2021 and 2022 were among the worst years for fixed-income investors in developed markets in world history. Bonds lost money. Stocks lost money. Crypto lost money. Inflation rose to levels not seen in Europe since the 1980s. The only thing that rose in value were commodities. You have to go back to the Civil War in the United States or the Napoleonic Wars in Britain to find a worse year than 2022. There was nowhere to hide.

When prices started to increase in 2021, the Federal Reserve warned that the inflation would be temporary and that investors should not worry about it, but inflation continued to rise throughout the world and did not go away. Inflation rose to double-digit levels in Germany, the United Kingdom and in other countries. Germany suffered its highest inflation since 1950. In February 2022, Russia invaded Ukraine. By the time central banks were willing to admit that inflation was approaching levels the developed world hadn’t seen in 40 years, it was too late. Central banks had to act quickly to stop inflation from becoming endemic in the global economy. No central bank wanted to see a repeat of the 1970s when inflation turned into stagflation.

During 2023, bond yields risen even higher in many countries, and in October 2023, it looked as if investors could have a third year of negative returns. But during the last two months of the year, bond yields fell dramatically as fears of inflation subsided and the anticipation of lower interest rates in 2024 drove bond yields down. Stocks provided positive returns as well after losing money in 2022. However, the gains in bond markets were not sufficient to offset the losses that had occurred during 2021 and 2022. It will take several more years for investors to get back to where they were at the beginning of the decade.

Declines in British Bonds

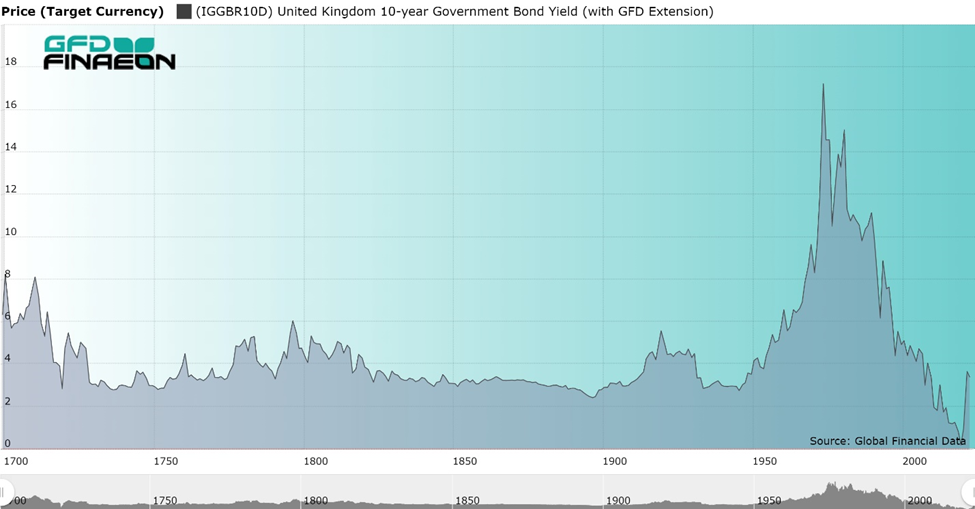

For a long-term perspective, to understand how these events affected the bond market, we need to look at London. The United Kingdom was the world’s financial center until World War II and is still the financial center of Europe. The British Consol traded in London between 1753 and 2015 and for most of Britain’s history, it was the global benchmark for government bonds. The yield on British bonds over the past 300 years is provided in Figure 1. What you see is a gradual decline in bond yields during the 1800s, followed by two periods of rising and then falling bond yields, between 1896 and 1945, peaking in 1920, and between 1945 and 2020, peaking in 1974. Yields rose back to the 4% level in 2023.

Figure 1. United Kingdom 10-year Government Bond Yield, 1700 to 2023

British fixed-income investors lost money during both 2021 and 2022 just as did investors in the United States and other developed countries. By our estimates, British fixed-income investors lost 6.25% in 2021 and 20.2% in 2022. British consumer inflation was 7.54% in 2021 and 13.44% in 2022. You have to go back to July 1803 during the Napoleonic Wars to find a larger nominal loss to bond investors in the UK. This produced a real loss of 14.3% in 2021 and 36.3% in 2022 or 55% between 2021 and 2022. Who would have put their money in “risk-free” government bonds anticipating that they would have lost half of their money after inflation in only two years? The British government may not have defaulted on their bonds, but lower bond prices and inflation reduced returns significantly.

