At its July meeting, the Bank of Japan (BOJ) made a small tweak to its yield curve control (YCC) policy. However, does this minor adjustment convey major implications? In our last update in March, we were closely watching services growth, inflation, and the appointment of Governor Ueda. Following the BOJ’s July change in YCC, we consider the potential impact on the trajectory of Japanese inflation and the implications for Japanese government bonds (JGBs) and the yen (JPY).

A regime change in Japanese inflation?

Japan had been in deflation for 30 years, but we have seen stirrings of a regime change since last year. Based on recent inflation trends, one could conclude that the BOJ’s ultra monetary easing over the last 30 years has finally worked. Between 1999 and 2019, Japanese core inflation averaged -0.24%, using data from Macrobond and the Japanese Statistics Bureau. Based on the latest BOJ forecasts, core inflation is expected to average 2.2% between 2022 and mid-2025.

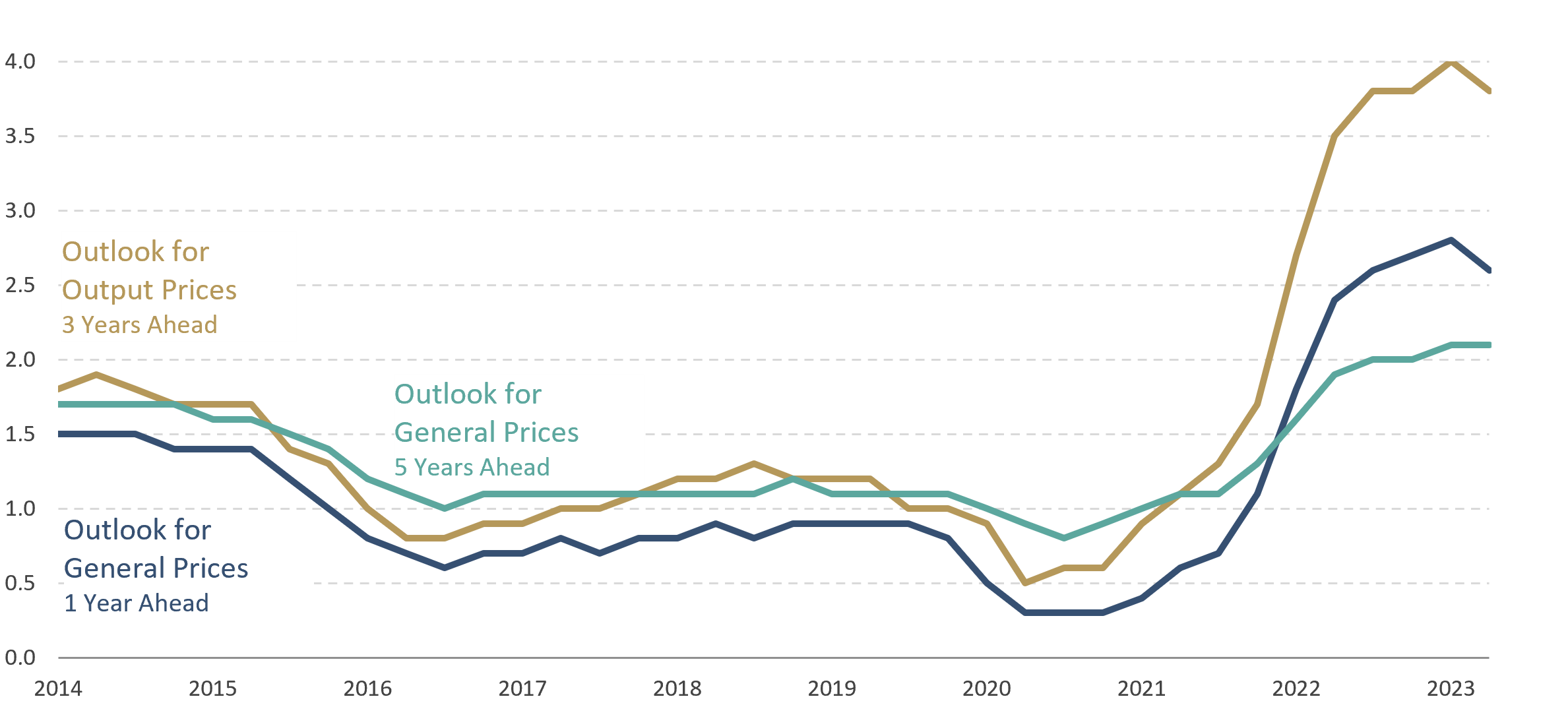

Recent inflation trends up until July of this year showed no relent, propelled by a strong, broadening underlying trend. The quarterly Tankan survey indicates corporations’ outlook on prices across the 1-, 3- and 5-year segments remains above 2% (see Exhibit 1).

