Oil and gas prices have roared back from the lows seen in 2020. However, investment in upstream production has not seen a similar bounce back. The energy transition push means that there is plenty of reluctance to boost spending. Clearly, this will have an impact on longer-term supply dynamics for the oil and gas market

Warren Patterson, Head of Commodities Strategy

ING, 26 January 2022

In this article

- Stubbornly low investment in upstream oil & gas

- What is holding back upstream investment?

- What are the longer-term implications of a lack of investment?

Stubbornly low investment in upstream oil & gas

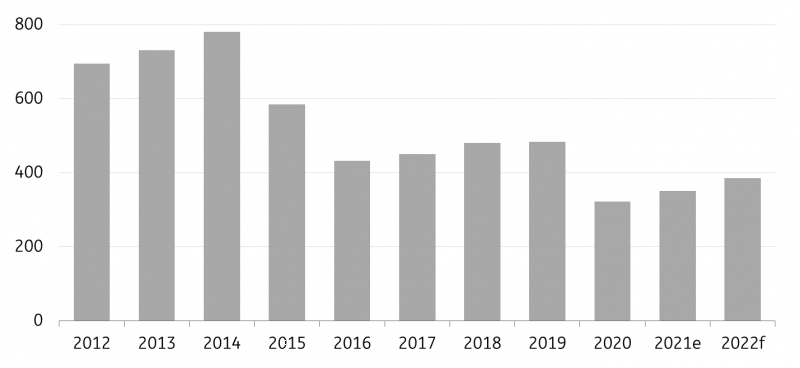

The upstream industry has struggled to boost spending over the years. According to IEA data, annual investment in upstream oil and gas peaked at around $780b in 2014. Since then, the highest annual spending we have seen was in 2019, which amounted to around $483b, just 62% of 2014 levels. This fall in spending has corresponded with the growth we have seen in US shale.

Covid-19 and the corresponding weakness in oil prices only led to a further decline in spending - estimated at around $320b in 2020. The recovery that we have seen in oil prices since bottoming out in 2Q20 has seen a slight pick-up in spending. However, at just $351b in 2021 it is still a far cry from 2014 levels, and indeed from pre-Covid levels. With the strength in prices in 2021, however, we expect to see another uptick in spending in 2022. Rystad Energy’s base case is that spending will increase by 10% year-on-year. This would still leave 2022 annual investments below 2019 levels.

Upstream spending still expected to be well below pre-Covid levels in 2022

Global oil and gas upstream investment (USD b)

Source: IEA, Rystad, ING Research

In recent years, the share of spending in short-cycle projects (wells that can be drilled and brought online quickly) has increased significantly, as these developments are a lower risk than some offshore projects, which take several years to develop and become operational. This would have been driven largely by growth in the US shale industry. However, post-Covid, we have not seen a strong recovery in drilling activity from US producers. The lack of spending from US independent producers, as well as oil majors, has meant that growth in upstream investment is currently being driven by Russian companies and Chinese and Middle Eastern national oil companies, according to the IEA.

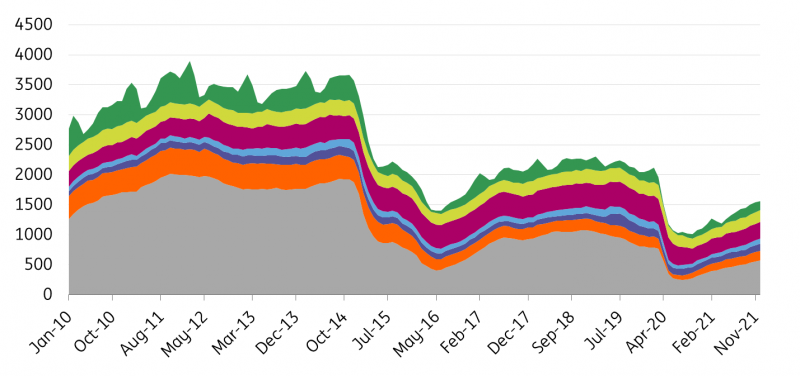

Global rig data shines a light on the impact lower spending is having on drilling activity. According to Baker Hughes data, at the end of December 2021, the global rig count totalled 1,563. This is a significant increase from the low of 1,016 seen in October 2020. However, the global rig count is still about 23% below December 2019 levels. Looking at the count by region, only Canada's rig count is above 2019 levels.