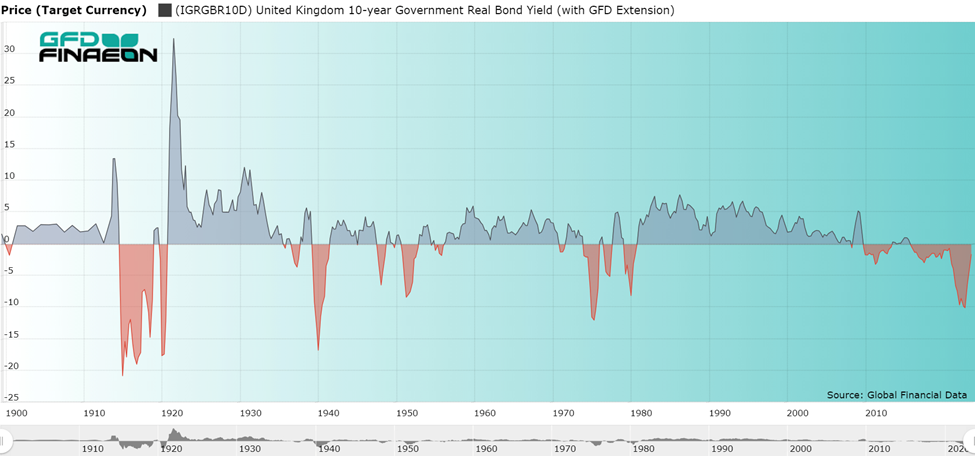

Figure 2. United Kingdom Real 10-year Government Bond Yield, 1875-2023

Inflation is the worst enemy of fixed-income investors and war is one of the major causes of inflation. The real return to fixed-income investors in Britain is illustrated in Figure 2. You can see the negative real yields during World War I, the Great Depression, World War II and the inflation of the 1970s. Unfortunately, during the twenty-first century, the real yield to investors has been negative more often than it has been positive as the Bank of England tried to stimulate the economy by keeping interest rates low.

Britain suffered 19% inflation in 1974 when the British bond index had a 19% decline producing a 41% total loss after inflation. 1974 was also one of the worst years in stock market history when the British stock market plunged 51.8%, worse than the decline during the Great Depression. Luckily the stock market recovered by 152% in 1975 and the bond market recovered by 37.9% in 1975. Although bond and stock markets are unlikely to recover by that much in 2023, the worst of the decline for British investors is over with.

Britain needs to get inflation under control so that fixed-income investors can once again beat inflation. No matter how much the Bank of England reduces inflation, it will be the 2030s before British fixed-income investors will recover the losses they have suffered during 2021 and 2022.

Global Bonds Reverse Two Years of Declines

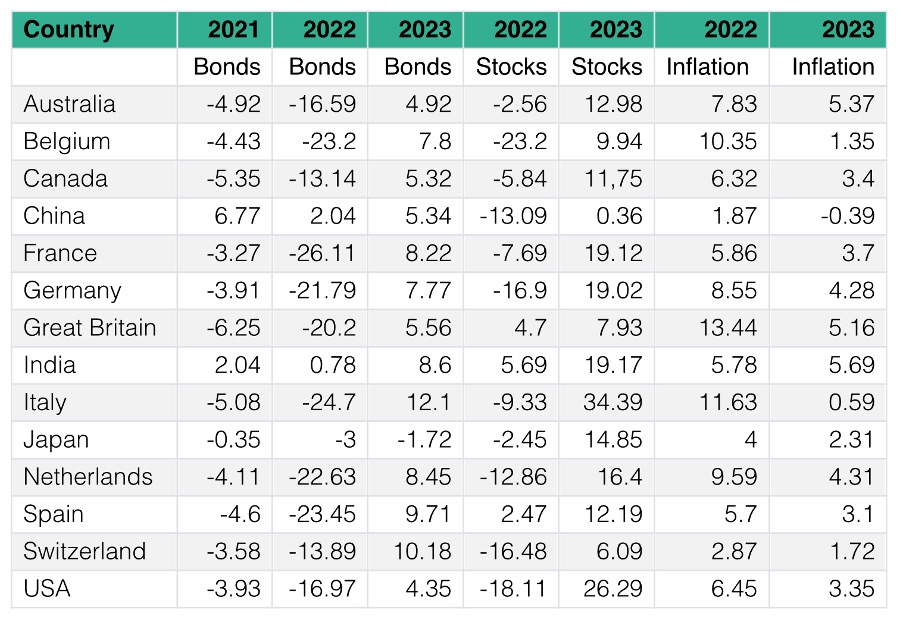

It wasn’t only in the United Kingdom that fixed-income investors lost money during 2021 and 2022. Losses occurred in most developed markets. This is illustrated in Table 1 which shows the returns to investors in 10-year government bonds in 15 different countries as well as the return to stocks in 2022 and 2023 and the inflation rate in 2022 and 2023. After inflation, fixed-income investors in many countries lost over 30% in one year. All developed markets suffered losses, and the only two markets that had positive returns during the past two years were China and India. In most countries, the losses in the bond market were greater than the losses in the stock market.

Fixed-income investors in all of the developed markets lost money in both 2021 and 2022. The smallest losses were in Japan where government intervention in the bond market kept bond yields from rising. The Japanese government has recently raised the ceiling on 10-year Government Bond yields from 0.25% to 1.00%, but has not permitted higher yields to prevail, though there is growing pressure on the Bank of Japan to eliminate its yield ceilings.