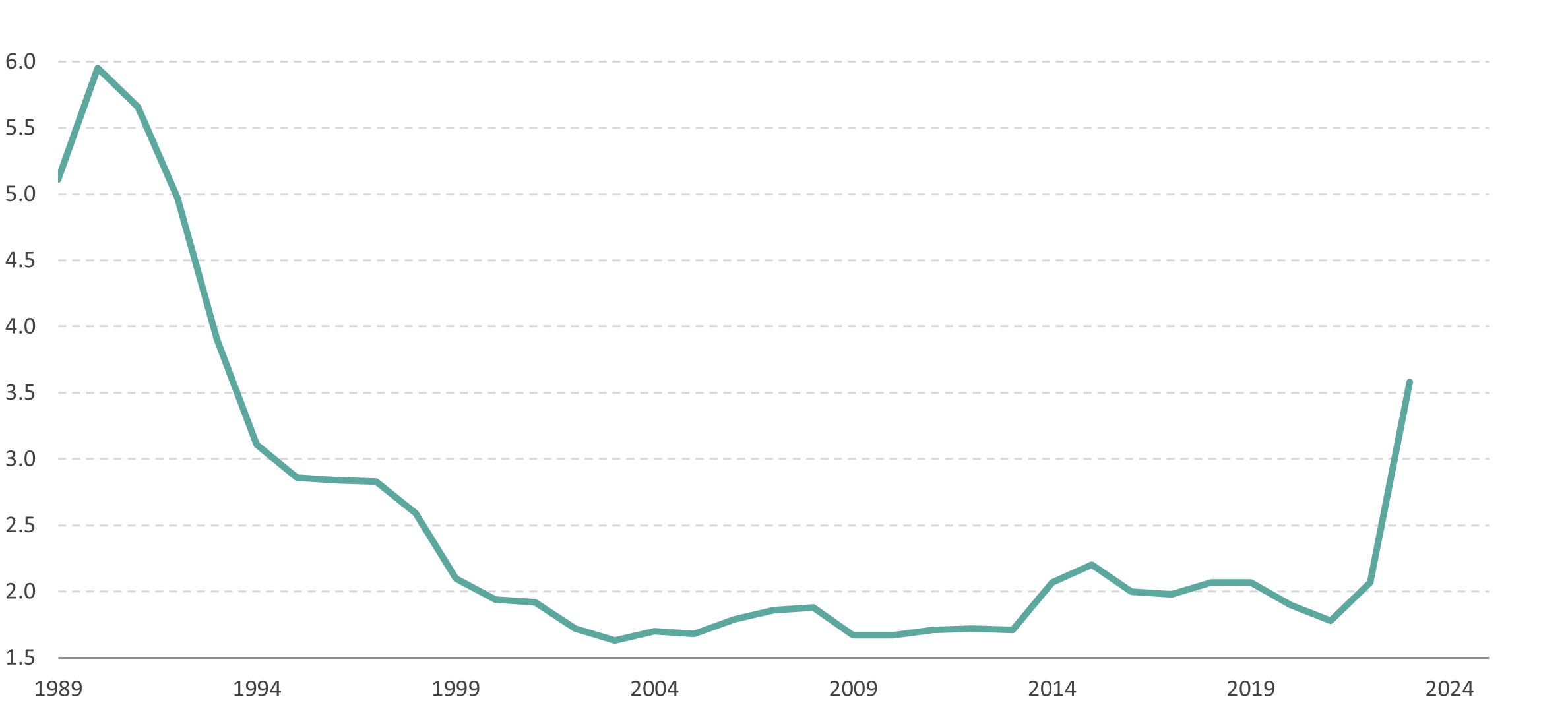

The 2023 Shunto wage negotiations recently concluded with a headline wage growth of 3.58%, the highest since the early 1990s (see Exhibit 2). This trend could well continue given corporate profits are set to reach all-time highs.1 Coupling prospects for higher wages along with business expectations for rising inflation, corporations may be more inclined to pass on higher prices to consumers compared with the past.