Global drilling activity recovering, but still plenty of room to grow

Global active rig count

Source: Baker Hughes

What is holding back upstream investment?

There are several factors holding back upstream spending. More recently, the demand hit from Covid-19 and the resulting low oil and gas prices saw a drastic cut in spending. While capex will recover from the lows (and already is), the longer-term trend is downwards.

In the US, there has been a shift in the behaviour of producers. The days of rampant production growth appear to be behind us. Instead, the industry is focusing on capital discipline, which has led to record levels of free cash flow generated amongst US producers. Shareholders have put significant pressure on producers to focus more on shareholder returns and it appears that this is what we are seeing now. While US oil output will continue to grow from current levels, capital discipline means that growth will be more gradual, unlike in previous up cycles.

Oil majors have also slashed upstream spending significantly. While part of this would reflect the low-price environment seen over 2020, there is again a structural change. ESG is becoming an increasingly important factor for the oil & gas industry, both to meet internal climate policies and from external pressure. Therefore, we are seeing majors reducing their share of upstream spending, while increasing the amount going to renewables. In fact, the IEA estimates that in 2021, investment in renewables exceeded spending in upstream oil and gas. While there will be pressure on majors to address carbon emissions, there is also uncertainty over the pace of the energy transition, which only adds to the reluctance to make significant upstream investments.

According to the IEA, oil majors make up around 25% of total upstream spending at the moment, compared to closer to 40% in the mid-2010s. This highlights the changes in attitude and behaviour we are seeing coming through from majors. But it’s not just majors which are taking ESG more seriously. US independents are also putting more focus on it. Historically, CEO pay packages of independents were largely tied to production and production growth. ESG, capital spending and cash flow generation are becoming increasingly important factors for determining these pay packages.

What are the longer-term implications of a lack of investment?

The oil market should be able to meet demand in the medium term (next two years). However, the significant fall in spending and the lack of willingness of some producers to invest does leave the market in a vulnerable state in the longer term. It is important to remember that given natural declines rates, producers need to invest in order just to keep production flat. Decline rates are in the region of 6% per year. Obviously, the market will need to ensure that production doesn’t remain just flat, but grow in the years ahead, given the need to meet demand growth.

There is plenty of uncertainty over how much investment is needed, given the big question mark around when global oil demand will peak. The key agencies have different views on when this will happen. OPEC is of the view that oil demand will plateau around 2035, while the IEA has different scenarios which see demand peaking soon after 2025 or as late as the mid-2030s. Clearly, if the demand peak in oil is still more than a decade away, it suggests that we need to see a pickup in investment. As a result, this suggests that there is upside for oil prices in the longer term. These higher prices will be needed to either attract further spending or to bring forward peak demand.

The gas market should attract a larger share of future upstream investment. In fact, Rystad sees upstream gas and LNG investments growing by 14% YoY in 2022, compared to 7% growth in upstream oil. However, spending is still expected to be below 2019 levels. Natural gas is seen as a bridging fuel for the energy transition, and this should support robust demand growth in gas/LNG over the next decade. Asia should drive this demand growth with LNG, as we see coal to gas switching. We estimate that LNG export capacity will grow by around 3% per annum through until 2025, which will likely fall short of what is needed, particularly if demand follows the same trend we have seen in recent years, with trade in LNG growing by around 8% per year since 2015.

All these factors suggest that prices will remain above historical averages.

Link to the original article

Content Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.