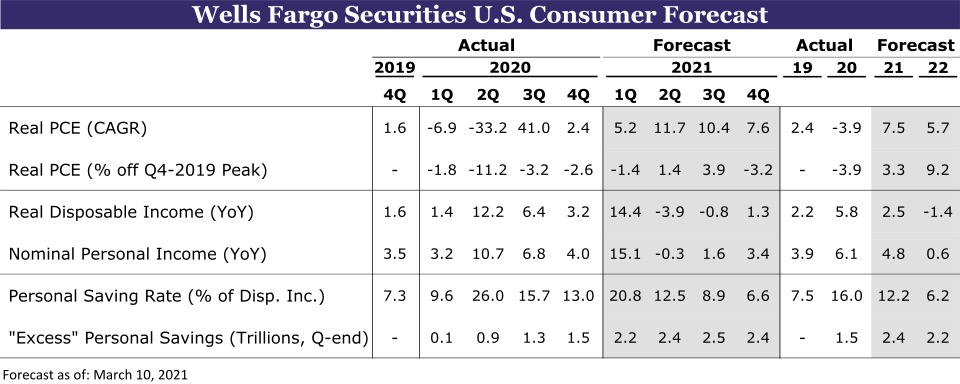

Summary

Ready Money & the Re-opening of the Service Sector

In data going back to the 1940s, U.S. consumer spending has never grown at an annualized percentage rate north of 10% in back-to-back quarters, but our latest forecast update says that is exactly what could be in store for the second and third quarters of this year. This call for the fastest six-month pace of consumption in at least 70 years warrants some explaining and that is what this report is about.

Households are set to receive another $700 billion over the next six months from the latest round of COVID fiscal relief, which will add to already elevated levels of “excess” personal savings. A combination of a mountain of savings and over a year of forced-thrift among consumers leaves us fairly optimistic for a sizable snapback in spending this year.

Unlike earlier rounds of relief when the virus was growing, the public health situation is rapidly improving now, which suggests the latest fiscal relief may provide an even larger boost to spending than prior packages. If vaccination continues at its current pace, we expect the turning point for services consumption to be around midyear.

Our latest forecast has the overall level of real personal consumption expenditures surpassing its pre-virus peak (Q4-2019) by the second quarter of this year, with the pace of growth remaining above trend throughout our forecast horizon to 2022.

Although the near-term outlook is more certain than it has been in a while, things remain unsettled further out. Spending in the latter half of this year and into next year depends heavily on what the public health situation looks like next winter and to what extent consumers draw down “excess” savings as the jolt from direct checks fades and unemployment benefits run dry. In other words, is the consumer sugar-high set to wear off?

Source: U.S. Department of Commerce and Wells Fargo Securities

What the Latest Fiscal Relief Package Means for Households

Households are set to receive around another $700 billion over the next six months from the latest round of COVID-fiscal relief, which will lead to another boom in consumer spending and add to already elevated levels of household savings. That amounts to about 40% of the roughly $1.9 trillion package showing up in personal income. Although we have been factoring additional stimulus into our forecast for quite some time, here we unpack the high-level details of the cash support to households.

As with the past two packages, a sizable portion of the support will be in the form of another round of “economic impact payments,” or direct checks to households from the federal government. Importantly, these checks will be larger with most Americans seeing more than double the amount they received from the late-December fiscal stimulus package. This segment of the bill should total roughly $400 billion. Our personal income forecast assumes the timing of these checks going out is similar to what occurred last spring and this winter, with most households receiving the payments in March and April.

The package also includes an extension of the pandemic unemployment programs and includes an additional $300/week in jobless benefits through September, which together we estimate to total about $170 billion. Finally, enhanced tax credits were also included in the package, which are set to boost income in the latter half of this year.

