Has to Be a Compromise between Equality and Freedom.

Has to Be a Compromise between Equality and Freedom.

Most politicians, economists, journalists, etc. know about the so-called Gini coefficient, a measure of statistical dispersion intended to represent the income inequality (or wealth inequality) within a nation or group of people. At zero we have perfect equality; at 1 we have perfect inequality, one individual capturing the whole income, leaving nothing for the rest of the group. In reality, the Gini coefficient - as computed by the specialists - varies between .25 (very egalitarian societies) to .65 (very unequal ones).

Most people on the left of the political spectrum consider the most desirable result of a policy to be an ever-falling Gini coefficient, going down asymptotically towards zero, and that the role of the State should be to achieve such an outcome by force (nationalisation) or by taxes and redistribution. Each and every one of these politicians, if and when elected by more than 50% + 1 of the population, will then work steadfastly to increase taxes on the high earners and/or the “rich” to transfer money to the low earners and the poor, in order to establish the highly desirable so-called “social justice.” But, as the French philosopher Montesquieu once said, “A perfect equality of income in a country would require the whole of the political power to be exercised by only ONE man,” and this is what the story of totalitarianism in the 20th century has taught us in no uncertain terms.

As I have written often in the past, most social phenomena are distributed according to Pareto’s Law which states that 80% of car accidents are caused by 20% of the drivers. Applied here, 80% of the losses in your portfolio are caused by 20% of the positions, and then of course, 80% of the gains too, which implies that 60% of the said portfolio is just dead wood.

Now let me assume that 80% of the wealth is created by 20% of the people and for the sake of argument, we will call the wealth creative people the “entrepreneurs.” Of course, within the entrepreneurs, 80% of the money earned by this entrepreneur’s class will be earned by 20% of them, implying that 4% of the population will be responsible for 64% of the wealth creation. And amongst the entrepreneurial elite of the best 4%, we would have again 20% creating 80% of the 64%, which automatically implies that 0.8% of the population creates 51.2% of the wealth created during any period of time.

So, in a purely Darwinian world with no intervention by the State, around 1% of the population would create and earn roughly 50% of the wealth created for a Gini ratio of around .50. Therefore, it should be no surprise that 1% of the population controls 50% of the assets as this is just a result of Pareto’s Law. Refusing such reality is about as stupid as revolting against gravity or death.

However, one does not need to be a rocket scientist to infer from the set of hypotheses mentioned above that there is a built-in contradiction between the political push towards equality by the leftist politicians and Pareto’s Law which is a natural push towards inequality.

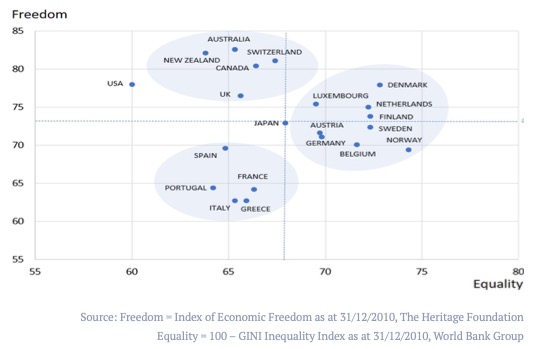

By design, the leftist politicians will take money from the efficient minority to give it to the not-so-efficient rest of the population (capturing a significant part of it for themselves and their cronies in the process) and, probably at some point, we will reach a level where the Gini coefficient will keep going down (improving in the eyes of the said politicians), but where everybody and especially the poorest will only get poorer and poorer, simply because the entrepreneurs will stop taking risks or move abroad. So, there must be some sort of a trade-off between equality and freedom, and there is, according to the graphs below. There is a generally accepted way to measure inequality - the Gini coefficient - and there is also a not-so generally accepted measure of freedom, this time provided by the Heritage Foundation. Both have long track records and the methodologies to build them have not changed for quite a while. I pass no judgment on how these two indices have been built, nor on how valid they are; I am simply trying to use them to check on the trade-offs between equality and freedom by building the following graph.

Fig. 1 Freedom Index vs. Equality Index in Developed Economies

On the Y-axis we have put the “freedom” index, and on the horizontal axis the 100-Gini coefficient to measure “equality.” The data for both indices (which move very slowly) are for 10 years ago (i.e. before the current monetary experiments), and the results for the financial markets (see second chart) are for the last twenty years.

We have three groups of countries and two outliers emerging:

The freest ones are the group gathered around the British Common Law,with Switzerland being the land of the referendums appearing in this group. There is more than one way to be free.

The least free could be called the Catholic or the “wine drinker” groups.

The third group-the group which seems to have found an optimum-is made loosely of what can be called the Lutheran Europe or the “beer drinkers.”

