What do COVID lockdowns, currency collapses, and hyperinflation all have in common? According to Steve Hanke, they all reveal how central planners manipulate fear, money, and power to control society.

How Textiles Made the World

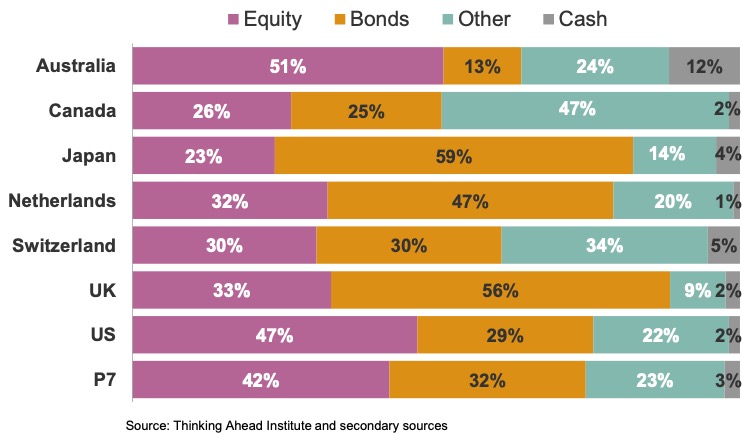

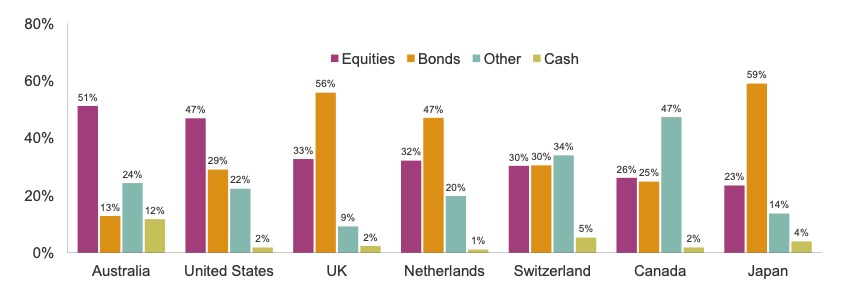

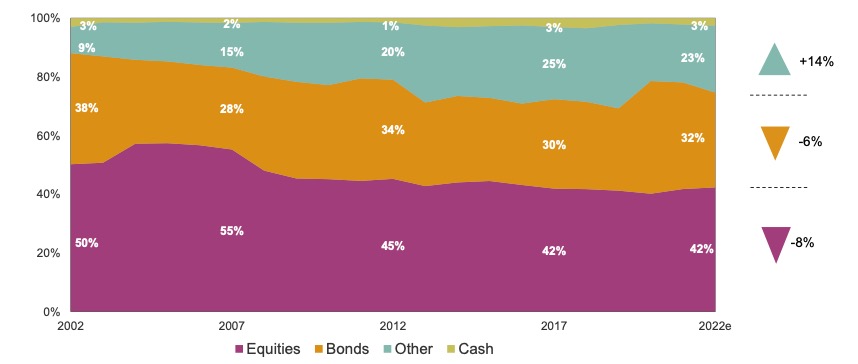

For institutional investors only

"You know what kills most ideas, I think, is people desperate to express an opinion."

"I was born in Beijing, My given name is Puyi, together with my original Manchurian surname, my full name is Aisin-Gioro Puyi. I was Emperor of China in 1909."

“Er träumte von einer Klarinette, die sich selbst spielte.“