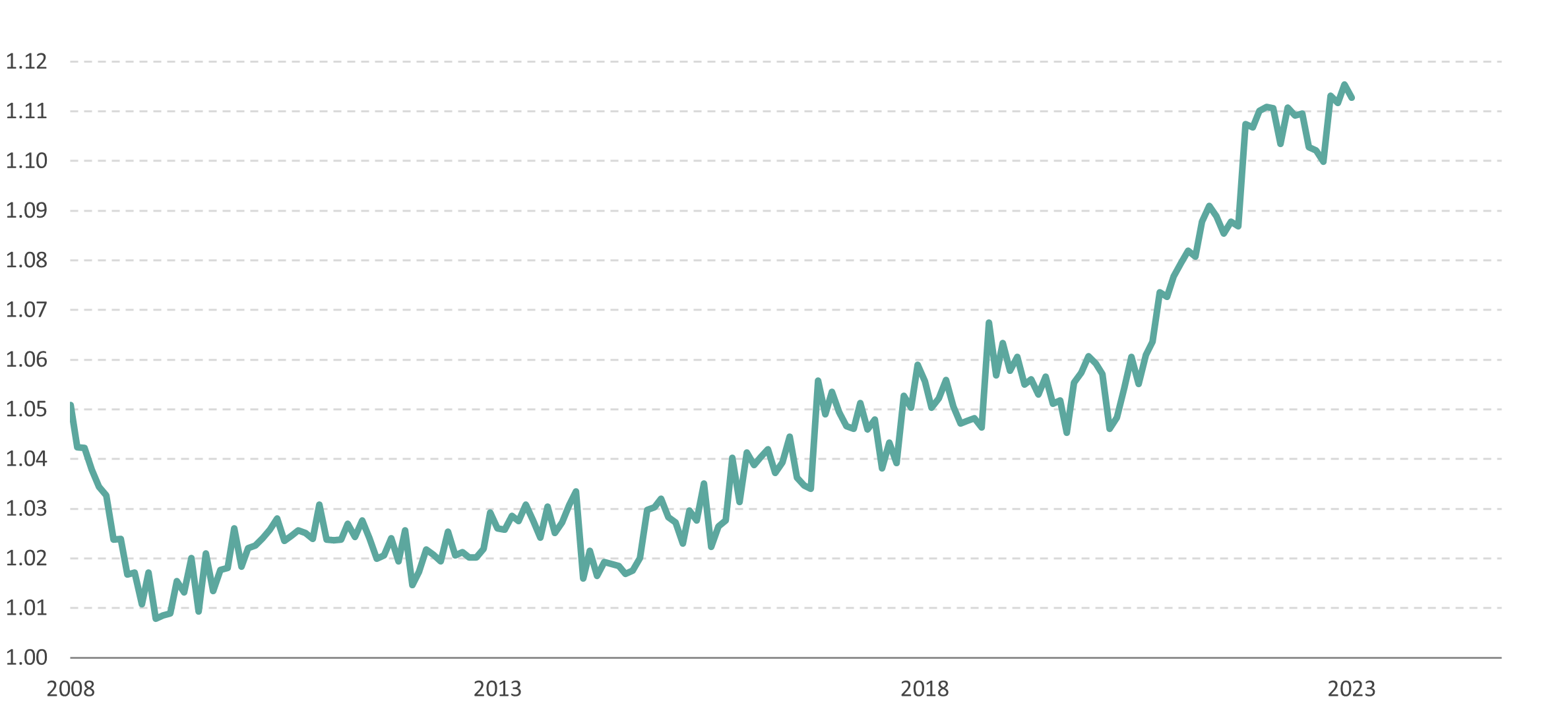

Lastly, asset prices are a testament that Japan might finally be ready to move out of its easy monetary regime. Residential real estate prices in real terms have been growing above trend since 2021 (see Exhibit 3). Japanese equities have been one of the top-performing equity markets this year, based on the performance of the Nikkei 225 Index.2