The two outliers are Japan (which is right in the middle as is fit for a country trying to reach the consensus all the time) and the US, which is very free but very unequal (they would drink anything, including water). This may be due partly to cultural reasons but also partly to the fact that immigration has been constant in the US for ages.

Less freedom doesn’t mean more equality but rather more inequality, as evidenced by the comparison between the Catholic group and the Common Law group (more growth in the second), or with the Lutheran group (more growth AND more equality).

The bigger the power of the State (less freedom) seems to equate with more inequality, which should surprise no one.

The “optimum” seems to have been reached by the Lutheran group, and the reason might be simple. The State passes laws for equality to be achieved (like all children must have a good education), but the supply of educational services is not provided by civil servants but by the private sector in a competitive manner (educational vouchers). The same being true for retirement benefits, as another example. The State prescribes what must be done, and the competitive private sector deals with the production side of the requirement, with the results being checked by agencies of the State.

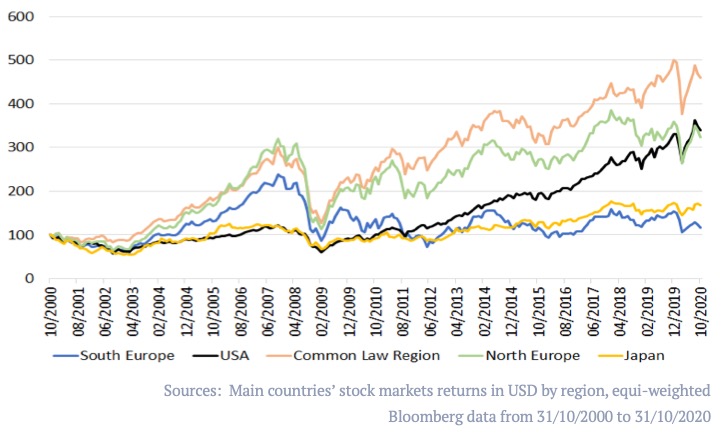

Investment Performance

We have built stock market indices for the three clusters and for the two outliers (see above). Here are the results:

Fig. 2 Stock Market Performance p.a. by Region, in USD

The winner is of course, the“freest”group.

Next comes the “optimum” group, closely tied to the US.

Then come the two laggards, Japan and Catholic Europe.

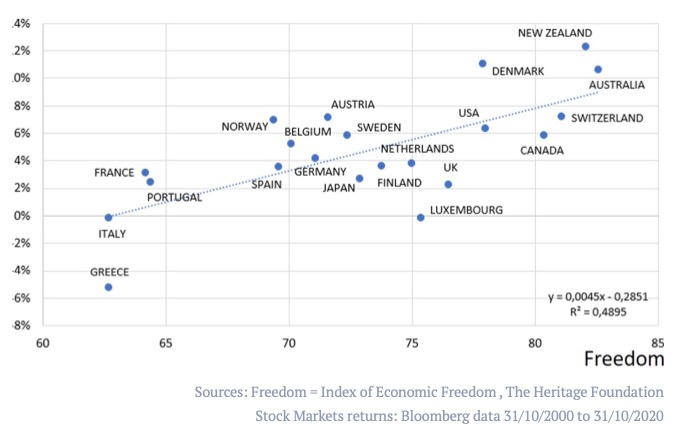

On an individual country basis, the fit between more freedom and more stock market performance is reasonably good, as evidenced by the next graph.

Fig. 3 Stock Market Performance as a Function of the Freedom Index by Country (20-Year return p.a, in USD)

Structural Consequences:

The UK should not have joined Europe but should have stayed in the Commonwealth, where the future of the country was and still is.

It is totally idiotic to try to fix an exchange rate between countries belonging to different clusters. One could perhaps fix the exchange rates inside Lutheran Europe or inside Catholic Europe, but having the same exchange rate for both is plain stupid.

For those wishing to index their portfolios, it would make a lot of sense to have an indexed portfolio for each cluster which corresponds to a cultural reality, rather than indexing to something as arbitrary and inefficient as “Euro-Europe” and non “Euro- Europe,” which will not last.

Developed economies’ portfolios should be concentrated in the US, the Common Law area and the Lutheran countries.

The most stable cluster has to be Lutheran Europe, the safest legally is the Common Law area, and the most Schumpeterian one, the US.

How surprising!

© Gavekal Intelligence Software. Redistribution prohibited without prior consent. This report has been prepared by Gavekal Intelligence Software mainly for distribution to market professionals and institutional investors. It should not be considered as investment advice or a recommendation to purchase any particular security, strategy or investment product. References to specific securities and issuers are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.