With long-term bond yields down about half a percentage point from their early-2021 not-so-high highs, chatter has inevitably returned to high-dividend stocks as an alternative income generator. While 10-year US Treasurys pay a paltry 1.35%, the MSCI World High-Dividend Yield Index boasts a 3.44% yield, spurring an avalanche of headlines like “5 High-Yield Dividend Stocks for Healthy Income” and “6 Dividend Stocks With Big Payouts and Less Risk.”[i] What better time, in our view, to explain once again why high-dividend stocks aren’t the magic solution to all your investing dilemmas?

Dividends have long had the reputation as steady workhorses that churn out reliable payments while avoiding the brunt of the stock market’s occasional declines. If we were to hazard a guess, we would posit that this stems from days gone by, when dividend checks came in the mail, there was no CNBC or Internet, and tracking stock prices required a daily perusal of your newspaper’s Business section. That took deliberate effort, whereas the checks just showed up, giving the perception of stability.

It is a quaint, comforting image—and wrong. We like dividends! But they aren’t special. They don’t add to returns. They aren’t even a return on your investment—they are a return of your investment. Every time a company pays a dividend, the exact dollar amount is removed from the share price. The company is basically slicing off a small piece of its total value and sending it to shareholders. It can be hard to see due to market volatility, but by rule, every time a stock pays a $1 dividend, the share price falls by $1.

Dividends are an important piece of total return, and part of the reason is the cash payouts itself. However, the reinvestment of that cash and the subsequent return on it matters much more. That is what total return is: Price movement plus reinvested dividends. Accordingly, to accurately compare high-dividend payers and the broader stock market, you have to tune down your biases and objectively compare their total returns.

