China Gets Snared in its Debt Trap Diplomacy

The soon-to-be hosts knew they would ultimately serve the revenge cold. Luckily, there was salt on hand to pour in the wound. Salt production was, after all, Hong Kong’s first industrial sector in the third century BC, more than 2,000 years ago. A bit more patience was required, which came easily after more than 150 years of waiting. Appearances first though. On December 19, 1984, British Prime Minister Margaret Thatcher and Chinese Premier Zhao Ziyang signed large red-bound documents with black fountain pens and then shook hands. Set in motion was a timeline for China re-assuming sovereignty over the city on July 1, 1997. The Joint Declaration was to adhere to the “one country, two systems” formula under which Hong Kong became part of a communist regime but retained its capitalistic economic system and partially democratic political system for 50 years after the 1997 handover.

The first inklings that fate might not hold with this idyllic co-existence arrived with 1989’s Tiananmen Square pro-democracy massacre. Nonetheless, in 1992, with much aplomb, Chris Patten assumed his position as Britain’s last governor of Hong Kong. That October, he announced proposals for the promised democratic reforms including broadening the voting base in elections. China is outraged at the ambitiousness and not being consulted beforehand. Two bitter years of backbiting ensued yielding watered-down legislation that fell far short of universal suffrage. By the time 1997 rolled around, most observers knew true democracy would never be achieved. The key, for the Chinese, was closing the ugly chapter that started January 20, 1841, when control of Hong Kong was ceded to the British to stand as reparations for their loss of the First Opium War.

A decade on, following many protests, retributions and international accusations of bad faith negotiating, a blueprint outlining full democracy was still in the planning stages. Buying (a lot) of time, Beijing accedes to allowing Hong Kong people to directly elect their own leader in 2017 and their legislators by 2020. Many more protests later, in June 2017, Chinese President Xi Jinping uses the occasion of swearing in newly elected chief executive Carrie Lam to issue a warning against any attempt to undermine China’s influence over the special administrative region. The strongman tactics fomented the first violent protests that only COVID-19 could temporarily repress.

A May 20, 2020 Washington Post headline reads: “An Explosive Summer of Discontent is Brewing in Hong Kong.” On May 18, Xi’s allies in the Hong Kong legislature forcibly seized control of a committee that controls which bills can be brought before lawmakers, a move to force Beijing’s agenda. The first up would make it a criminal offense to disrespect China’s national anthem. The true test will arrive June 4, a day that Hong Kong has always marked to commemorate the students who fell 31 years ago at Tiananmen Square. To try to quash this date marking the beginning of another season of discontent, Hong Kong authorities have extended the ban on public gatherings under the auspice of controlling the pandemic. With 1,056 cases in total, Hong Kong is ranked 99th in the world. In one of the world’s densest cities that has the most cross-border traffic with mainland China, four there have died, and one person remains in hospital.

But it wasn’t Lam who moved swiftly on behalf of her constituents. In fact, Lam purposefully waffled on closing the border and went so far as to order civil servants to not wear masks. In a medical and societal miracle, scarred with memories of SARS and fully organized and mobilized for the past year against their own government, the people of Hong Kong came together and devised a grass roots plan to save themselves. COVID-19 did not dissipate the resoluteness of the movement; it strengthened it.

As determined as Xi may be to exert his authority, unlike last summer, he will have to be mindful of depleting his military, political and most of all, economic ammunition. There will be no more of the West turning a blind eye as it did for the first round of protests.

More than any development in the past 30 years, China’s handling of the coronavirus threatens its visions of imperialism. While the conventional route of overt military force has not been an option, a covert building up of its military in the South China Sea and alliance-building with frenemies of the West have played their parts. But more than anything, with Hong Kong as its symbolic front man, China’s imperialist ambitions have been furthered by gaining economic control of foreign resources abroad and critical globally dependent industries at home.