Exhibit 1: Tankan Corporate Outlook on Prices

Percent, Change year/year, as of Q2 2023

Sources: Brandywine Global, Macrobond, BOJ (© 2023). There is no assurance any forecast, projection or estimate will be realized.

Exhibit 2: Shunto Spring Wage Negotiations – Weighted Average Wage Growth

Percent, as of 2023

Sources: Brandywine Global, Macrobond (© 2023).

Exhibit 3: Japan: Residential Real Estate Prices in Real Terms

Log, as of April 30, 2023

Sources: Brandywine Global, Macrobond (© 2023). Past performance is not an indicator or a guarantee of future results.

A regime change in the BOJ’s response? Takeaways from the recent BOJ meeting

The first yield curve control (YCC) tweak came in December 2022, when ex-Governor Kuroda widened the band to +/-0.5%. This response was aimed at relieving the market dysfunction in 10-year JGBs and the initial rise in inflation. The latest YCC tweak marks the second change, with Governor Ueda widening the trading range of the band further by another 0.5% to +/-1.0%.

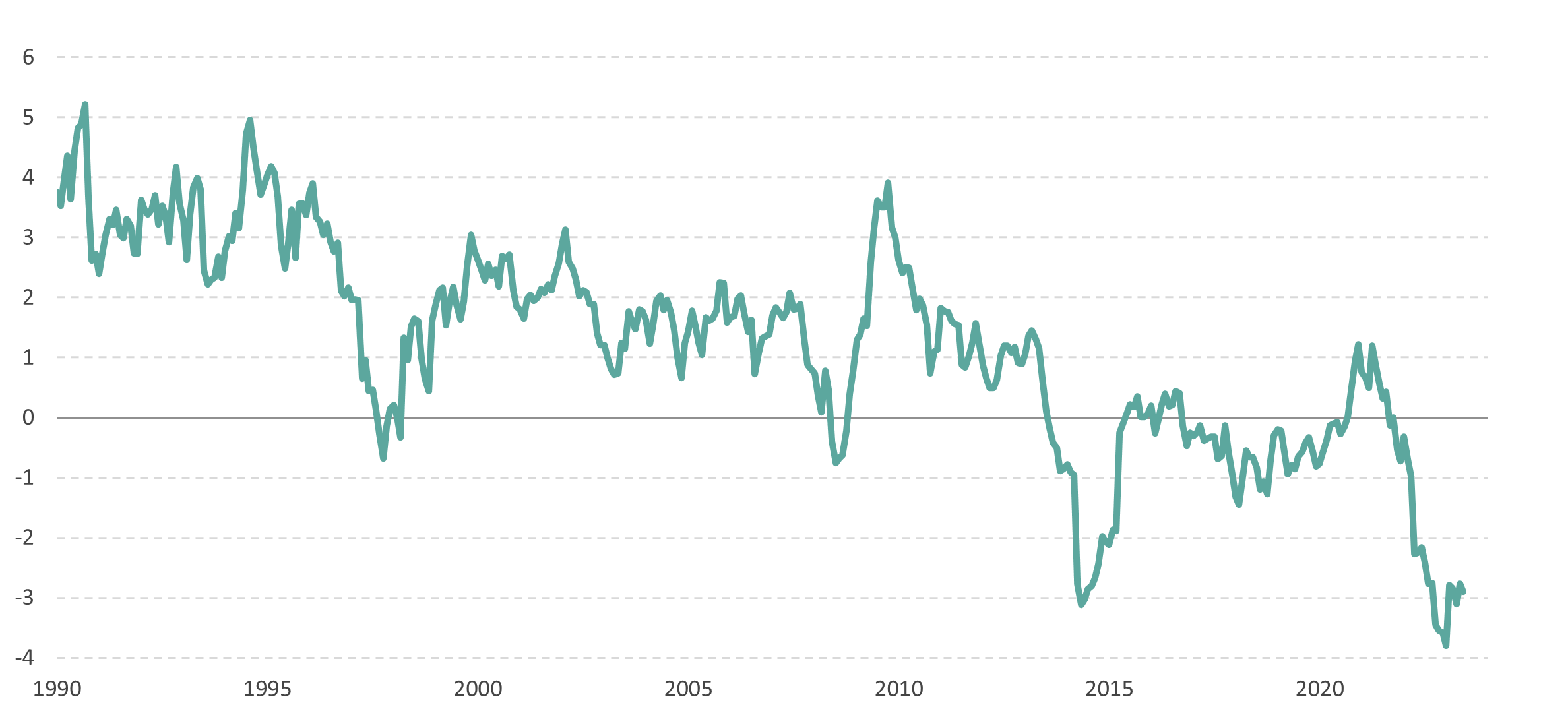

Given the broadening out in the inflation trend, a tweak to the 10-year target band was within our expectations for some kind of change in the second half of 2023. A widening in the range at this point helps to ease off market dysfunction. At the same time, it allows monetary easing in its current form to continue until the BOJ determines that normalization out of its negative interest rate policy (NIRP) is needed. A question we constantly ask ourselves: Is the BOJ comfortable keeping real yields at such a negative extreme at this juncture of growth and inflation (see Exhibit 4)?