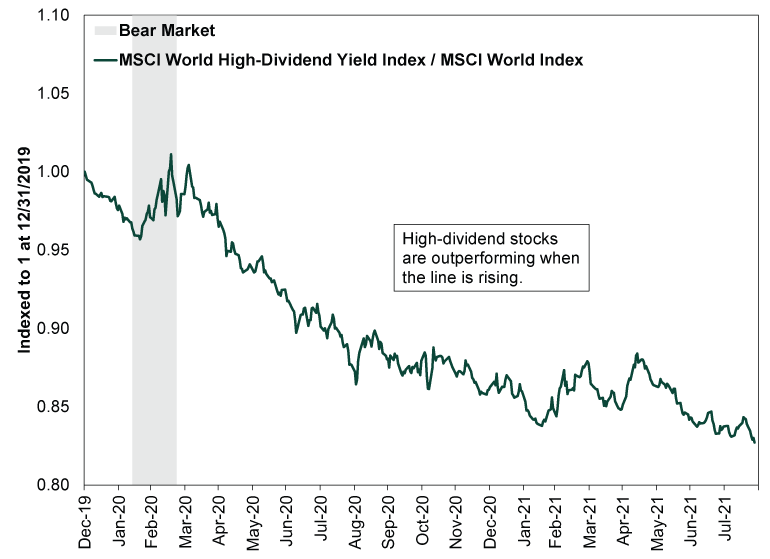

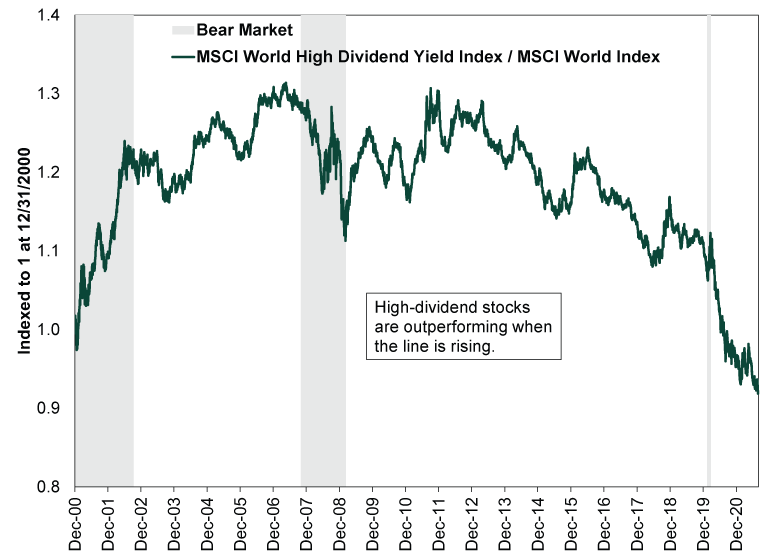

Do so, and you will see high-dividend-paying stocks aren’t inherently superior to other stocks. Forgive the tautology, but stocks are stocks, period. They are all volatile from day to day, week to week, month to month and year to year. Bear markets hit high-dividend stocks and low- or no-dividend stocks alike. Sometimes high-dividend payers outperform the broader market. Sometimes they don’t. As Exhibit 1 shows, high-dividend payers have trailed the broader market quite badly since 2020 began, with the outperformance during last year’s short, lockdown-induced bear market a brief countertrend. Lest you think high-dividend stocks have special bear market powers, however, consider Exhibit 2, which compares high-dividend and broad developed stock markets since daily data begin at the end of 2000—high-dividend stocks took a disproportionate beating during the bear market that accompanied the global financial crisis in 2007 – 2009. That is also when several high-dividend-paying Financials companies cut payouts investors had taken for granted for eons. In other words, dividends and safetyaren’t synonymous.

Exhibit 1: High-Dividend Payers Have Had a Rocky Stretch

Source: FactSet, as of 8/30/2021. MSCI World and MSCI World High-Dividend Yield Index returns with net dividends, 12/31/2019 – 8/27/2021. Indexed to 1 at 12/31/2019.

Exhibit 2: Make That a Rocky Decade?

Source: FactSet, as of 8/30/2021. MSCI World and MSCI World High-Dividend Yield Index returns with net dividends, 12/31/2000 – 8/27/2021. Indexed to 1 at 12/31/2000.