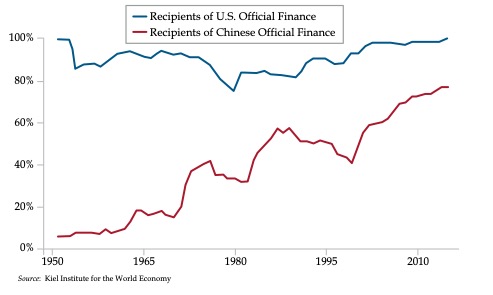

Last year, I had the honor of presenting alongside Carmen Reinhardt, one of the world’s preeminent experts on China’s quiet colonization who was today named chief economist of the World Bank. The next few charts are the product of the work she has done with the Kiel Institute for the World Economy. The biggest picture takes us back 60 years to a time when Chinese finance had virtually no global footprint and the U.S. was geographically universal. While the reach of the United States has held steady, China’s influence has risen steadily alongside its economy unseating one country after another in its march to becoming the world’s second-largest economy.

China’s Influence Has Grown Alongside its Global Penetration of Official Financing

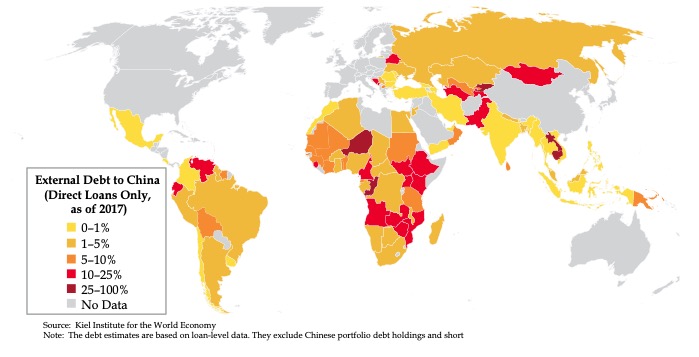

Two lines cast on two axes can’t adequately convey China’s reach. As you see on this map, it’s far easier to say that save Europe, the United States and Canada, China is just about everywhere in its capacity of lender of first resort.

Note that it does not look as if Australia is in debt to China. While that’s all well and good, it’s also because China already owns (islands) or leases (its biggest port for 50 years) such a vast amount of the island nation. That makes it odder still that Australia has taken the lead in pursuing China via an independent investigation into the origins of the coronavirus.

The question is one of motive. In 2017, an Indian think tank coined a phrase that was swiftly embraced by the media, that of China’s “debt-trap diplomacy.” In short, this form of entrapment lures third-world countries with the guise of economic development. Whether it be infrastructure or helping a country realize its resource or strategic geographic location, the “trap” part entails the repossession event if a country fails to pay off its loans in a timely manner. Think of it as a leveraged buyout with the intent of driving the business into the ground and walking away after having poached the prized assets.

China’s Reach: Seeing is Believing

In a December 2018 submission to the left-leaning Center for Global Development, Scott Morris posited that the Chinese had American inspiration in the form of the following excerpt:

“...to exchange lands which they have to spare & we want, for necessaries, which we have to spare & they want, we shall push our trading houses, and be glad to see the good & influential individuals among them run in debt, because we observe that when these debts get beyond what the individuals can pay, they become willing to lop th[em off] by a cession of lands. at our trading houses too we mean to sell so low as merely to repay us cost and charges so as neither to lessen or enlarge our capital. this is what private traders cannot do, for they must gain; they will consequently retire from the competition...”

The author was President Thomas Jefferson in 1803. He was writing to William Henry Harrison who was then the governor of the Indiana territory. The objective was wrangling lands from Native American tribes via commercial relationships that rendered them vulnerable. Morris noted that the most remarkable aspect of Jefferson’s position is, “that truly commercial actors (the private sector) would be driven out of this task, leaving the government to proceed as it wished.”