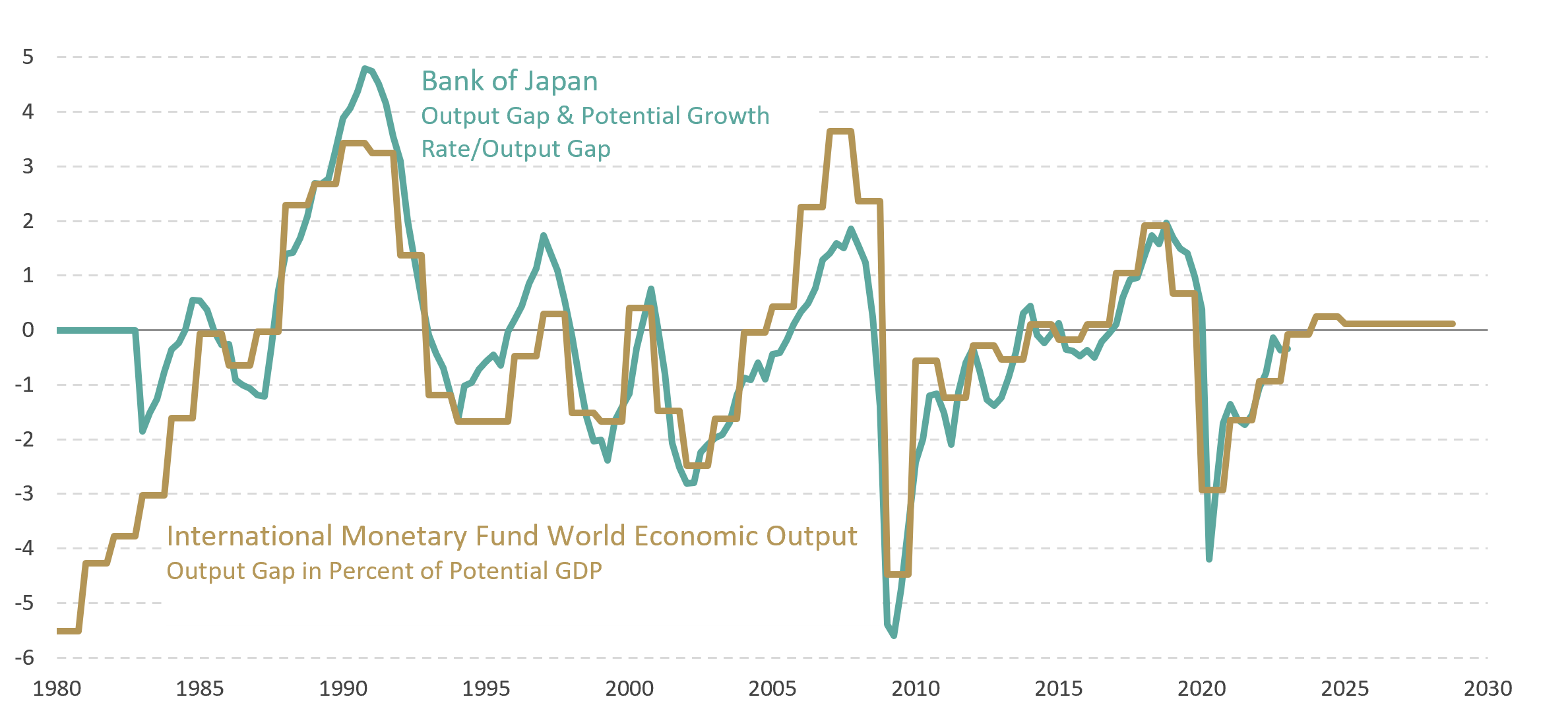

Looking ahead, we believe inflation could possibly be sustained at an average of 2% into next year, especially if the output gap starts to close in the second half of this year (see Exhibit 5). To achieve this rate, cyclical growth momentum needs to be sustained without the yen overly strengthening. The BOJ is well aware that inflation might be sustainable into next year, evidenced by the rise in the fiscal year 2024 balance of inflation risks contained in its latest economic outlook.

Exhibit 4: 10-Year Japanese Government Bond Real Yields

Percent, as of June 30, 2023

Sources: Brandywine Global, Macrobond (© 2023). Past performance is not an indicator or a guarantee of future results.

Exhibit 5: Japan: Output Gap

Percent, as of Q1 2023

Sources: Brandywine Global, Macrobond, BOJ, OECD, IMF (© 2023). There is no assurance any forecast, projection or estimate will be realized.

Are JGBs and JPY priced for the inflation and monetary policy shifts?

The latest YCC tweak led to a selloff in 10-year JGBs. However, following its meeting, the BOJ has been buying bonds with the intention of curbing market expectations on a quick renormalization process. The appreciation in the yen also has been underwhelming.

As we discussed in our March 2023 blog, we continue to believe a removal of YCC and NIRP could be a story for 2024. The timing of that reversal would be crucial. It could likely be sometime after the start of the 2024 Shunto wage negotiations as Governor Ueda has firmly supported seeing wage inflation sustained not just in 2023 but in 2024 as well.