This Is a Bigger Deal for Personal Income than Last Year's CARES Package

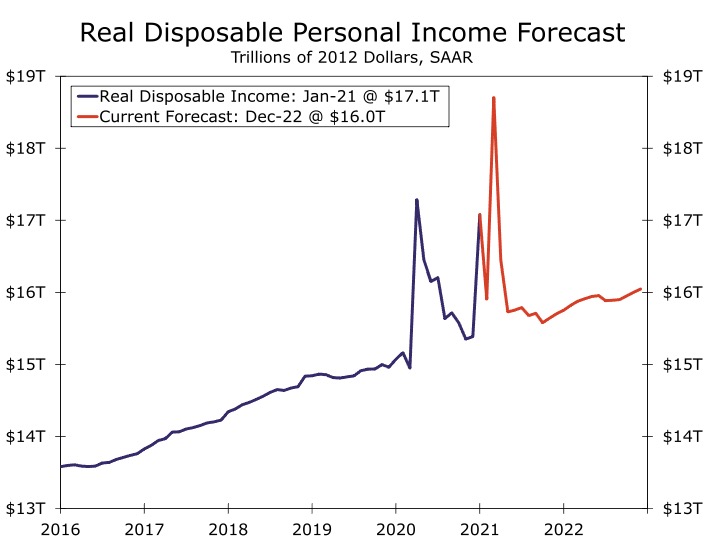

All told, we expect a combination of sizable direct checks, more generous unemployment benefits and enhanced tax credits to push real disposable personal income to unprecedented levels in March and April (Figure 1).

This package underpins our bullish outlook for a rebound in consumer spending midyear. Based on the January spending data and the higher propensity to consume with the latest round of relief, we feel fairly confident that the next round of direct checks will boost spending. Research suggests one-time payments, such as the direct checks to households, lead to a boost in spending more than a steady payment resulting in a change to income1. With many households set to receive direct checks that are more than double what they received in January, we expect a sizable jolt to spending to follow in the April and May data.

Figure 1

Source: U.S. Department of Commerce and Wells Fargo Securities

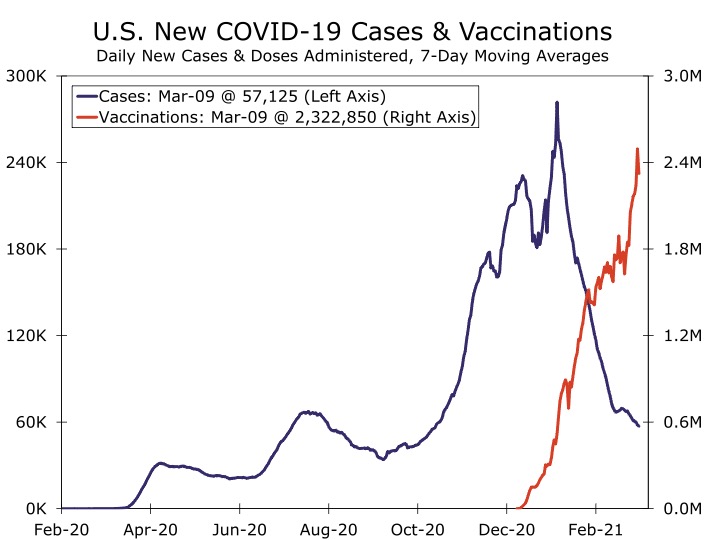

Figure 2

Source: Bloomberg LP and Wells Fargo Securities

Furthermore, unlike the past COVID-fiscal relief packages, which were passed during the initial shock- and-awe phase of the pandemic (March 2020 CARES Act) and when the virus was approaching its worst point (December 2020 package), this package is set to hit as the public health situation is rapidly improving (Figure 2). New daily case counts are falling faster than at any time in the past year and the vaccine deployment is steadily gaining momentum, which suggests the latest stimulus may provide an even larger boost to spending than the past packages. Warmer weather across most of the country beginning in April should also provide added support to spending just as consumers should once again have the ability to spend, particularly on services.