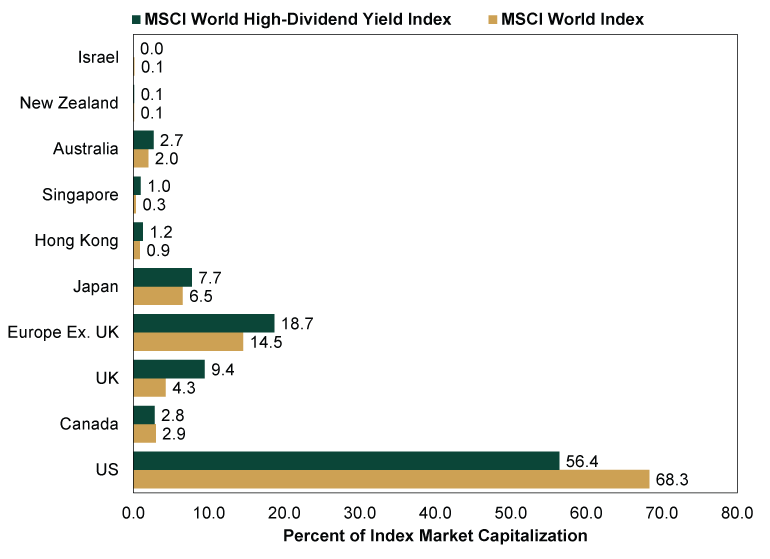

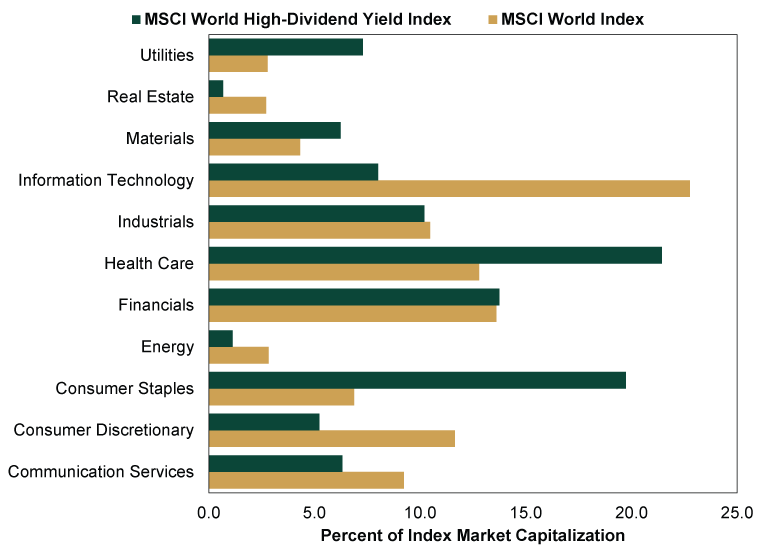

High-dividend payers’ underperformance doesn’t mean they are inherently inferior. But neither are they inherently superior. They simply tend to have different categorical weights and concentrations in terms of geography, sector and style. As Exhibit 3 shows, compared to the MSCI World Index, high-dividend stocks are significantly underweight to the US and overweight Europe and the UK. This is largely because, as Exhibit 4 shows, the high-dividend realm is very light on Tech and Tech-like stocks and overexposed to Utilities, Health Care and Consumer Staples. These are all defensive- and value-heavy areas, making a high-dividend portfolio basically a play on defensive-and-value oriented stocks. Over the past 20 years, the MSCI World High-Dividend Yield Index’s return relative to the MSCI World Index has a correlation of 0.51 with the MSCI World Value Index’s return relative to the MSCI World Growth Index.[ii] A correlation of 1 is identical movement and -1 is polar opposite, so a 0.51 correlation means high-dividend and value stocks outperform in tandem much more often than not. That works out well when value does well, but not when growth is leading—and growth has led for the past few years.

Exhibit 3: High-Dividend Paying Stocks Are Biased Toward Value-Heavy Countries …

Source: FactSet, as of 8/30/2021. MSCI World High-Dividend Yield and MSCI World Index country weightings on 8/27/2021.

Exhibit 4: … And Value-Heavy Sectors

Source: FactSet, as of 8/30/2021. MSCI World High-Dividend Yield and MSCI World Index sector weightings on 8/27/2021.

This is why we always encourage people to change their frame of reference when thinking about how to generate money from their portfolio. Too often, people think only of portfolio income, e.g., dividends and interest—a very limiting mindset. We think it is more beneficial to think in terms of simple cash flow instead—in other words, the total amount you need to withdraw each month or year. Then give yourself an array of options to generate that cash, including selling securities—a tool we call homegrown dividends. When you approach it this way, then it becomes much less about yield and much more about the rate of return you’ll need in the long run to minimize the likelihood of outliving your assets. You can manage for total return and capitalize on broad sector, country and style trends without being hamstrung by one arbitrary variable.

If that sometimes includes a gaggle of high-dividend payers, great! But consider that a happy side effect, and don’t get too attached.

[i] Actual headlines from Kiplinger and Barron’s. Oh and the data here are from FactSet, as of 9/9/2021. 10-year US Treasury Yield (Constant Maturity) and MSCI World High-Dividend Yield Index dividend yield on 9/9/2021.

[ii] Source: FactSet, as of 8/30/2021. MSCI World High-Dividend Yield Index, MSCI World Index, MSCI World Value Index and MSCI World Growth Index returns with net dividends, 8/31/2001 – 8/30/2021. Correlation calculation uses weekly change in MSCI World High-Dividend Yield Index / MSCI World Index and MSCI World Value Index / MSCI World Growth Index, all indexed to 1 at 8/31/2001.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.