Why should long-term investors care about market forecasts? Vanguard, after all, has long counseled investors to set a strategy based on their investment goals and to stick to it, tuning out the noise along the way.

Why should long-term investors care about market forecasts? Vanguard, after all, has long counseled investors to set a strategy based on their investment goals and to stick to it, tuning out the noise along the way.

Why should long-term investors care about market forecasts? Vanguard, after all, has long counseled investors to set a strategy based on their investment goals and to stick to it, tuning out the noise along the way.

The answer, in short, is that market conditions change, sometimes in ways with long-term implications. Tuning out the noise—the day-to-day market chatter that can lead to impulsive, suboptimal decisions—remains important. But so does occasionally reassessing investment strategies to ensure that they rest upon reasonable expectations. It wouldn’t be reasonable, for example, for an investor to expect a 5% annual return from a bond portfolio, around the historical average, in our current low-rate environment.

“Treat history with the respect it deserves,” the late Vanguard founder John C. “Jack” Bogle said. “Neither too much nor too little.”1

In fact, our Vanguard Capital Markets Model® (VCMM), the rigorous and thoughtful forecasting framework that we’ve honed over the years, suggests that investors should prepare for a decade of returns below historical averages for both stocks and bonds.

We at Vanguard believe that the role of a forecast is to set reasonable expectations for uncertain outcomes upon which current decisions depend. In practical terms, the forecasts by Vanguard’s global economics and markets team inform our active managers’ allocations and the longer-term allocation decisions in our multiasset and advice offers. We hope they also help clients set their own reasonable expectations.

Being right more frequently than others is certainly a goal. But short of such a silver bullet, we believe that a good forecast objectively considers the broadest range of possible outcomes, clearly accounts for uncertainty, and complements a rigorous framework that allows for our views to be updated as facts bear out.

So how have our market forecasts fared, and what lessons do they offer?