Sans judge and jury, it’s unseemly to draw parallels between then and now, to suggest China is driven by a similarly irreverent imperialism. What if this is all about the benign “Belt and Road” initiative to forge new trade routes between China and developing nations that stand to benefit from the economic actualization such endeavors would proffer?

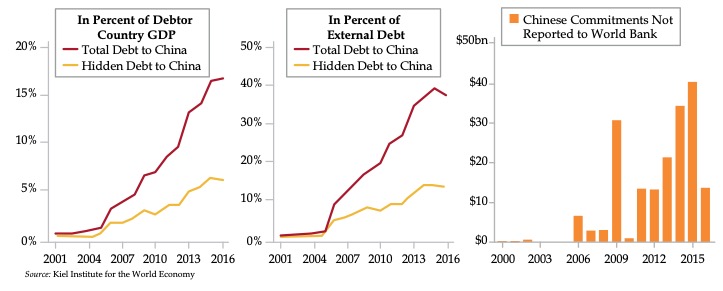

It’s not so much the scope, which speaks for itself. It’s what is not visible to the naked eye. Extricate China from the calculus for a moment. Over the last 10 years, starved for yield as central banks colluded to keep interest rates at artificially low levels, investors clamored for any source of income. One expression of this quest for yield is the roughly $2 trillion that poured into financing emerging markets.

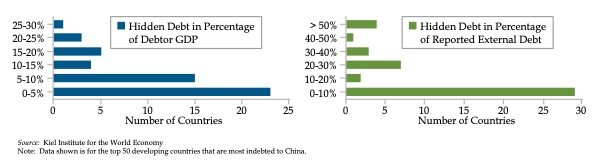

But that’s just what is known to the World Bank (WB) and the International Monetary Fund (IMF). Collaborating with economists Sebastian Horn and Christoph Trebesch, Reinhardt and her team found an additional $200 billion in loans China had extended to overseas borrowers, monies that were unaccounted for in the public purview. The most damning evidence their forensics unearthed: Among the top 50 countries most indebted to China, a dozen of the poorest owed debts equal to 20% or more of their annual GDP. There are even more (green bars) countries who’ve underreported their external debt by 20% or more.

The Hidden Magnitude of Emerging Markets Debt Owed to China

In all, 70 countries are taking part in Belt and Road Initiative (BRI). Many signed on as strategic partners when commodity prices were in the stratosphere and fiscal prospects looked that much more promising as a result.

The examples are plentiful. But the one that garnered the most headlines involves a Sri Lankan port for which that country had borrowed money from the Chinese government. Encountering difficulty in paying the loans, in 2017, the government agreed to lease the port for 99 years to a venture led by China Merchant Port Holdings in return for $1.1 billion. But that’s just one of many deals gone bad. A light railway project and a Pakistani power plant are also among deals that have some countries keen to having made a deal with the devil.

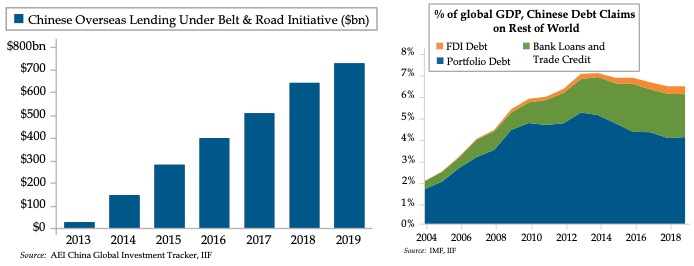

Creditors are like relatives. After the debt is taken on, you can’t get rid of it. Add it all up and China is now the world’s largest creditor to low-income countries. As per fresh data from the Institute of International Finance (IIF), China’s outstanding debt claims on the rest of the world have soared from $875 billion in 2004 to over $5.5 trillion in 2019. That’s more than 6% of global GDP. A huge contributor of which has been debt assumed to further the BRI. As per the IIF, “Since Xi Jinping launched this flagship initiative in 2013, at least $730 billion has been directed to overseas investment and construction contracts in over 112 countries.”