A Year's Worth of Forced Thrift Adds Up to a Mountain of Savings

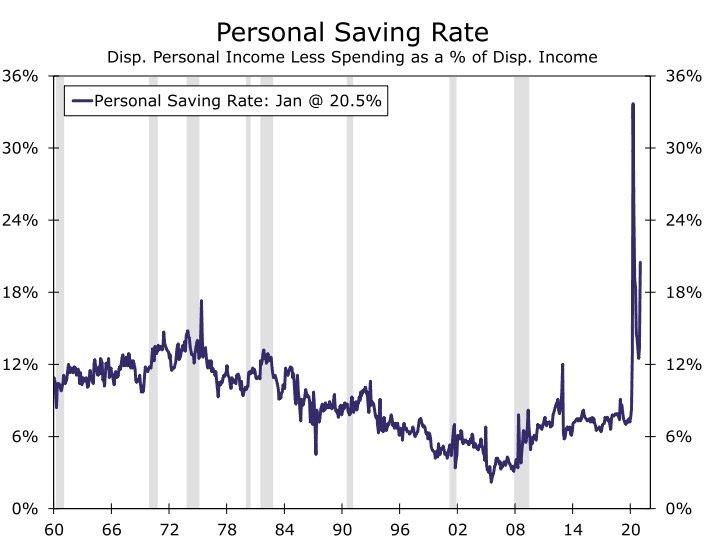

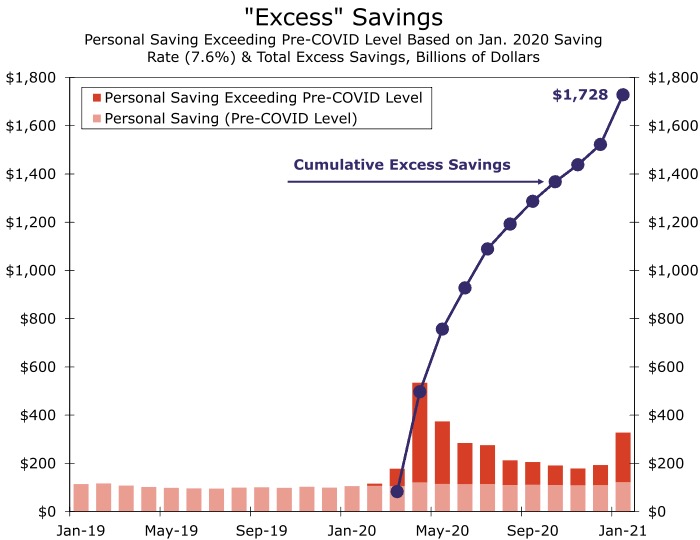

The influx of cash in March/April is also set to add to already elevated levels of “excess” personal savings. Personal saving rates jumped at the onset of the pandemic as an influx of fiscal transfers were met with forced thrift among consumers unable to spend. The personal saving rate skyrocketed to an all-time high in April, the same month the U.S. economy shed over 20 million jobs, but personal income surged 12.4% due almost entirely to fiscal transfers from the government. The personal saving rate received another boost in January, as households received another round of direct checks (Figure 3).

Comparing the recent elevation in personal saving rates to saving prior to the pandemic, we estimate consumers have accumulated roughly $1.7 trillion in “excess” savings through January2 (Figure 4). Excess savings should continue to rise, surpassing $2 trillion once the March fiscal package hits income and topping out at around $2.5 trillion in the third quarter based on our forecasts for personal income and spending. For context, that forecast implies excess saving is set to reach nearly 20% of consumer spending in a given year pre-pandemic. This implies a dramatically large amount of “dry powder” for consumers to tap once the economy re-opens later this year and in-person activities resume.

Figure 3

Source: U.S. Department of Commerce and Wells Fargo Securities

Figure 4

Source: U.S. Department of Commerce and Wells Fargo Securities

Where's the Money Lebowski?

Until the next Fed Survey of Consumer Finance in 2022, there is no way to know for sure if all the excess savings has just been sitting idle. In fact, the historic pace of deposit growth and a decline in revolving consumer credit suggest a decent portion of the saving may have been used to pay down debt. Survey evidence by the New York Fed after the CARES Act suggested households used about 35% of their stimulus checks to pay down debt3. Even if a sizable amount of excess savings has lowered debt burdens, we still view that as a positive for the medium- to long-term trajectory of the consumer.

Another reasonable argument that we gather anecdotally is that excess savings may be adding to the recent rise in retail investing. With households unable to spend in a traditional sense, they have instead allotted some recent cash to investing in brokerage accounts or perhaps decided to contribute more to retirement savings. Again, if this is the case, we view these decisions as positives for the overall financial health of the consumer, provided the equity market holds up. In many ways, on a macro level, the consumer is coming out of the crisis in better financial shape than they came into it. The healthier financial position combined with months of doing dishes and staycations leads us to believe pent-up demand will be unleashed once consumers have the ability to safely return to some semblance of normal life.

How Does This Translate to Our Forecast for Consumer Spending?

Between another sizable injection into the economy in the form of fiscal transfers to households and record amounts of excess savings, consumers have signicant means to consume as the COVID situation improves. In many ways, the medium-term outlook comes down to how comfortable consumers are with venturing out. Consumer mindsets appear to be largely influenced by the virus itself, with confidence data as measured by the Conference Board only hitting triple digits during two months of the pandemic era: September and October. That coincides with the periods when new cases fell below 60,000, and we were making progress against the spread, but before the winter surge. Now with vaccinations under way and case counts falling once again, confidence is rebounding.