Table 1. Global Stock and Government Bond Returns in 2021, 2022 and 2023

The rest of the developed world has allowed the market to set the yields on government bonds. Central Banks in Europe have raised the discount and lending rates that they charge. The European Central Bank raised its lending rate from 0.25% in July 2022 to 4.75% in September 2023. Because bond yields were lower in Europe than in the United States in 2021, in many cases they were negative, investors suffered larger losses as bond prices collapsed more in Europe than in the US. Moreover, few stock markets in Europe did well in 2022 as the anticipation of higher interest rates and bond yields hit investors hard. The era of zero yields that began with the Great Financial Crisis of 2008 is over. Central banks will have to keep yields positive for the foreseeable future.

Bond yields have risen, and fixed-income investors have suffered double-digit losses in every country in Europe. Yields on 10-year government bonds were negative at the beginning of 2021 but yields on the 10-year bond have risen to positive levels in all European countries. Most of the increase in yields occurred in 2022 rather than 2021. Every country saw the inflation rate decline in 2023.

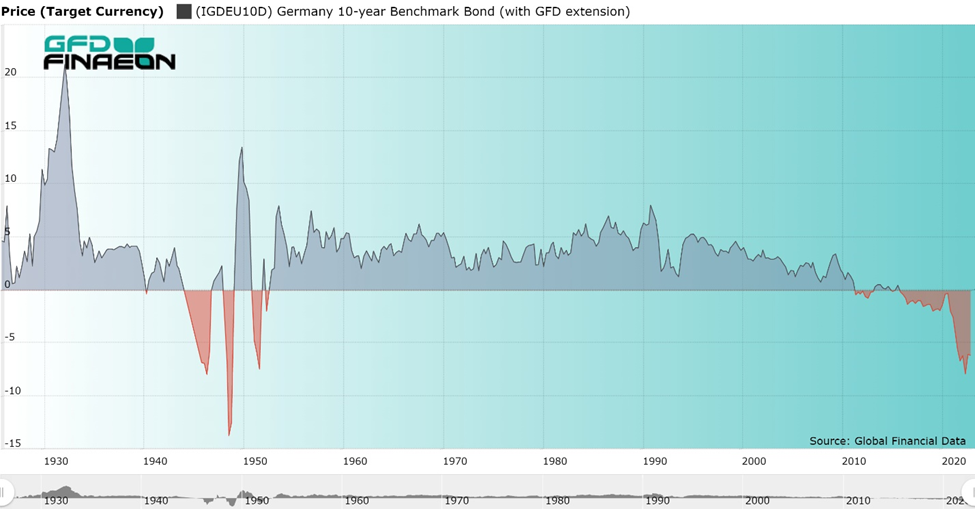

Germany provides an example of the impact of these policies. As Figure 3 shows, after adjusting for inflation, German yields have been consistently negative since 2015. It is interesting to note that real yields on German bonds were consistently positive between 1952 and 2010. The European Central Bank has not only reduced central bank interest rates, but real German bond yields have been pushed down to negative nominal and real levels, contrary to German financial history between 1952 and 2010. Central banks in almost all developed countries produced policies that have created negative real yields to help the economy recover. But how long can these policies continue?

Many investors expect that the dramatic increase in interest rates in 2022 and 2023 has come to an end, and the next change in central bank rates will be a decrease, not an increase. Barring some unexpected increase in inflation rates in 2024, the next change in interest rates should be downward. This will drive bond yields down, not up.

Figure 3. German 10-Year Bond Yields After Inflation, 1925 to 2023

As Table 1 shows, all European fixed-income investors received positive returns in 2023. Only Japanese investors saw losses. However, if you look at real bond yields, they are likely to remain negative. Inflation is still a problem in Europe. Only when central banks once again get inflation under control, will bondholders receive a positive real return. Fixed-income investors may spend the rest of the 2020s trying to earn back the losses that occurred during 2021 and 2022.

A Lost Decade for Fixed Income?

Fixed-income investors throughout the developed world endured one of the worst bear markets in history in 2021 and 2022. The only times in the past when fixed-income investors received worse returns was when there was a war or hyperinflation. US investors haven’t seen a worse year since the Civil War and UK investors since the Napoleonic wars. Luckily, during the past 230 years, US fixed-income investors have never suffered three successive years of losing money in government bonds.

Central banks must get inflation under control if investors are to get returns that beat inflation and earn back the losses they suffered during 2021 and 2022. In a country like Britain where real losses exceeded 50% during 2021 and 2022, it will be the 2030s before investors fully recover. Britain is not alone in this. It may well take the rest of the decade for most European investors to recover from the losses of 2021 and 2022.

With bond yields declining for four decades in a row between 1974 and 2020, this bear market was inevitable. It was only a question of when this bear market would occur, not if. When the Great Financial Crisis took place in 2008 and central banks pushed interest rates and government bond yields to negative levels, they knew they could not keep interest rates low forever. A day of reckoning was due when central banks would have to raise interest rates to levels consistent with historical norms. Even today, discount rates and bond yields remain below the inflation rate imposing negative real yields on investors. Who says government bonds are risk free?

It will take the rest of the decade for fixed-income investors to recover from the losses of 2021 and 2022, but slow recovery is better than continued losses.