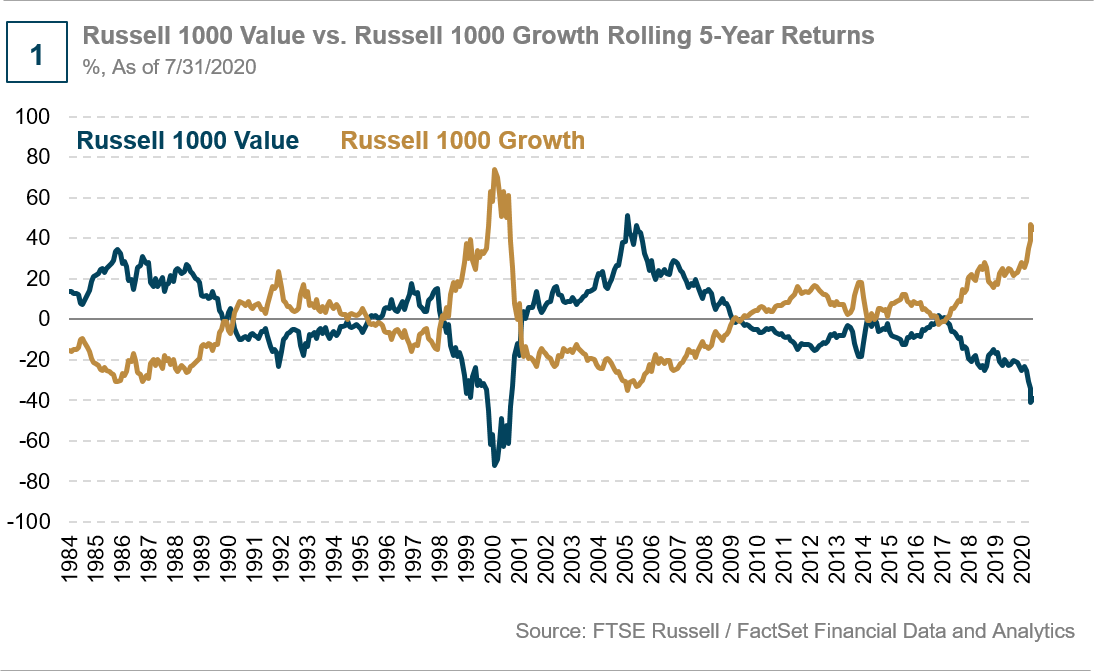

Value stocks have lagged growth stocks for some time, but the disparity has become particularly acute this year.

