The Fed’s words are just that—not actions—and its words are squishy. Two other words many Fed observers love to cite as gospel: “data dependent.” As in, the Fed’s monetary policy will be “data dependent.”

Editorial Staff

Fisher Investments MarketMinder, 05/15/2019

In the press conference following early May’s Fed meeting, Fed head Jerome Powell said, “We suspect transitory factors may be at work,” regarding today’s low inflation. Pundits wasted little time seizing onto his “transitory” remark, extrapolating that meant we should no longer expect rate cuts. Accordingly, some think a pillar of the market’s 2019 rally just fell away, presuming stocks have done well because a rate cut appeared to be coming. But hold that thought. Rewind the tape six weeks earlier, when Powell described low inflation as “one of the major challenges of our time,” implying America risked turning Japanese. In our view, the problem for investors isn’t what the Fed thinks. Rather, it is that many take Fed statements as gospel. Whether the Fed characterizes low inflation as “transitory” or “persistent” doesn’t etch future monetary policy in stone.

Flawed Projections

The Fed’s words are just that—not actions—and its words are squishy. Two other words many Fed observers love to cite as gospel: “data dependent.” As in, the Fed’s monetary policy will be “data dependent.” When the “facts” (really their interpretation thereof) change, Fed members can change their minds, too. It all seems so science-y! Economists dispassionately viewing data and sizing up proper policy as a result. Hold on though. For all their supposed data dependence, they seem awfully prone to dismiss economic data that don’t conform to their forecasts, calling them “transitory.”

In June 2013, as the Fed considered tapering its quantitative easing (QE) program, the personal consumption expenditure (PCE) price index—the Fed’s targeted inflation gauge—was running about 1.5%,[i] below its 2% target. Fed staff claimed: “the recent softness in inflation would be transitory [and] projected that inflation would pick up in the second half.” [Boldface ours.] There is that word again! Now, if the Fed is so data dependent—and QE is actually inflationary (hint: it isn’t)—then they would leave policy unchanged, given sub-target inflation. They tapered in December, with inflation still below 2.0%. In September 2015, as the Fed jawboned about fed-funds target rate hikes, inflation fell to 0.1% y/y.[ii] Really low! Far below target. What to do? Again with the “transitory.” Lastly, for all this talk of transitory low inflation, may we point out they have achieved 2% y/y PCE or greater in only 14 of 86 months since setting an inflation target in January 2012?[iii]

Unreliable Narrators

These aren’t the only squishy Fedwords. What the Fed considers “neutral” or “accommodative” monetary policy also isn’t clear cut. In October, Chairman Powell said interest rates were a “long way from neutral”—rates that are neither stimulus nor inflation-fighting. The next month, they were “just below,” despite no change in policy rates. In December, after one rate hike, he said we had reached “the lower end of neutral.” His commentary around neutral seems pretty, ummmm, transitory. What changed? Possibly stocks’ correction, but it could be anything. What is to say he won’t reverse now?

The Fed members who set policy all have their own inconsistent definitions about its “appropriate stance”—and even their own definition can shift from meeting to meeting. Which they are pretty upfront about! As former Fed head Janet Yellen remarked at a 2016 Jackson Hole confab: “Our ability to predict how the federal funds rate will evolve over time is quite limited because monetary policy will need to respond to whatever disturbances may buffet the economy. In addition, the level of short-term interest rates consistent with the dual mandate varies over time in response to shifts in underlying economic conditions that are often evident only in hindsight.” This is essentially Fedspeak for: We are making it up as we go along as best as we can (so don’t hold us to it).

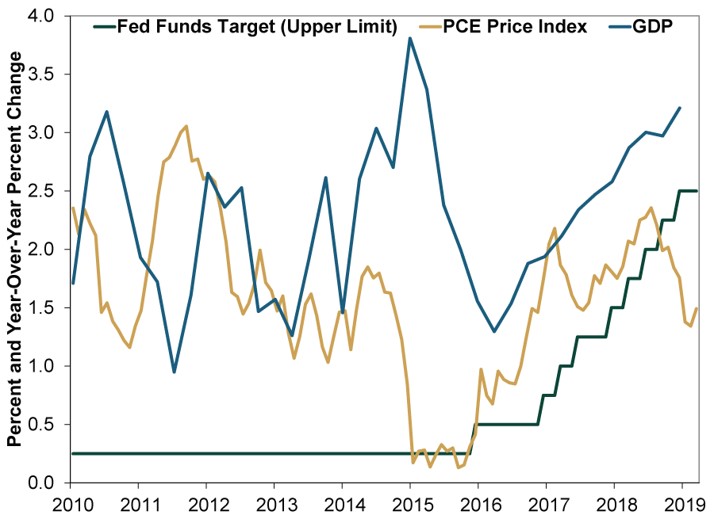

Overrated Influence

Then, too, even when they do act, their influence is usually overrated. The Fed’s dual mandate is to ensure price stability and foster maximum employment, but its ability to hit an inflation target or generate jobs is limited. As Exhibit 1 shows, years of near-zero policy rates and QE didn’t seem to buy them much. Inflation wandered between 0% and 3%, and GDP has chugged along, whether they floored rates and bought bonds or they didn’t. Economically speaking, there isn’t much to distinguish “accommodative” Fed policy from what it considers “neutral.” Monetary policy certainly has an influence on the economy and inflation. But don’t overrate it.

Exhibit 1: Not Much Economic Difference Between “Accommodative” and “Neutral” Fed

Source: Federal Reserve Bank of St. Louis, as of 5/8/2019. Fed funds target range - upper limit, percent, PCE price index, January 2010 – March 2019, and real GDP, Q1 2010 – Q1 2019.

Yes, the Fed controls short rates—and can monkey with long rates through long-term asset purchases. These can have important impacts on monetary policy, an economic input. But it is one input. One that doesn’t dictate all the cumulative decisions by households and businesses. We doubt many firms would hinge a major business expansion or hiring plan solely on what the Fed aims to do with interest rates. Many think high interest rates are an impediment to business investment, but if long-term funding costs at 4% versus 6% (roughly investment grade corporate bonds’ yield range since 2010) are what make or break a project, it probably wouldn’t have been worth pursuing in any event. Interest costs matter, but they are usually marginal, in our view.

We believe overrating whatever a Fed policymaker says is likely to prove an error—overthinking words that may not prove lasting to begin with. This isn’t to say a rate cut is or isn’t coming. We don’t know—and neither, in our view, does any other investor. Which is fine! We don’t think rate cuts are necessary to prolong this post-correction rally. Rallies like this are typically strong and usually doubted—part and parcel of what we have seen this year. Moreover, rate cuts, contrary to popular belief, aren’t bull fuel. It is conceivable one may perversely spook markets into thinking the Fed sees more trouble ahead than it previously acknowledged. (Not that Fedpeople possess such wonderful insight, but we digress.) So don’t fret the Fed’s words. This bull market isn’t nearly as transitory as central bankers’ squishy language.