The Belt & Road Initiative Contributes to China’s Rise as Major Global Creditor

The IMF estimates suggest that China accounts for at least 11% of low-income countries’ external public debt. But once again, there is more than meets the eye. A separate study referenced by the IIF, though, suggested that up to 50% of Chinese overseas loans to developing countries are not reflected in the official statistics, an even higher figure than Reinhardt et al found to be the case.

How on earth did these countries let themselves become so hobbled? Some of it goes to extrapolating too much of the present into the future. For a time, the growth of Chinese domestic consumption and Chinese officials lying to the world about their capacity to maintain growth rates papered over the exhaustion of Chinese urbanization. The trade war succeeded in ripping off the façade. China’s growth slowed to a three-decade low arresting global growth’s momentum.

As bad as things were for China, the secular decline in commodities has amplified spreading collateral damage. Headed into 2019, many Wall Street strategists made calls for what they thought was an inevitable reversal in the long downtrend in commodities. The charts screamed that the whole complex was due for a bounce, such was commodities dislocation from other asset classes. In the end, the unexpected came to pass with the renewed decline in commodities reflecting world trade sliding into contraction for the full year 2019.

None of this, however, made for the 100-year storm. Central banks worldwide were feverishly printing money to prevent the debt from coming due, whatever it took to ensure the refinancing window never closed. Nothing short of a massive and global recession could counter central banks’ exertions. And then the impossibility of COVID-19 happened.

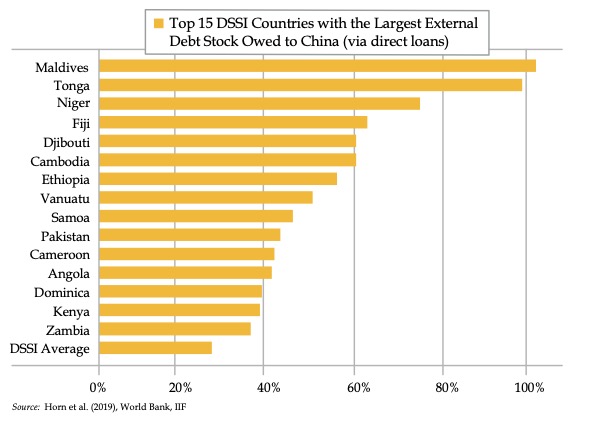

There’s no need to regurgitate headlines. The world of debt did blow up. On April 15, the G20 announced the Debt Service Suspension Initiative (DSSI), an eight-month official bilateral sovereign debt payment suspension by the International Development Association (IDA) countries and least developed countries that are current on their IMF and WB obligations. The DSSI allows 76 IDA countries and Angola to suspend principal or interest payments on their debts to G20 members through the end of 2020.

There is a Chinese wrinkle given many BRI recipient countries qualify for the DSSI. While China is a signatory to the initiative, points of clarification remain. As per the IIF, these include, “the demarcation between official and private sector claims, which is particularly relevant given that much Chinese BRI lending has been done on commercial or near-commercial terms. Many DSSI countries are highly indebted to China, with Pakistan, Angola, and Ethiopia on top of the list in USD terms.”

The Debt Service Suspension Initiative Reprieve Could Collide with Chinese Private Lenders

Estimates indicate that China accounts for over one-quarter of the total external debt of the DSSI countries. This varies from 1% in Comoros (not among the yellow bars) to over 98% in Maldives. Tonga, Niger, Fiji, Djibouti, and Cambodia also top the list of countries most reliant on China for their external financing.