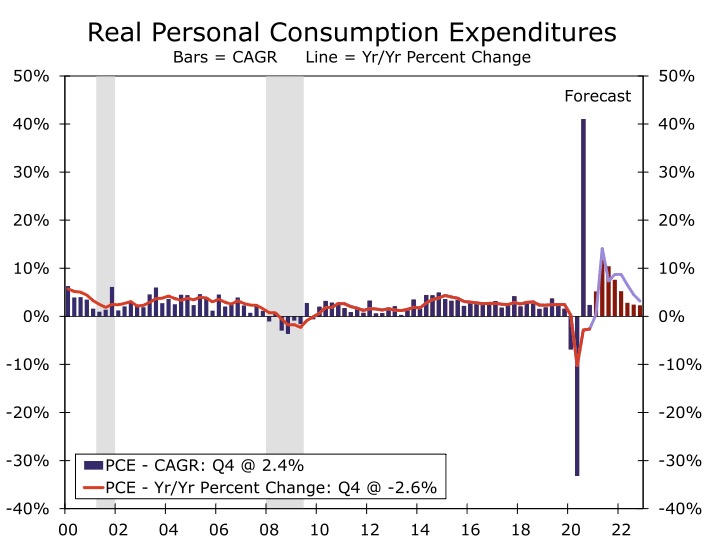

This leaves us optimistic for a rapid rebound in consumer spending this year. Our latest forecast projects total personal consumption expenditures (PCE) on track to grow 7.5% this year as a whole, and we forecast back-to-back double-digit percentage gains in PCE in the second and third quarters (Figure 5). If realized, the U.S. consumer is poised to emerge from the recession with the biggest six- month spending surge the world's largest economy has seen in at least 70 years.

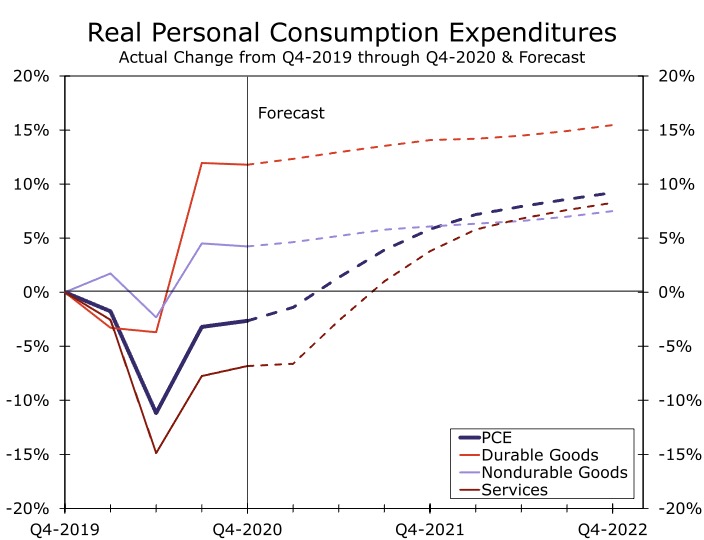

We have long expected a service-sector rebound as the virus gradually fades away, but the remarkable pace at which the public health situation is improving leaves us more optimistic regarding the timing of the spending rebound. If the United States is able to sustain its current vaccination pace, the turning point in services consumption should be around midyear (Figure 6). The sizable pickup in services consumption will be the primary driver of PCE in the second half of the year, but that need not come at the expense of an outright collapse in goods spending. We've long held the view that goods' consumption would hit an air pocket once service spending returned, and we got that toward the end of last year with three consecutive monthly declines in goods spending. But then, goods rebounded nearly 6% in January, amid an influx of cash in the form of direct checks from the government. It remains to be seen if the air pocket late last year was the extent of it or if we will get a renewed pullback once services again take up wallet share. We look for goods spending to remain elevated, though the pace may moderate over the next year or so.

Figure 5

Source: U.S. Department of Commerce and Wells Fargo Securities

Figure 6

Source: U.S. Department of Commerce and Wells Fargo Securities

Gone with the Windfall?