Michael J. Fleisher, Portfolio Manager

Brandywine Global, Around the Curve, 14 September 2020

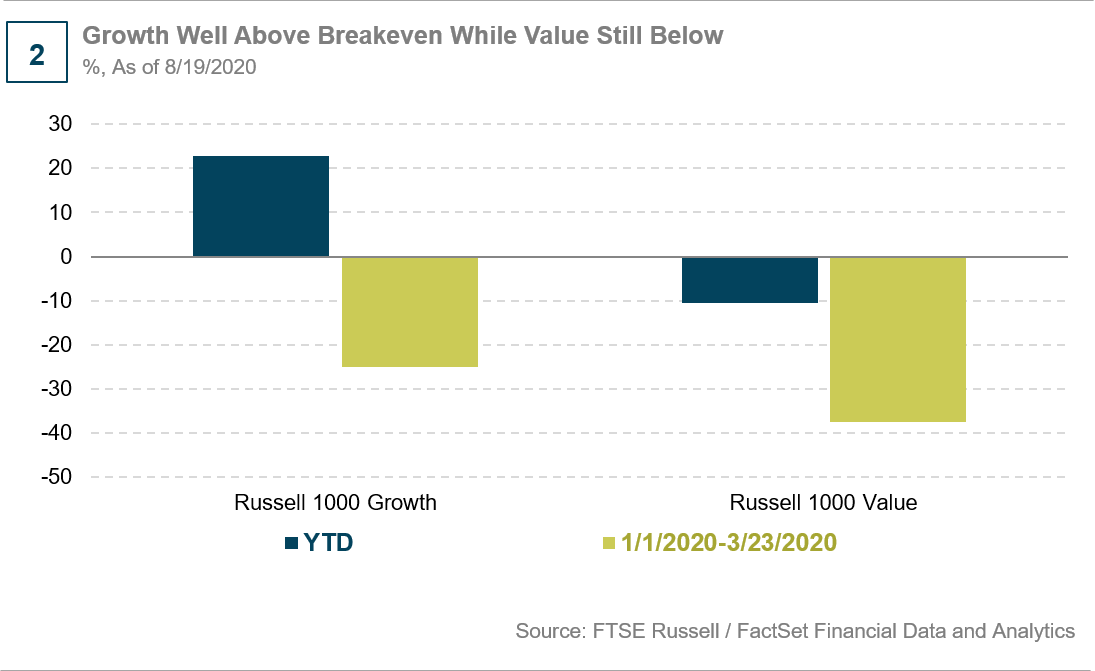

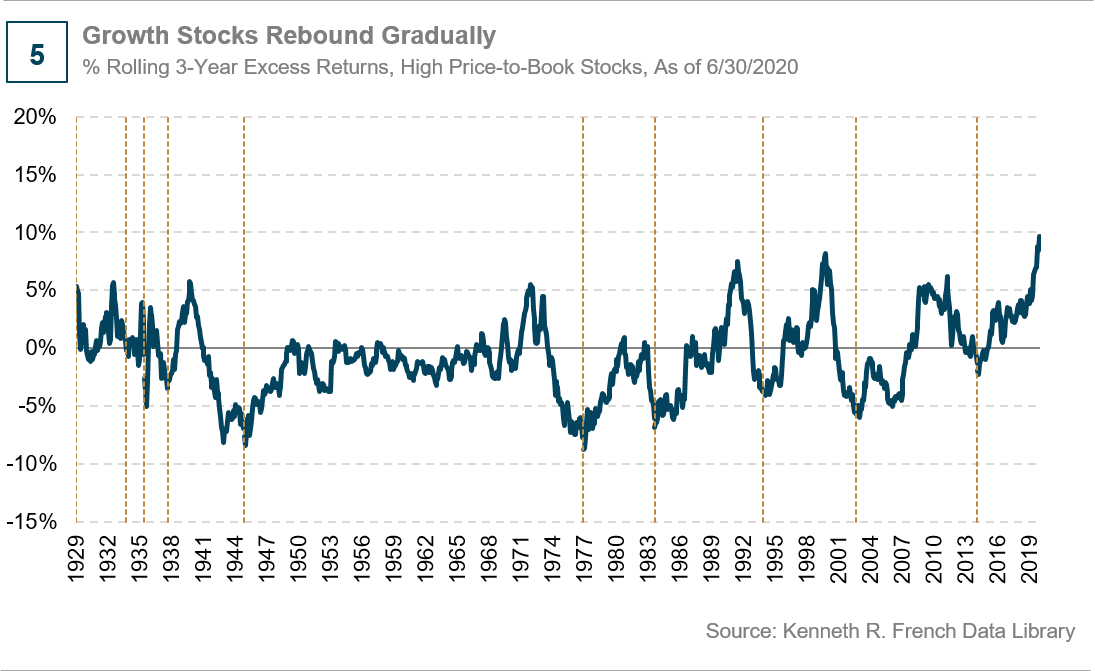

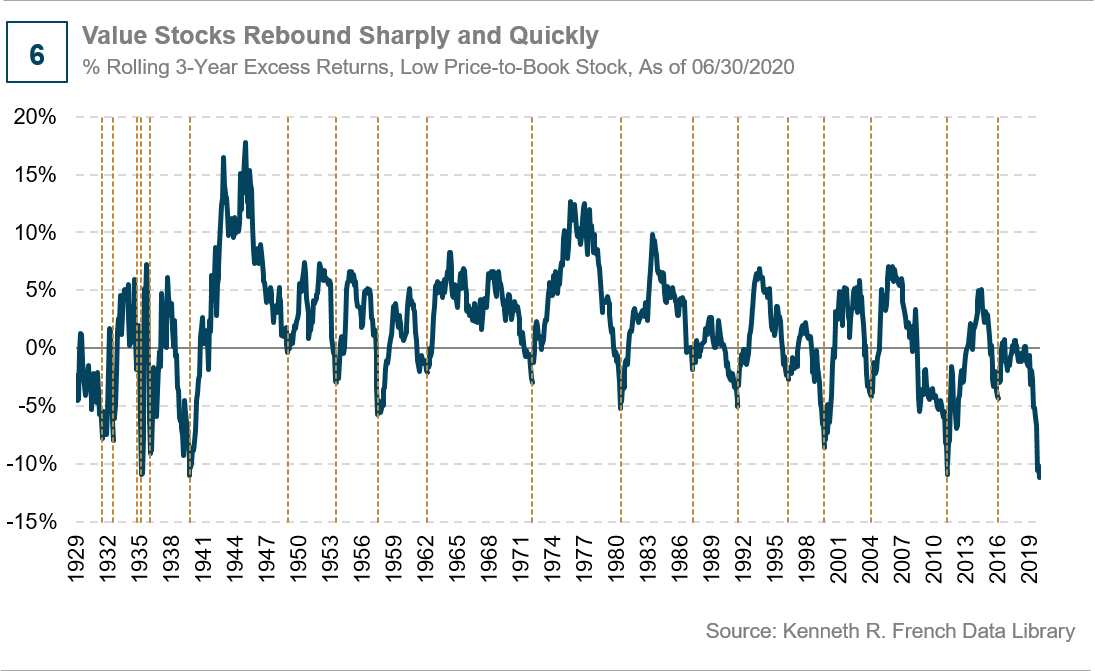

Value stocks have lagged growth stocks for some time, but the disparity has become particularly acute this year. Growth stocks have rebounded from their March lows while value stocks generally remain below the breakeven point as measured by the Russell 1000 Growth and Russell 1000 Value Indices.