The fact that you’ve (I’d) possibly not heard of the countries listed should not give you a false sense of comfort. There are plenty of recognizable countries in hock to China. The largest among them may have shocked other debtor nations by driving its debt so low it ended 2019 with more cash reserves on hand than sovereign debt. But Russian households are likely in a world of pain as the coronavirus rips through the country. According to Russia’s Ministry of Economic Development, one-third of consumer loans were issued to borrowers whose debt burden consumes 60% of their monthly incomes. This gives new meaning to pay- check-to-paycheck and paints a stark picture of the coming hit to the country’s consumption.

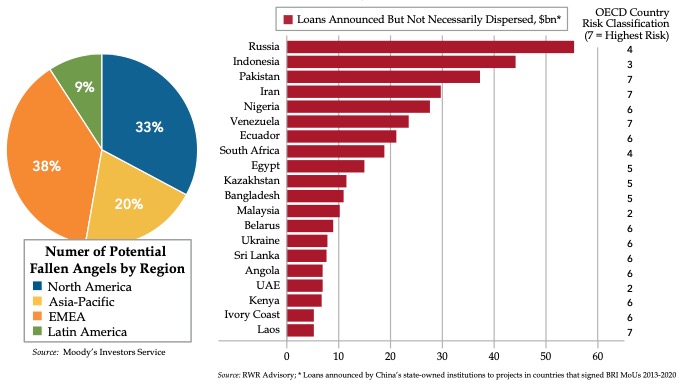

We know the coronavirus has been a tragedy in Pakistan and Iran. We’ll likely never know what it has or has not done to the people of Venezuela. Setting aside the human element, as if that can be done, the globality of the slowdown will act as a drag on every economy in the world. China, the mega-creditor, will not be dealing with debilitated finances in a handful of countries that can’t make good on their obligations. History will also be rewritten by the number of sovereign angels that fall into junk status in the coming downturn.

China’s Belt & Road Loan Recipients Among Some of World’s Weakest Sovereign Credits

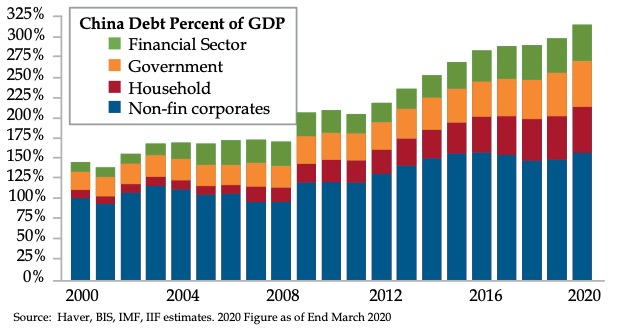

Shakespeare once wrote, “Neither a Borrower Nor a Lender Be.” Rather than reminicsce about English literature classes gone by, trust me that both sides of the proposition ended badly. While it takes one’s breath away that world debt was tracking $325 trillion in the first quarter, China’s contribution to the effort is borderline reckless. Total debt in the world’s second largest nation hit 317% of GDP, up from 300% in 2019’s fourth quarter marking the largest three- month growth in history. The context is painful – that same ratio 172% of GDP in 2008.

The next time someone raises the subject of the miracle of global growth in the past decade, remind them that since 2007, China has accounted for more than 40% of the global growth in debt. For our immediate purposes, the takeaway is that China might have to be wicked bill collector. Its own finances may be so hobbled, it’s forced to collect on its debts.

