Is the low and range bound outlook for rates plausible in a historical context?

Robert Tipp, Chief Investment Strategist and Head of Global Bonds, PGIM Fixed Income

PGIM, January 2020

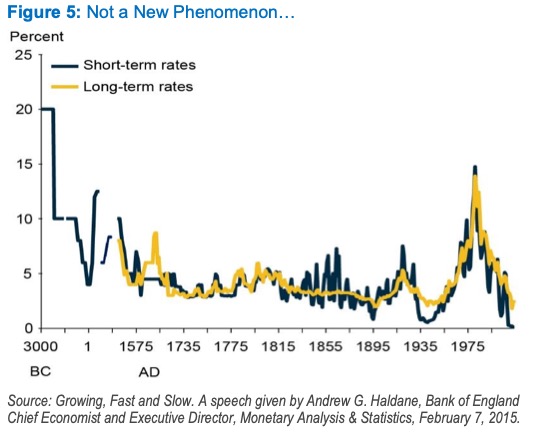

Is the low and range bound outlook for rates plausible in a historical context? In 2015, the Bank of England’s chief economist pointed out that rates weren’t just near recent lows, but were at the lows looking back over thousands of years (Figure 5). For many, the take away from the BoE research is that developed market interest rates are in fact too low, and they should revert higher.

For us, however, the takeaways from the research are: 1. the rarity of persistently-high interest rates; and 2. the extreme longevity of interest-rate trends. Since the 1890s, for example, there have only been four major trends (two bears and two bulls). Furthermore, from 1690 to 1890, there were only two major trends (one bear and one bull) over roughly 200 years.

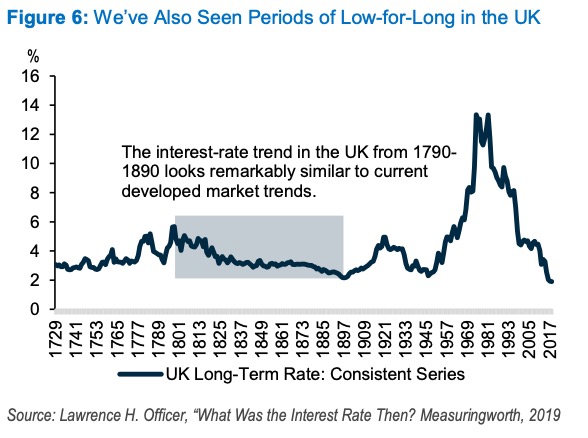

As another case in point, we turn to the UK from 1790–1890—a span that featured relatively stable central bank and fiscal frameworks combined with a general trend towards geopolitical stability—as a period that may rhyme with current conditions (Figure 6)2. Over that interval in the UK, there was one basic trend in the bond market: falling long-term interest rates, ultimately to levels similar to current rates. The business cycle and other cyclical undulations mostly manifested themselves in waves of rising and falling short-term rates. Yet, with stable long-term growth and inflation expectations, there was little impact on the overall trend in long-term interest rates.

While the UK comparison is not necessarily our vision for the next century, it characterizes our outlook for now and the foreseeable future—low and range bound long-term rates. Fundamental and technical conditions point in that direction, and, if history is any guide, a bond market trend that’s four decades old could only be half over.

2 For example, callable UK consols yielding between 2% and 3% are arguably not that different from the current yields on non-callable 30-year U.S. Treasury bonds.

@2020. For Professional Investors Only. The views and opinions of the author are as of 31/12/2019, are for informational purposes only, and are subject to change.