Still Room to Catch the Deep Value Wave

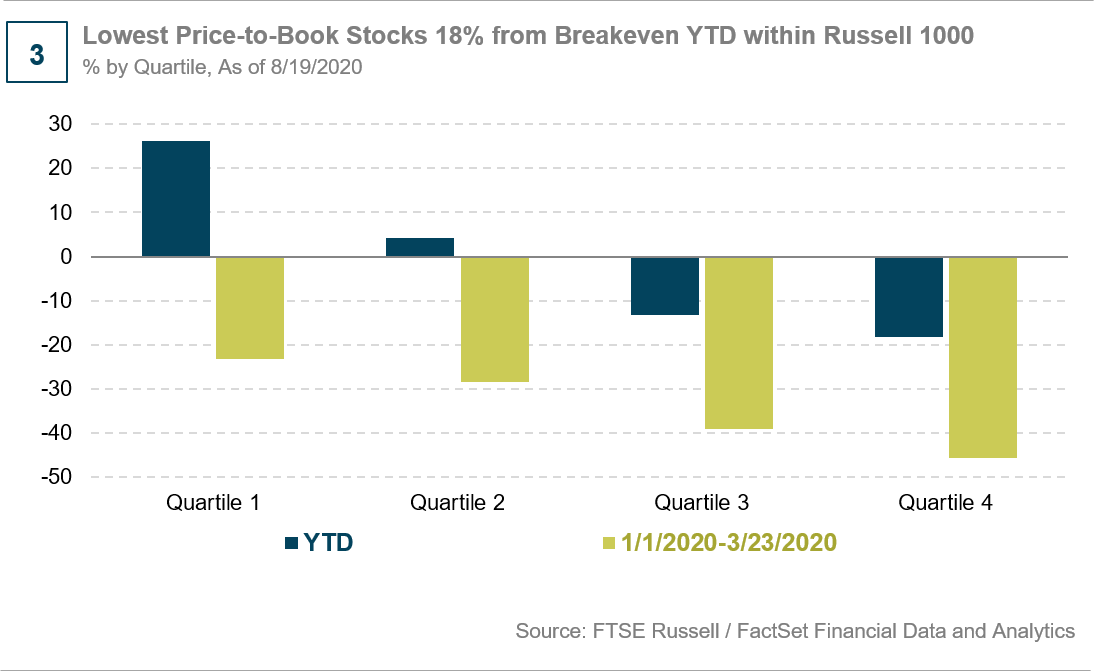

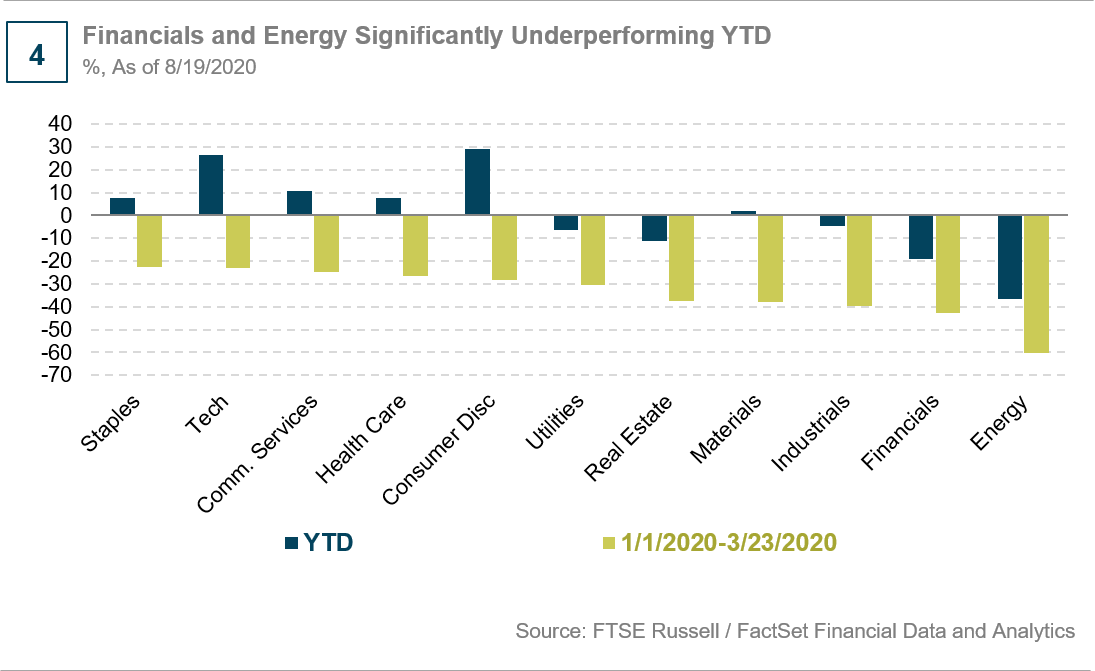

Furthermore, within value, the cheapest quartile stocks generally remain up to nearly 20% below breakeven from their March lows. Certain sectors, including energy and financials, have lagged significantly. This disparity suggests a shift may be yet to come from broad value to deep value stocks—and the snapback in deep value stocks could be significant.

But the Snapback May Be Sharp and Quick

When the shift to value occurs, it could come suddenly. A comparison of the historical return patterns of high price-to-book stocks with lower-priced stocks shows that value stocks tend to recover more sharply. And, their rebounds may be recouped over shorter time spans than growth stocks, which tend to see outperformance extended more gradually over longer time periods.

Not One or the Other

Rather than a choice between growth or value, there is likely a role for both. However, even carefully blended portfolios may be unknowingly or significantly overweight to growth stocks given the extended outperformance of higher-priced stocks and the tendency for major equity indices to be skewed heavily toward growth. Revisiting value exposure, particularly within deeply valued sectors, may be beneficial for several reasons. Investors, particularly those who missed the strong recovery in growth stocks, may be at risk of missing the rebound in value stocks given their tendency for sharp, quick reversals. Value’s recovery may not require an outright collapse in the outperformance of technology stocks but only a slowdown in the pace of gains for growth stocks. Furthermore, growth stocks have been behaving defensively, similar to a bond proxy, during the pandemic. When this relationship decouples, and gains in higher-priced stocks begin to slow, investors overweight to growth may find themselves overexposed to risk.

Groupthink is bad, especially at investment management firms. Brandywine Global therefore takes special care to ensure our corporate culture and investment processes support the articulation of diverse viewpoints. This blog is no different. The opinions expressed by our bloggers may sometimes challenge active positioning within one or more of our strategies. Each blogger represents one market view amongst many expressed at Brandywine Global. Although individual opinions will differ, our investment process and macro outlook will remain driven by a team approach.