1970s inflation to today

Consider some recent and less extreme currency inflations. The 1970s bear market in equities saw relatively mild inflation which was also characterized by relatively mild but nevertheless real factionalization of society. An ideological left vs right battle played out between labour and capital, unions and non-unions and perhaps most bizarrely, between rock and disco. As already stated, money implies a trust in the future. It implies that today.s money can be used in the future. So in the era of punk, did the Sex Pistols provide the most concise commentary of the malaise?

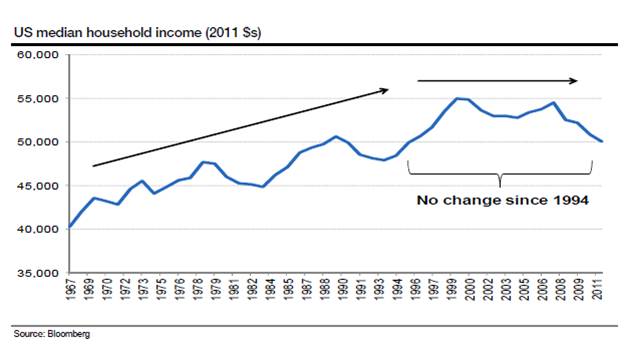

Which brings us to today. Despite the CPI inflation of the 1970s receding, our central banks have continued to play games with money. We.ve since lived through what might be the largest credit inflation in financial history, a credit hyperinflation. Where has it left us? Median US household incomes have been stagnant for the best part of twenty years (chart below).

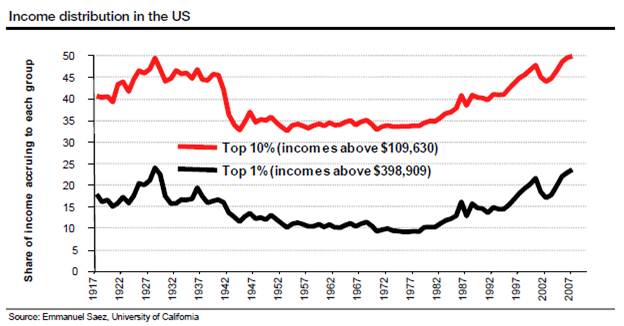

Yet inequality has surged. While a record number of Americans are on food stamps, the top 1% of income earners are taking a larger share of total income than since the peak of the 1920s credit inflation. Moreover, the growth in that share has coincided almost exactly with the more recent credit inflation.

These phenomena are inflation's hallmarks. In the Keynes quote above, he alludes to the "artificial and iniquitous redistribution of wealth" inflation imposes on society without being specific. What actually happens is that artificially created money redistributes wealth towards those closest to it, to the detriment of those furthest away.

Richard Cantillon (writing decades before Adam Smith) was the first to observe this effect (hence “Cantillon effect”). He showed how those closest to the money source benefited unfairly at the expense of others, by thinking through the effects in Spain and Portugal of the influx of gold from the new world as follows:

“If the increase of actual money comes from mines of gold or silver … the owner of these mines, the adventurers, the smelters, refiners, and all the other workers will increase their expenditures in proportion to their gains. . . . All this increase of expenditures in meat, wine, wool, etc. diminishes of necessity the share of the other inhabitants of the state who do not participate at first in the wealth of the mines in question. The altercations of the market, or the demand for meat, wine, wool, etc. being more intense than usual, will not fail to raise their prices … Those then who will suffer from this dearness … will be first of all the landowners, during the term of their leases, then their domestic servants and all the workmen or fixed wage-earners ... All these must diminish their expenditure in proportion to the new consumption …”

In other words, the beneficiaries of newly created money spend that money and bid up the price of goods with their higher demand. Those who suffer are those who have to pay newly higher prices but did not benefit from the newly created money.

The credit inflation analog to the Cantillon effect has played out perfectly in recent decades. Central banks provided cheap money to banks, the cheap money artificially inflated asset prices, artificially inflated asset prices made anyone connected to those assets rich as we became a nation of speculators, those riches were achieved at everyone else’s expense, and ‘everyone else’ has now realized what has happened and is understandable enraged … as Keynes explained, “Those to whom the system brings windfalls …. are the object of the hatred.

And now the social debasement is clear for all to see. The 99% blame the 1%, the 1% blame the 47%, the private sector blames the public sector, the public sector returns the sentiment … the young blame the old, everyone blame the rich … yet few question the ideas behind government or central banks ...

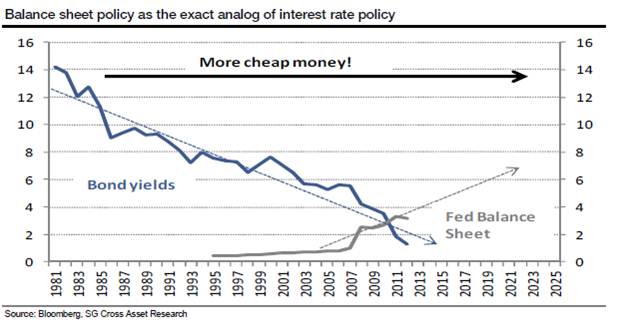

I'd feel a whole lot better if central banks stopped playing games with money. But I can't see that happening anytime soon. The ECB has thrown the towel in, following the SNB last year in committing effectively to print unlimited amounts of money for the greater good. The BoE and the Fed have long since made a virtue of what was once considered a necessity, with what was once the unconventional conventional. As James Bullard told everyone a few weeks before the last Fed meeting, lest there be any doubt:

"Markets have this idea that, there's QE1 and QE2, so QE3 must be the same as those previous ones. It's not that clear to me that this is the way this is going … it would just be to do balance sheet policy as the exact analogue of interest rate policy."

In other words, the central banks. balance sheets are the new policy tool. As interest rates embarked on a multi-year decline from the 1980s on, central bank balance sheets are set to embark on a multi-year climb ...

So as Nobel Prize winning experts in economics punch the air because inflation expectations have been rising since the policy was announced, “It’s the whole point of the exercise” (Duh!) the BoE admits that QE has mainly benefited the rich, but vows to continue anyway.

All I see is more of the same - more money debasement, more unintended consequences and more social disorder. Since I worry that it will be Great Disorder, I remain very bullish on safe havens. The next few issues of Popular Delusions will outline some thoughts on what exactly that means.