After a spending boom this year, things get a lot more uncertain. Spending in the latter half of this year and into next year depends heavily on what the public health situation looks like next winter and to what extent consumers draw down excess savings as the jolt from direct checks fades and as unemployment benets runs out at the end of September. The latest round of fiscal relief already faced some skepticism, which makes another round of stimulus checks untenable. In other words, the torrid pace of spending cannot be maintained.

Clearly, the sizable six-month pace of consumption we project in the second and third quarters cannot be sustained, but it remains to be seen to what extent spending stabilizes after pent-up demand takes hold and the novelty of getting out of the house wears off a bit. We expect consumers to continue to draw on excess savings, leading to above trend growth through next year, but there is something to be said for the mental accounting of relying on a dwindling pile of savings. To the extent that households see this as assets being diminished rather than a stable inflow of cash in the form of disposable income, we might see reluctance to spend it all. The scar tissue from COVID may convince some households of the merits of maintaining a more robust rainy day fund than they did before the pandemic.

Endnotes

1Sahm, C., Shapiro, M. and Slemrod, J. “Check in the Mail or More in the Paycheck: Does the effectiveness of Fiscal Stimulus Depend on How It Is Delivered?” National Bureau of Economic Research. July 2010. (Return to Section)

2We calculate “excess” personal saving by aggregating the addition to personal saving since March that is in excess of the amount of saving based off of the pre-crisis January 2020 personal saving rate of 7.6%. (Return to Section)

3Armantier, O., Goldman, L. Et. All. “How Have Households Used Their Stimulus Payments and How Would They Spend Next?” Liberty Street Economics. October 2020. (Return to Section)

Required Disclosures

This report is produced by the Economics Group of Wells Fargo Securities, LLC, a U.S. broker-dealer registered with the U.S. Securities and Exchange Commission, the Financial Industry Regulatory Authority, and the Securities Investor Protection Corp. Wells Fargo Securities, LLC, distributes this report directly and through affliates including, but not limited to, Wells Fargo & Company, Wells Fargo Bank N.A., Wells Fargo Clearing Services, LLC, Wells Fargo Securities International Limited, Wells Fargo Securities Europe S.A., Wells Fargo Securities Canada, Ltd., Wells Fargo Securities Asia Limited and Wells Fargo Securities (Japan) Co. Limited. Wells Fargo Securities, LLC is registered with the Commodity Futures Trading Commission as a futures commission merchant and is a member in good standing of the National Futures Association. Wells Fargo Bank, N.A. is registered with the Commodity Futures Trading Commission as a swap dealer and is a member in good standing of the National Futures Association. Wells Fargo Securities, LLC and Wells Fargo Bank, N.A. are generally engaged in the trading of futures and derivative products, any of which may be discussed within this report.

The information in this report has been obtained or derived from sources believed by Wells Fargo Securities, LLC to be reliable, but Wells Fargo Securities, LLC does not guarantee its accuracy or completeness, nor does Wells Fargo Securities, LLC assume any liability for any loss that may result from the reliance by any person upon any such information or upon any opinions set forth herein. Such information and opinions are subject to change without notice, are for general information only and are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial product or as personalized investment advice. Wells Fargo Securities, LLC is a separate legal entity and distinct from affliated banks and is a wholly owned subsidiary of Wells Fargo & Company. © 2021 Wells Fargo Securities, LLC

Important Information for Non-U.S. Recipients

For recipients in the United Kingdom, this report is distributed by Wells Fargo Securities International Limited ("WFSIL"). WFSIL is a U.K. incorporated investment firm authorized and regulated by the Financial Conduct Authority. For the purposes of Section 21 of the UK Financial Services and Markets Act 2000 (“the Act”), the content of this report has been approved by WFSIL, an authorized person under the Act. WFSIL does not deal with retail clients as defined in the Directive 2014/65/EU (“MiFID2”). The FCA rules made under the Financial Services and Markets Act 2000 for the protection of retail clients will therefore not apply, nor will the Financial Services Compensation Scheme be available. For recipients in the EEA, this report is distributed by WFSIL or Wells Fargo Securities Europe S.A. (“WFSE”). WFSE is a French incorporated investment firm authorized and regulated by the Autorité de contrôle prudentiel et de résolution and the Autorité des marchés financiers. WFSE does not deal with retail clients as defined in the Directive 2014/65/EU (“MiFID2”). This report is not intended for, and should not be relied upon by, retail clients.

SECURITIES: NOT FDIC-INSURED - MAY LOSE VALUE - NO BANK GUARANTEE