China Clocks Record Debt Growth Rate in First Quarter

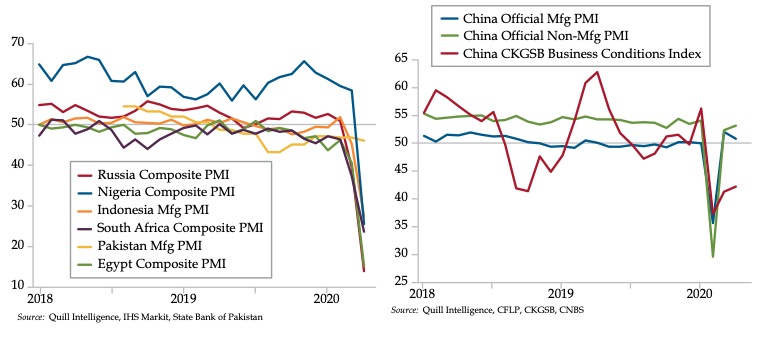

This gets us back to Shakespeare. In the midst of the closest thing to a global depression to happen upon the world in more than a century, the need to collect on debts and the wherewithal of borrowers to satisfy those demands don’t always meet. A quick perusal of some of China’s biggest debtors’ manufacturing sector makes that point abundantly clear. After weathering the trade war, flirting with expansion and just as often succumbing to contraction, every major BRI loan recipient’s factory sector has fallen deep into contraction.

At the risk of offending your sense and sensibility, it’s highly unlikely all of these countries hold the same tight grip on their statistical agencies as China. With that in mind, it’s equally unlikely they will enjoy the same V-shaped recovery that China has managed to (ahem) engineer. QI’s steely-eyed Dr. Gates suggested that cutting through the flattery could be easily accomplished by incorporating China’s CKGSB Business Conditions Index. Unlike the official surveys measuring manufacturing and non-manufacturing activity, this gauge of private sector small and medium business sentiment has slid to record lows and scarcely staged a rebound.

Will China’s Debtors Also Boast V-Shaped Recoveries?

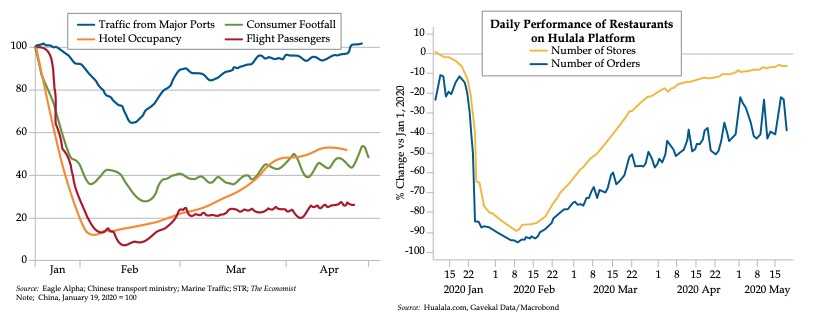

As for the other type of scarcity, as hard as we’ve battled to source real-time data to guide us through a post-coronavirus U.S. economy, we’ve found it’s nearly impossible to get our hands on reliable real-time Chinese data. One index suggesting that small and medium sized businesses are still hurting leads one to conclude that the consumer is as well.

Luckily, QI’s friends at Gavekal were kind enough to provide us with data showing that restaurant traffic remains moribund. That’s corroborating evidence if we’ve ever seen it and gives us a feel for what’s to come stateside. It’s also tricky to fabricate consumer footfall, hotel occupancy, and flight passenger traffic. Unlike port traffic, which can be encouraged, these three which have yet to regain their former levels, are hard to fudge.

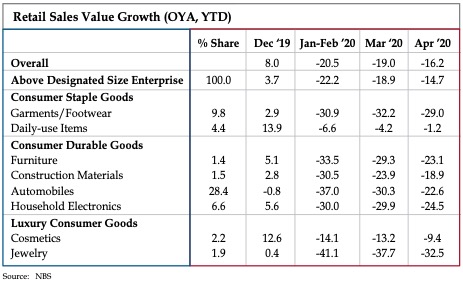

Finally, we have the weeds of April’s retail sales data to dig through. As was the case with U.S. data, apparel got shellacked. But as you see, this extremely discretionary sector has yet to bounce back. It doesn’t help that there was no Cash for Clothes to match the government’s car-buying incentive campaign. Jewelry and household electronics are the other two highly discreet categories that have also seen continued weakness. The tepid rebound in the discretionary sector validates the weakness in sentiment among the smaller operators and refutes the official narrative.

