"I see striking parallels between the dramatic recent sell-off in U.S. Treasuries and the Great Bond Crash of 1994. To make matters worse, today’s bond market is even more sensitive to fears about tightening thanks to the U.S. Federal Reserve’s unprecedented expansionary program since the 2008 crisis."

Scott Minerd

Guggenheim Investments, July 2013

At the start of June, I waxed nostalgic about the canary in the coal mine. In the aftermath of a string of downside moves in financial markets, I wrote about how early mines lacked ventilation and so miners brought caged canaries into new seams to detect deadly gasses. The story went that if the canary stopped singing, or even worse, died, the mine would be evacuated until the gas buildup could be cleared to make work safe again. My point was that markets were foreshadowing worse trouble ahead. Now, I regret to tell you, my prognosis was all too accurate. The canary is certainly dead. And, in the sudden market rout that has marked the beginning of the summer season, the chirpy yellow bird was far from the only casualty.

I see striking parallels between the dramatic recent sell-off in U.S. Treasuries and the Great Bond Crash of 1994. To make matters worse, today’s bond market is even more sensitive to fears about tightening thanks to the U.S. Federal Reserve’s unprecedented expansionary program since the 2008 crisis.

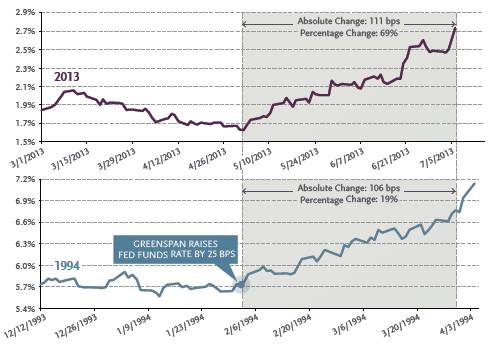

At the start of 1994, Bill Clinton signed the North American Free Trade Agreement into law, Alan Greenspan was at the helm of the U.S. Federal Reserve, and markets were optimistic. I was working in London, running European credit trading for Morgan Stanley. Our desk turned over about $500 million in credit daily. Bond yields were historically low, inflation was muted. Then, after a calm start to the year and almost without warning, bond markets suffered their largest crash since the Great Depression.

The trouble began in February when Fed Chairman Greenspan, after almost five years of monetary expansion, announced a seemingly innocuous 25 basis point increase in the federal funds rate. Bond markets reacted swiftly and violently, re-pricing securities based on where investors anticipated interest rates would be at the end of what markets

correctly assumed was a tightening cycle. Liquidity significantly dried up, and over the next nine months, the 10-year yield rose 240 basis points. We were on the front lines of the crisis – during those dark days, our daily volume on the trading desk shriveled from $500 million to just $15 million.

In 1994, investors were caught off guard because the duration of their positions – a great deal of which were mortgage-backed securities – was lengthened beyond their targets due to rising interest rates. Those investors used Treasuries as a means to sell duration because they were their most liquid assets. Credit spreads soon exploded as dealers lacked the ability to take on larger positions from would-be sellers. Both sides of the Street were sprinting in one direction, leading to a violent stampede for the only exit.

It appears we are witnessing a similar cascade today. The sell-off began at the start of May, as U.S. economic data suggested housing could spark a stronger economy. It continued after May 22, when Fed Chairman Ben Bernanke told lawmakers that the central bank would, in the coming months, discuss how it might approach tapering its asset purchases. Then on June 19, the other shoe dropped when Dr. Bernanke held his post-Federal Open Market Committee meeting press conference. Despite his insistence that tightening is not imminent, his guidance amounted to an outline and a timetable of how quantitative easing (QE) will be tapered, and eventually ended. Markets were

caught off guard by how quickly the Fed could take away the proverbial punch bowl.

Both Greenspan and Bernanke pushed the boundaries of Fed transparency, but the way they telegraphed their messages seems to have contributed to market volatility. Greenspan’s rate increase in February of 1994 marked the first time the FOMC released a statement announcing a move in the federal funds rate, its main policy tool. And Bernanke is the first Fed chairman to hold post-FOMC press conferences, a practice he began in April, 2011. The message contained in Bernanke’s June 19 post-FOMC press conference certainly triggered the market rout that would follow.

1994 Once More

Demand for U.S. Treasuries is contracting, while supply has drastically increased due to hedging and account liquidation. As a result, we have seen adverse moves on both sides of the market, causing a sharp decline

Source: Bloomberg, Guggenheim Investments. Data as of 7/5/2013.

Part of the recent correction in the bond market is the result of the readjustment of the term structure of interest rates, but most of it is due to concerned investors seeking to reduce their portfolio exposure by shedding duration, often by shorting Treasuries. Many of these investors have recently been engaged in a leveraged carry trade, meaning higher interest rates magnified the downside losses and, in the case of mortgage securities, the effect on prices was even more amplified as durations extended as a result of reduced expectations of repayment. This leveraged effect on mortgage portfolio losses explains the dramatic decline in mortgage REITs over the past weeks. While in the very near term things could improve, the situation could worsen because the rising interest rate trend looks set to continue, with a medium-term target of 3.25-3.5 percent for the 10-year note. The eventual follow-on to this will likely be a widening of credit spreads.