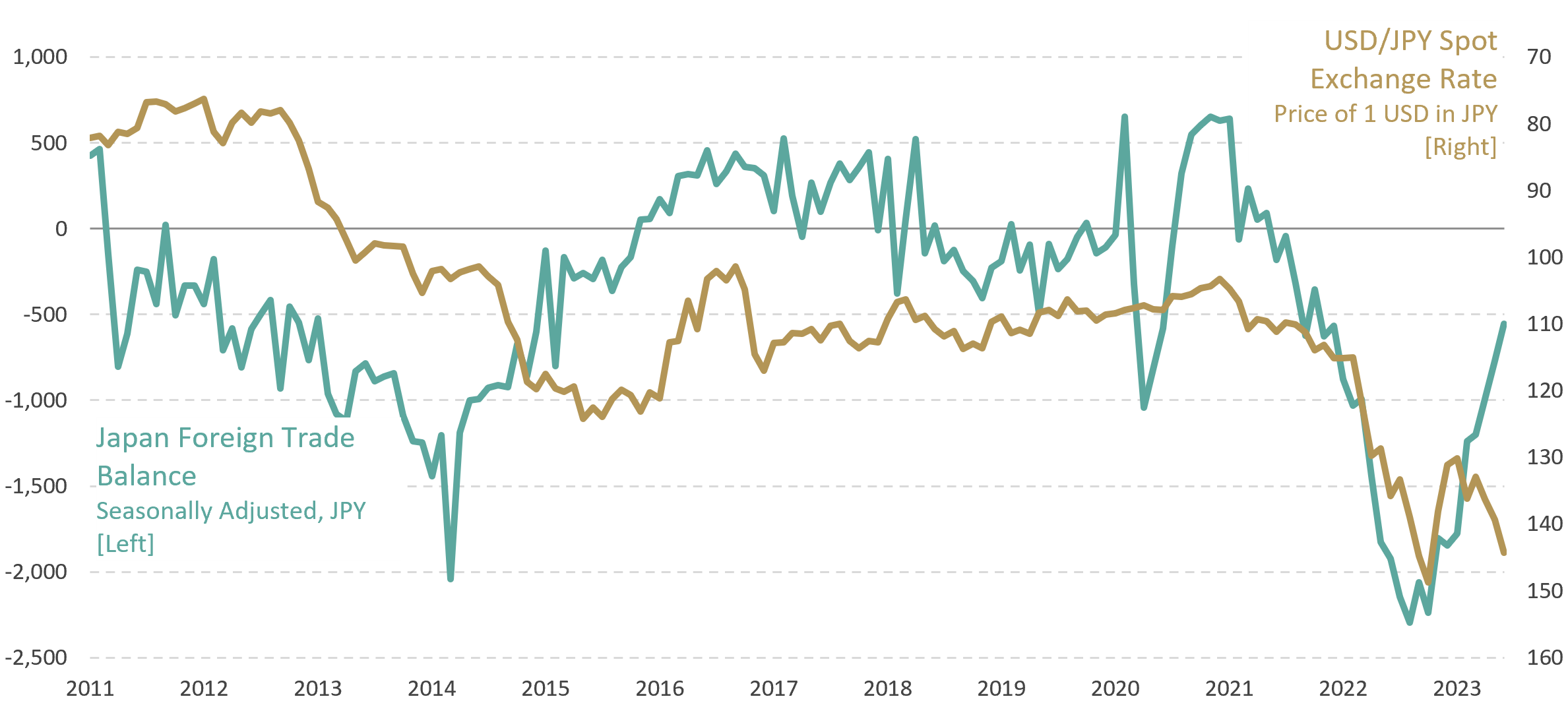

The investment implications in the medium term continue to point toward moderately higher yields in JGBs and a stronger yen. We believe a recovering current account balance in Japan and a peaking federal funds rate in the US, just as Japan is moving toward more normalization, are factors that will support the yen over the next year (see Exhibit 6).

Exhibit 6: Japan: Current Account and JPY

JPY, billion, as of June 30, 2023

Sources: Brandywine Global, Macrobond (© 2023).

Endnotes

-

Source: “Major Japan firms expect FY2023 net profit to rise 4% to record high,” The Japan Times, June 10, 2023

- Source: Shankar, V. “Investors are putting big money into Japan. Here’s why,” The New York Times, June 14, 2023.

Definitions:

The Bank of Japan (BoJ) is the central bank of Japan and is responsible for the yen currency.

The Nikkei 225 Index, or the Nikkei Stock Average, is a price-weighted equity index, which consists of 225 stocks in the Prime Market of the Tokyo Stock Exchange. It is the premier indicator of the movement of Japanese stock markets.

Shunto refers to the annual wage negotiations between enterprise unions and the employers in Japan. Beginning in February or March each spring, thousands of unions conduct wage negotiations with employers simultaneously. The practice began in 1956 when Japan's postwar economy was booming.

Yield curve control (YCC) involves targeting a longer-term interest rate by a central bank, then buying or selling as many bonds as necessary to hit that rate target.

The Tankan Survey is an economic survey of Japanese business issued by the central Bank of Japan.

A negative interest rate policy (NIRP) is an unusual monetary policy tool. Nominal target interest rates are set with a negative value, which is below the theoretical lower bound of 0%.

WHAT ARE THE RISKS?

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.