Stocks already showed they don’t need rate cuts.

2021 and 2022 were among the worst years for fixed-income investors in developed markets in world history.

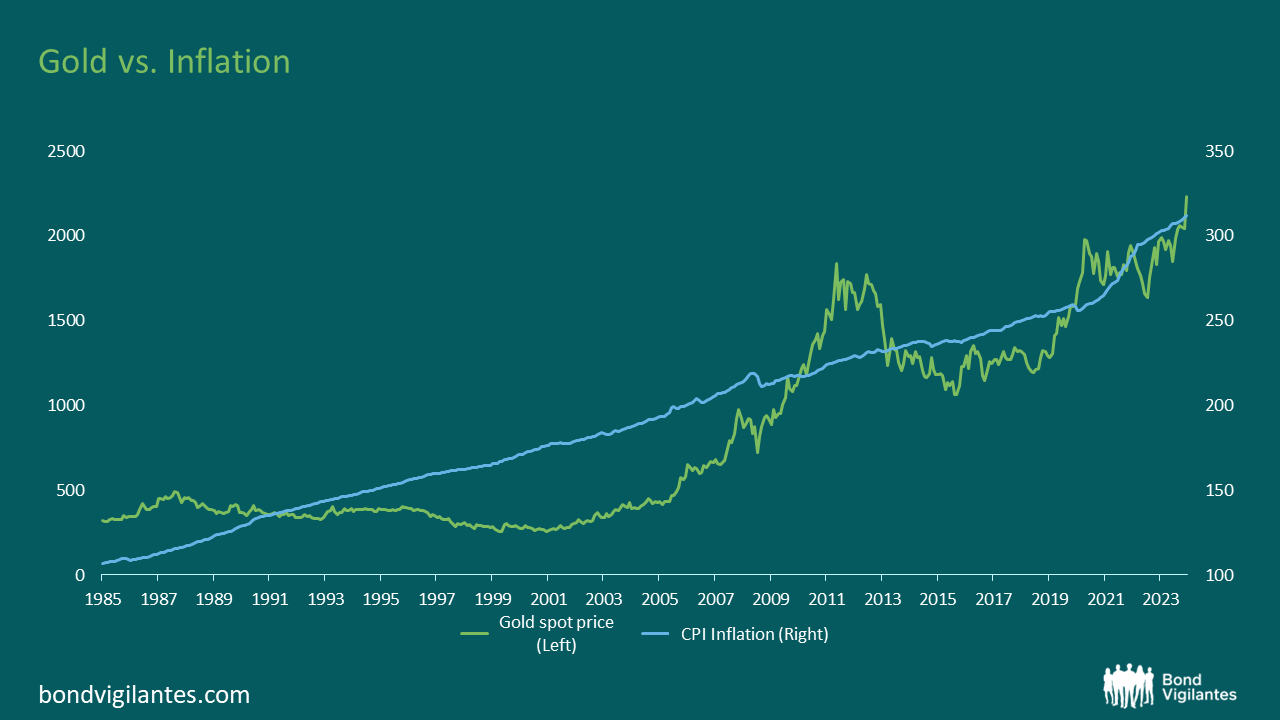

Renowned for its role as a hedge against economic uncertainty and inflation, gold has long captivated investors. One key factor influencing gold’s price is the relationship between real yields and inflation. Over the long term, gold has protected one against the pernicious effects of inflation and remains a powerful diversifier within an investment portfolio:

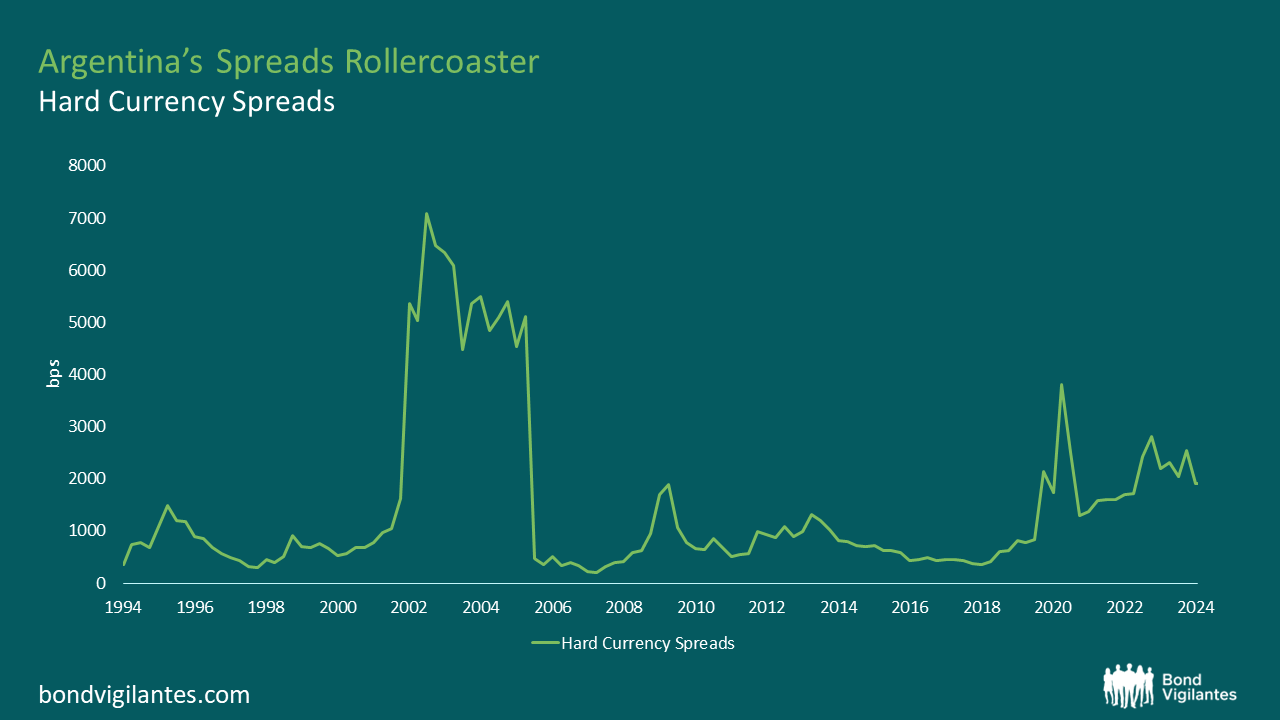

Javier Milei, Argentina’s newly elected president, shares similarities with Roosevelt in that he has inherited, to put it mildly, a struggling economy, and has begun attempting to implement reforms in very quick order.

Reasonable valuations could provide an upside surprise

For institutional investors only

Some people think of the glass as half full, some people think of the glass as half empty, I think of the glass as too big!"

Everyone has a plan until they get punched in the face."

Do you consider yourself a disciplined guy, do you get up every day and work?"

Oh, I try to get up every day!“