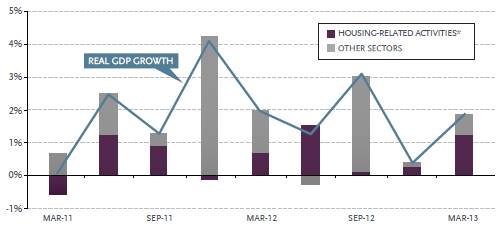

Rising rates will continue to reduce housing affordability, which is especially troublesome because housing is the primary locomotive of U.S. economic growth. Housing activity has been driven by artificially low mortgage rates. Housing-related activity, including private residential investment, personal expenditures on household durable goods and utilities, as well as the wealth effect on consumption from home price appreciation, has positively contributed to GDP growth for the last five quarters.

Housing activity was the sole positive contributor to economic growth in the second quarter of 2012, and it comprised over two thirds of real GDP growth in the first quarter of 2013. First quarter real GDP growth was only 1.8 percent, 69 percent of which was directly attributable to housing. Rising interest rates caused mortgage applications to fall sharply in May, and profits from new construction also faltered. The housing refinancing index has also come under pressure.

One Pillar Economy

Housing’s vast contribution to economic output is dependent upon the maintenance of extremely low mortgage rates, which have recently been moving higher.

Source: Haver Analytics, Guggenheim Investments’ estimates. Data as of 1Q2013. *Note: Housing-related activities are defined as private residential investment, personal expenditures on household durable goods and utilities, and the wealth-effect on consumption from home price appreciation. For simplicity, we don’t consider the impact of the housing boom on job creation, which could potentially add additional growth to housing-related activities.

The Fed’s assumptions now include a forecast that unemployment will drop to 7.2- 7.3 percent by year end. That suggests that the Fed believes economic activity will accelerate as we head into the summer. I do not subscribe to this view, since we are already seeing pressure on housing and the broader economy from higher interest rates, and the negative impact of the recent spike in yields is likely to continue to show up in the economic data over the summer. That means the Fed, despite Dr. Bernanke’s recently announced timetable, may be forced to expand or extend QE if the housing market’s response to recent events becomes more acute and starts to negatively affect the job market recovery. Consequently, it is fairly certain that QE will continue at its current rate through the end of 2013, and the Fed will likely still be carrying out asset purchases well into the second half of 2014. This view is supported by the low near-term risk of inflation.

Meanwhile Fed officials are struggling to put the toothpaste back in the tube. In the wake of Bernanke’s press conference, numerous Federal Reserve presidents have attempted to clarify or even refine the message. San Francisco Fed President John Williams, who in May said the central bank could begin tapering its asset purchases by the summer and finish them by year-end, backtracked in recent days. The centrist policymaker now says it’s too early to say when the Fed will taper and that the central bank must be certain the recovery can withstand ongoing fiscal contraction.

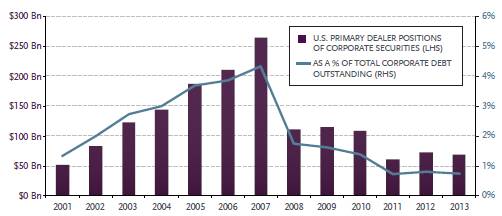

Another important consideration in the recent market dislocation is the value of primary dealer positions relative to the bond market’s total size. Ultra-low interest rates since 2008 spurred increased debt issuance while dealer positions in commercial paper, investment grade, and high-yield corporate bonds have declined from their peak of about $260 billion in 2007 to $69 billion today due to banking regulations. This means bond market dealer balance sheet coverage has shriveled from 4 percent of total inventory in 2007 to less than 0.7 percent of today’s $9 trillion market.

There will likely be further selling pressure when mutual funds post quarterly statements featuring losses, and as the carnage from the bond market shows up on 401k statements. These investors will not care that the risk of a recession is highly remote but will focus instead on signals from the Fed that interest rates will rise.

Rough Sledding Ahead

The lack of a cushion from Wall Street in the U.S. Treasury market increases liquidity risk because investors will lack the means to cut their positions as rates move up, pushing bond yields higher.

Source: Federal Reserve Bank of New York, Bloomberg, SIFMA, Guggenheim Investments. *Note: Corporate securities include commercial paper, investment grade, and high-yield corporate bonds. Data for 2013 as of 1Q2013.

The New York Stock Exchange Advance Decline line is also forecasting tough times ahead. Over the long-term, equities prices will likely reflect the recovery in the underlying economy, but a stock market fall of 10-20 percent is still likely given how volatile markets have become. Uncertainty will remain elevated through the summer because we will not be able to gauge the impact higher interest rates are having on the economy until we get data in August that reflects housing activity from months earlier.

Fixed-income investors should be particularly cognizant of liquidity levels, keeping maturities short and spread duration low. High-yield spreads may widen by another 100 basis points because of the recent Treasury crash and gold may ultimately regain its safe-haven status.

Markets are certainly under pressure, but this is not a doomsday scenario. This liquidity flush will continue to unfold, and things will likely get worse before they get better. Investors face a rough summer, but it is important to remember that even the extreme bear bond market that began in February 1994 ended before the end of that year.

This year, Treasuries began selling off in April, so if this swoon behaves like the 1994 bear market for bonds, we can expect to be out the other end by the end of the year. Certainly, I don’t think we will see any relief for lower bond prices until economic data begins to reflect a slowdown in both housing activity and price appreciation.

History, Mark Twain wrote, does not repeat itself, but it does rhyme. The Great Bond Crash of 1994 did not push the economy into recession, and it does not appear that will occur now either. There will continue to be strain on the financial system, but default levels will stay low. Investors who heeded this year’s earlier tough market conditions as a signal to take a more conservative stance are well prepared for the recent policyinduced volatility. Investors, who evacuated the mine immediately after the canary died, are now in a favorable position to seize opportunities that have and will result from the unfolding market turmoil.