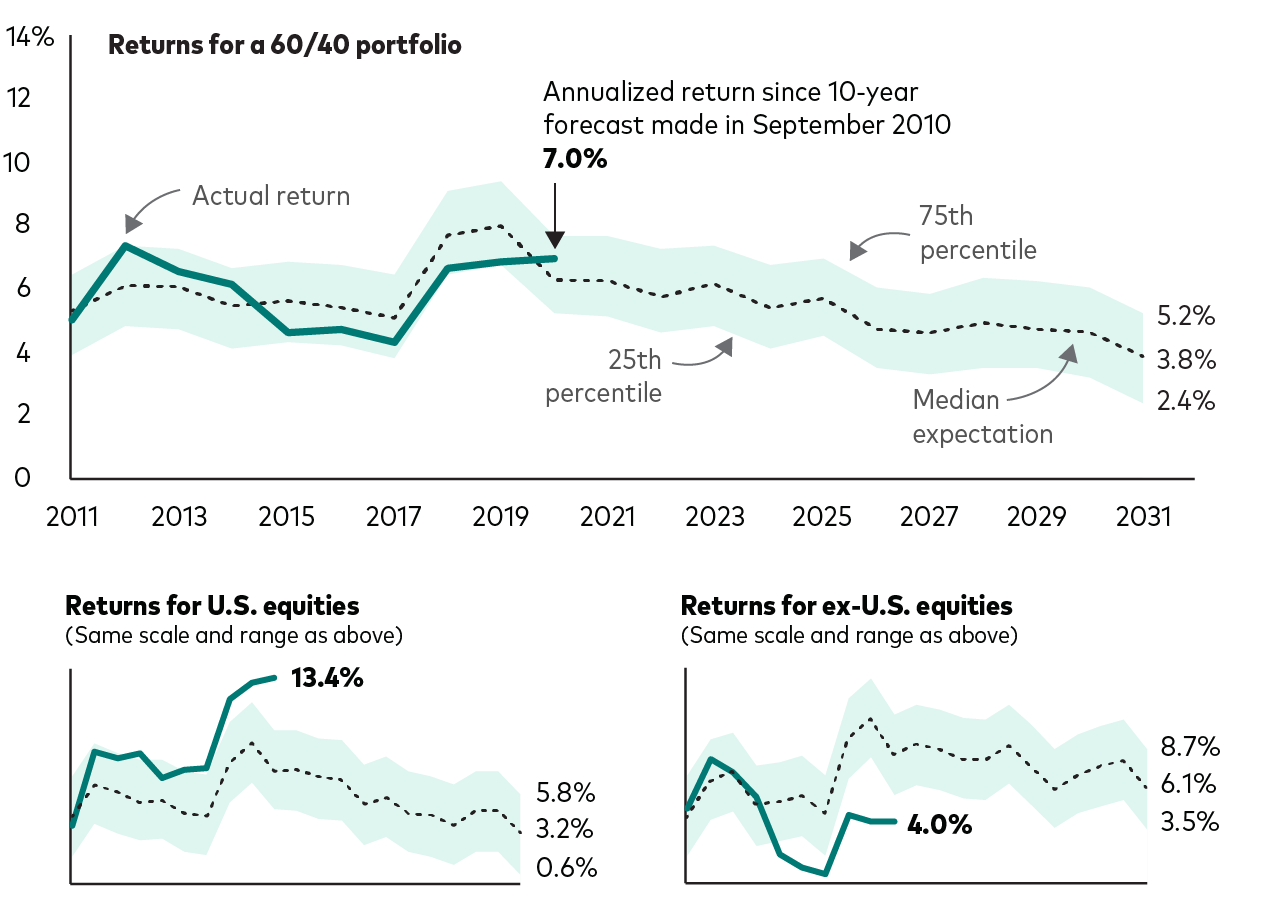

The illustration shows that 10-year annualized returns for a 60% stock/40% bond portfolio over the last decade largely fell within our set of expectations, as informed by the VCMM. Returns for U.S. equities surpassed our expectations, while returns for ex-U.S. equities were lower than we had expected.

The data reinforce our belief in balance and diversification, as discussed in Vanguard’s Principles for Investing Success. We believe that investors should hold a mix of stocks and bonds appropriate for their goals and should diversify these assets broadly, including globally.

You may notice that our long-run forecasts for a diversified 60/40 portfolio haven’t been constant over the last decade, nor have the 60/40 market returns. Both rose toward the end of the decade, or 10 years after markets reached their depths as the global financial crisis was unfolding. Our framework recognized that although economic and financial conditions were poor during the crisis, future returns could be stronger than average. In that sense, our forecasts were appropriate in putting aside the trying emotional strains of the period and focusing on what was reasonable to expect.

Our outlook then was one of cautious optimism, a forecast that proved fairly accurate. Today, financial conditions are quite loose—some might even say exuberant. Our framework forecasts softer returns based on today’s ultralow interest rates and elevated U.S. stock market valuations. That can have important implications for how much we save and what we expect to earn on our investments.

Valuation expansion has accounted for much of U.S. equities’ greater-than-expected returns over a decade characterized by low growth and low interest rates. That is, investors have been willing, especially in the last few years, to buy a future dollar of U.S. company earnings at higher prices than they’d pay for those of ex-U.S. companies.

Just as low valuations during the global financial crisis supported U.S. equities’ solid gains through the decade that followed, today’s high valuations suggest a far more difficult climb in the decade ahead. The big gains of recent years make similar gains tomorrow that much harder to come by unless fundamentals also change. U.S. companies will need to realize rich earnings in the years ahead for recent investor optimism to be similarly rewarded.

More likely, according to our VCMM forecast, stocks in companies outside the United States will strongly outpace U.S. equities—in the neighborhood of 3 percentage points a year—over the next decade.

We encourage investors to look beyond the median, to a broader set between the 25th and 75th percentiles of potential outcomes produced by our model. At the lower end of that scale, annualized U.S. equity returns would be minuscule compared with the lofty double-digit annual returns of recent years.

This brings me back to the value of forecasting: Our forecasts today tell us that investors shouldn’t expect the next decade to look like the last, and they’ll need to plan strategically to overcome a low-return environment. Knowing this, they may plan to save more, reduce expenses, delay goals (perhaps including retirement), and take on some active risk where appropriate.

And they may be wise to recall something else Jack Bogle said: “Through all history, investments have been subject to a sort of Law of Gravity: What goes up must go down, and, oddly enough, what goes down must go up.”2

1 Bogle, John C., 2015. Bogle on Mutual Funds: New Perspectives for the Intelligent Investor. Hoboken, N.J.: John Wiley & Sons, Inc.

2 Jenks, Philip, and Stephen Eckett, 2002. The Global-Investor Book of Investing Rules: Invaluable Advice from 150 Master Investors. Upper Saddle River, N.J.: Prentice Hall PTR.

I’d like to thank Ian Kresnak, CFA, for his invaluable contributions to this commentary.

Important information:

All investing is subject to risk, including the possible loss of the money you invest. Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income.

Past performance does not guarantee future results.

In a diversified portfolio, gains from some investments may help offset losses from others. However, diversification does not ensure a profit or protect against a loss.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk.

About the Vanguard Capital Markets Model:

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s Investment Strategy Group. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

"Tuning in to reasonable expectations", 5 out of 5 based on 38 ratings.