The Chinese Consumer Has Not Rebounded Alongside the Factory Sector

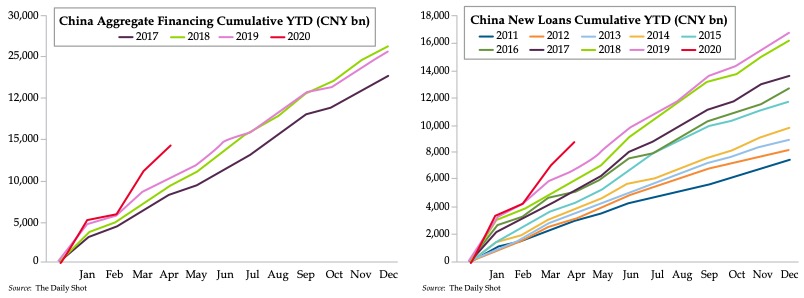

With estimates suggesting the true unemployment rate, that will never see the light of day, is closer to 10%, it’s no wonder Chinese loan originations and aggregate financing are running off the charts. As is the case with the Federal Reserve and Congress, both monetary and fiscal authorities in China are working overtime to keep the peace. The social safety net is nowhere near as tightly knit in China which explains leaked footage here and there of protests in the streets.

On a higher level, it’s fair to ask whether China can continue to play its two roles of lender and borrower. It’s one thing to weather a global meltdown when you’re still in relatively good standing with your frenemies. It’s quite another when you whittle down your allies to a tight circle in the midst of a global pandemic for which you’re increasingly blamed.

China Pulls Out All Stops to Keep Stimulus Flowing to the Economy

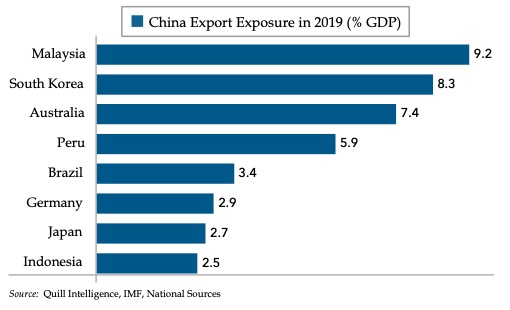

At last count, 116 countries had joined Australia in demanding an independent coronavirus inquiry. In a world rife with divisiveness both within countries and across borders, this unified front is extraordinary. At its most fundamental, Australia has suffered lower losses tied to the coronavirus and has much to lose by leading the affront to China, which is not named by the World Health Organization (WHO). Standing on principle on behalf of the rest of the world is sacrificial when your economy has been expanding for nearly 40 years thanks in large part to China. The most direct representation is the 7.4% of Australia’s GDP it exports to China. But China’s economic influence goes well beyond that one input. The same can be said for the other countries in this next chart, all of which have joined Australia in its demands.

United Against the Hand that Feeds Them

Though the saber-rattling emanating from U.S. shores due East is the loudest, the one country conspicuous in its absence from the roll call of countries petitioning the WHO is the United States. That is not to say the demands are any less insistent.

In late April, Republican Senators Ted Cruz of Texas and David Perdue of Georgia and with 14 other senators sent a letter voicing their concerns about the potential risk of deteriorating market conditions as it pertained to those beholden to China. Their plea:

“We urge the State Department and the Treasury to consider the impact of the Chinese-financed Belt and Road Initiative (BRI) on the finance of many troubled economies and policy implications of additional International Monetary Fund (IMF) or World Bank support.

“Domestic economic constraints in China stemming from COVID-19 will likely make China less willing to roll over debts as they mature, which could exacerbate emerging-market liquidity challenges, as projects struggle in areas of strategic interest, China will be tempted to safeguard its investments and political influence.

"Short of this, U.S. and other Western taxpayers would be in essence bailing out Chinese financial institutions and enabling China's debt-trap diplomacy."

