The great Milton Friedman famnously referred to inflation as a disease.

Adrian Owens, Investment DIrector; Rahul Mathur, Investment Manager

GAM Investments, 09 March 2021

The great Milton Friedman famnously referred to inflation as a disease. GAM Investments' Adrian Owens and Rahul Mathur discuss why the unfolding macro backdrop is in fact presenting compelling opportunities across a diverse range of government bonds and currencies.

“Inflation is always and everywhere a monetary phenomenon.” – Milton Friedman

Diagnosis

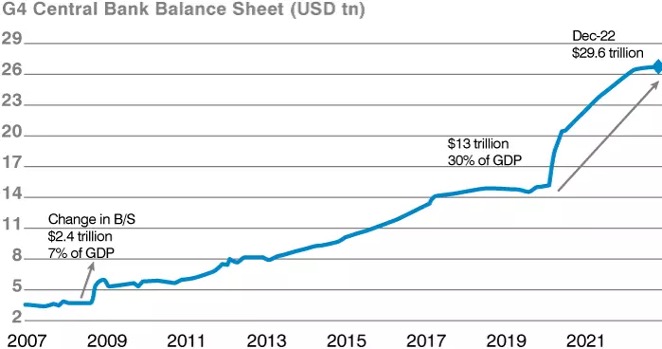

Almost a year on from the onset of the Covid-19 pandemic, it is clear that policymakers are willing to run their economies ‘red hot’ in order to generate above-target inflation. Given the exogenous nature of the Covid-19 shock, policymakers have been unfettered by the moral hazard concerns that constantly stalled their response in the global financial crisis (GFC). This has been evident in both the magnitude and speed of the policy reaction to the Covid-19 crisis versus 2008. We can see the impact of the expansion of central bank balance sheets on key monetary variables (for January 2021: US money supply M2 +26% year-on-year, UK money supply M4 +13% year-on-year, euro area money supply M3 +13% year-on-year). In the long run, we know that there is a close relationship between broad money growth and inflation. All of this is reinforced by central bank rhetoric. In contrast to previous cycles, when the Federal Reserve (Fed) tightened policy well before inflation moved sustainably above 2%, central banks have been explicit that this is now unlikely to be the case, allowing any initial increase in inflation more time to take hold.

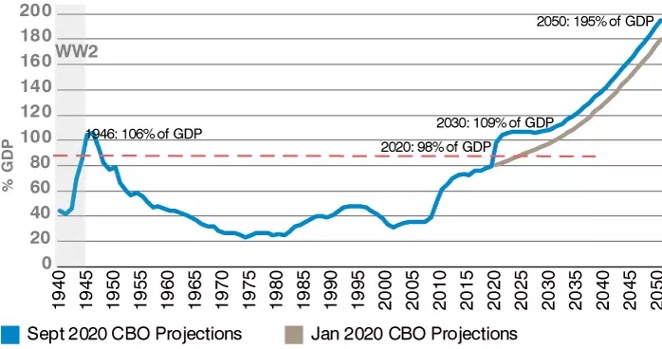

Chart 1: Unprecedented debt – US federal debt held by the public (% of GDP)

Source: Congressional Budget Office (CBO), Deutsche Bank, Haver Analytics, Bank of England, European Central Bank, International Monetary Fund, Morgan Stanley Research. Data as at January 2021. For illustrative purposes only.

Chart 2: Unprecedented QE – G4 central bank balance sheets (USD trillions)

Source: Morgan Stanley Cross-Asset Playbook – Three Catalysts for an Overshoot. Data as at February 2021. For illustrative purposes only.

On the fiscal front, there are likely only three ways that governments can deal with the huge amount of debt being issued: 1) default 2) raise nominal growth to pay down debt 3) deflate the real value of debt through creeping inflation. The latter is the only expedient option for policymakers today. In terms of the magnitude of the fiscal response, pandemic-related unemployment has cost US households USD 330 billion in lost wage income, but the same households have already received USD 1 trillion in aggregate transfers. That figure excludes Joe Biden’s imminent fiscal spend. US households are presently sitting on excess savings of USD 1.4 trillion. This is a huge amount of fuel for pent-up demand, which is likely to meet constrained supply as the economy reopens.

“Only government can take perfectly good paper, cover it with perfectly good ink and make the combination worthless.” – Milton Friedman

Observable symptoms

We are already seeing signs of margin expansion in high demand sectors (household appliances, hardware). Housing rents represents 40% of the core consumer price index (CPI) in the US. In the year to Q4 2020, median asking rents grew at the fastest pace on record (+18% year-on-year). January’s Prices Paid Index, a sub-component of the Institute of Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI), is at decade highs. Outside of the US, commodity and oil prices are providing a near-term inflationary impulse. Spot containerised freight rates from Shanghai are three times the levels they were in May 2020 and this is consistent across other freight indices.

The Fed’s dot plot, used to signal the outlook for the path of interest rates, shows the first hike in 2023. We think it is highly likely that core personal consumption expenditure will be above the Fed’s target by the end of 2021, which potentially sets the scene for a collision between the Fed and the market later this year.

“Inflation is the one form of taxation that can be imposed without legislation.” – Milton Friedman

Recommended treatment

We believe reflation, inflation protection, fiscal sustainability and value are currently the most compelling themes in fixed income and FX. Long 10-year and 30-year US inflation break even swaps represent one direct way of potentially taking advantage of higher inflation expectations. The US CPI has averaged around 2.5% over the last 30 years while 10-year and 30-year break evens are currently trading at 2.2-2.3%. We expect curves to steepen on the back of reflation and fiscal incontinence.

More idiosyncratic, relative value expressions of the broader themes could also be considered. For example, economic data in Norway remains strong. The country is a commodity exporter and Norges Bank is one of the few central banks projecting rate hikes later this year. From a fiscal perspective, we believe the Norwegian krone benefits from the quirk that Norway’s sovereign wealth fund must sell FX to purchase Norwegian krone in order to finance fiscal spending. In our view, Norway is exceptional in terms of fiscal sustainability - the sovereign wealth fund’s assets under management outweigh public debt, meaning Norway has the enviable advantage of a negative gross financing need. Other potential relative value trades which pick up on relative idiosyncratic factors in addition to divergences in the growth / inflation / fiscal outlooks could include positions in the UK and New Zealand versus Canada, for example, and in the front end of the Australian government debt market versus the US, for instance.

Ultimately, we believe market participants are underestimating inflation risks and, in our view, the opportunity set across fixed income and currencies looks compelling.

Important legal information

The information in this document is given for information purposes only and does not qualify as investment advice. Opinions and assessments contained in this document may change and reflect the point of view of GAM in the current economic environment. No liability shall be accepted for the accuracy and completeness of the information. Past performance is no indicator of current or future trends. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a security is not a recommendation to buy or sell that security. The securities listed were selected from the universe of securities covered by the portfolio managers to assist the reader in better understanding the themes presented. The securities included are not necessarily held by any portfolio or represent any recommendations by the portfolio managers. There is no guarantee forecasts will be achieved.