutions are those defined as Institutional Accounts under FINRA Rules and is not intended to be, nor shall it be construed as legal, tax or investment advice or as an offer, or the solicitation of any offer, to buy or sell any securities. Any enclosed or attached material is provided for informational purposes only as of the date hereof and is subject to change without notice. Ruffer LLC is generally compensated by Ruffer LLP for finding investors for the respective Ruffer LLP funds it represents. Ruffer LLP is a registered investment adviser advising the respective Ruffer LLP funds, and is responsible for handling investor acceptance. Any information contained herein, including investment returns, valuations, and strategies, has been supplied by the funds to Ruffer LLC and, although believed to be reliable, has not been independently verified and cannot be guaranteed. Ruff LLC makes no representations or warranties as to the accuracy, validity, or completeness of such information. No representation or assurance is made that any fund will or is likely to achieve its objectives, benchmarks or that any investor will or is likely to achieve a profit or will be able to avoid incurring substantial losses. Past performance is no guarantee or indication of future results.