Few would argue the animus has been a long time in the making. QI friend Leland Miller, with whom you are likely familiar care of his exemplary China Beige Book, cut to the chase: “The truth is, this has been some time in the making. This type of debt diplomacy spiraled out of Beijing's control years ago. Covid19 just accelerated the reckoning and made it more of a public spectacle.”

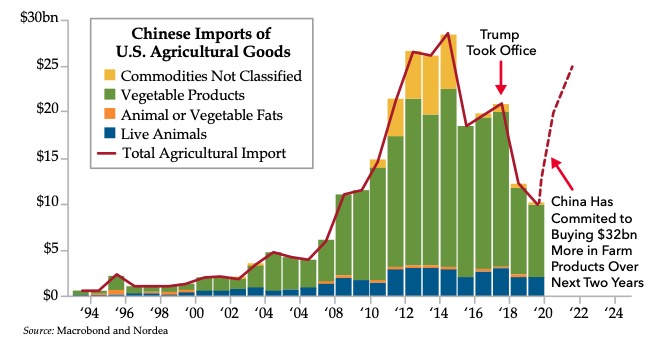

Dare we point out the other elephant in the room, that of it being an election year. Through March 2020, China’s year-to-date imports from the U.S. were $19.8 billion, That compares to the targeted level of $43.2 billion. To borrow a phrase from another friend, Ben Hunt, which describes the flagrancies that have manifested in too many ways to count – They’re not even pretending any more.

Chins Flaunts its Disregard of the Trade Agreement

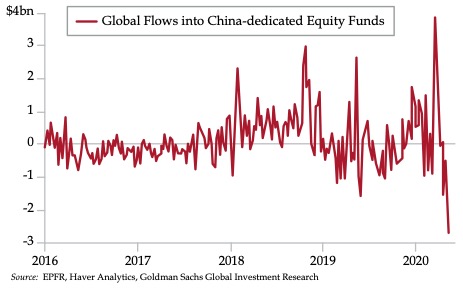

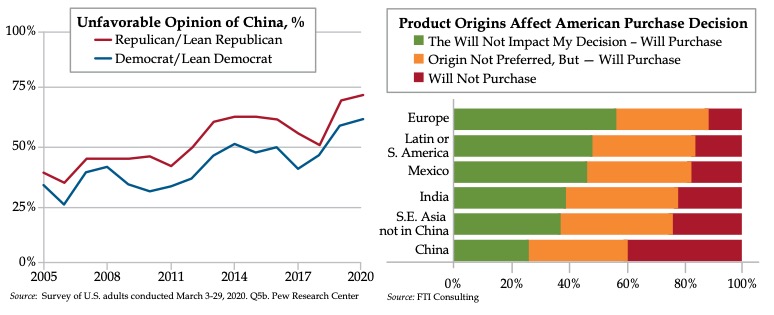

In true form, Trump is meeting this aggression by going on the attack. But set aside the histrionics on display in the White House. Focus instead on the massive fund flows out of China-dedicated funds. Behold the bipartisan disdain with which the American public holds China. Cost consciousness be damned, take note that 40% of U.S. consumers will no longer buy a product brandishing the label “Made in China.” The backlash against China has spread from coast to coast and made its way round the world.

Investors and Consumers Turn Their Backs on China

China’s biggest annual political affair takes place this Friday. The National People’s Congress was delayed from its scheduled March start as the coronavirus necessitated the precaution for safety sake. The world will be watching. When we peer into that grand gathering, will they be standing shoulder to shoulder as is customary? Or will social distancing besmirch appearances as world leaders seem determined to communicate by example? As the world unites to uncover the origins of the invisible virus and its unforgiving aftermath, we can only expect that China comes together with equal energy in defiance of its detractors. With so much lost, bravado may fall far short. The time may have finally come for China’s Imperialism to be Interrupted.

Quill Intelligence