When the Fed kept quantitative easing (QE) in place last week, US investors weren’t the only ones (wrongly) breathing a sigh of relief. Taper terror is fully global!

By Elisabeth Dellinger

Fisher Investments, MarketMinder, November 8th 2013

When the Fed kept quantitative easing (QE) in place last week, US investors weren’t the only ones (wrongly) breathing a sigh of relief. Taper terror is fully global!

In Emerging Markets (EM), many believe QE tapering will cause foreign capital to retreat. Some EM currencies took it on the chin as taper talk swirled over the summer, and many believe this is evidence of their vulnerability—with India the prime example as its rupee fell over 20% against the dollar at one point. Yet while taper jitters perhaps contributed to the volatility, evidence suggests India’s troubles are tied more to long-running structural issues and seemingly erratic monetary policy—and suggests EM taper fears are as false as their US counterparts.

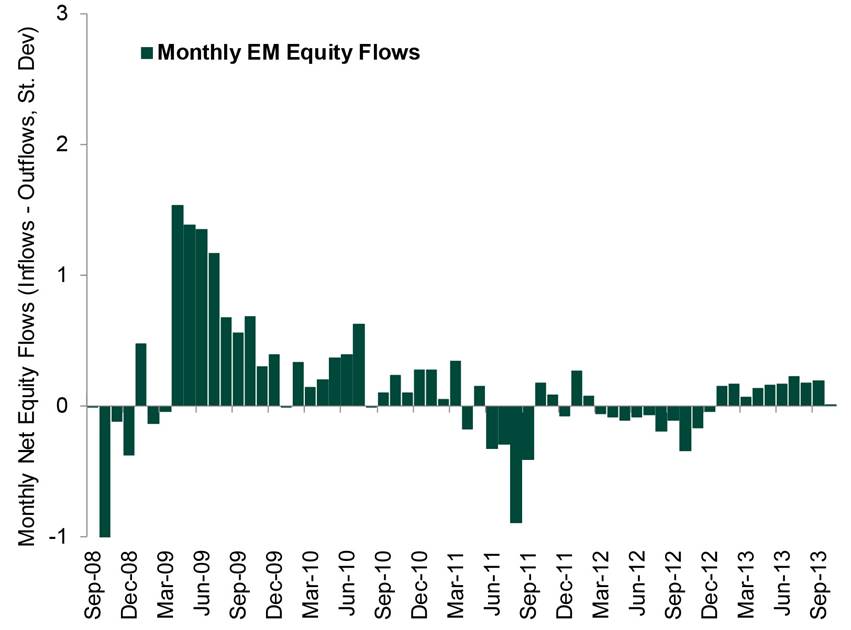

The claim QE is propping up asset prices implies there is some sort of overinflated disconnect between Emerging Markets assets and fundamentals—a mini-bubble. Yet this is far removed from reality—not what you’d expect if QE were a significant positive driver. Additionally, the thesis assumes money from rounds two, three and infinity of QE has flooded into the developing world—and flows more with each round of monthly Fed bond purchases. As Exhibit 1 shows, however, foreign EM equity inflows were strongest in 2009 as investors reversed their 2008 panic-driven retreat. Flows eased off during 2010 and have been rather weak—and often negative—since 2011.

Source: State Street Global Markets Research, as of 10/18/2013.Source: State Street Global Markets Research, as of 10/18/2013.

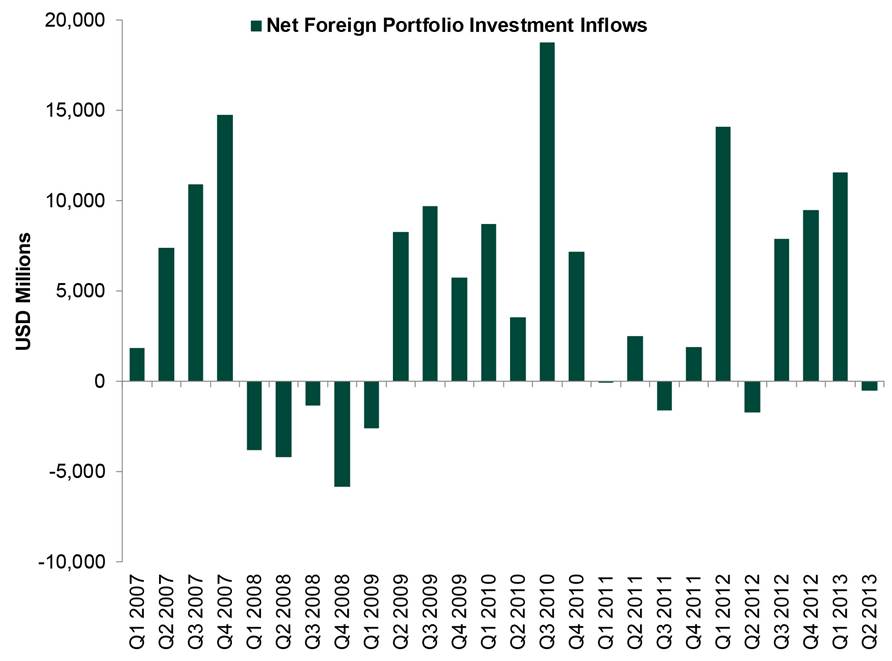

This also holds for India. Much like broader Emerging Markets, Indian equity markets show no signs of euphoric disconnect from reality—there is no evidence of a bubble. Foreign portfolio investment inflows, too, show no signs of abnormality. As shown in Exhibit 2, inbound investment since QE began isn’t out of line with pre-2008 flows.

Exhibit 2: Indian Net Foreign Portfolio Investment Inflows

Source: Reserve Bank of India, as of 10/17/2013.Source: Reserve Bank of India, as of 10/17/2013.

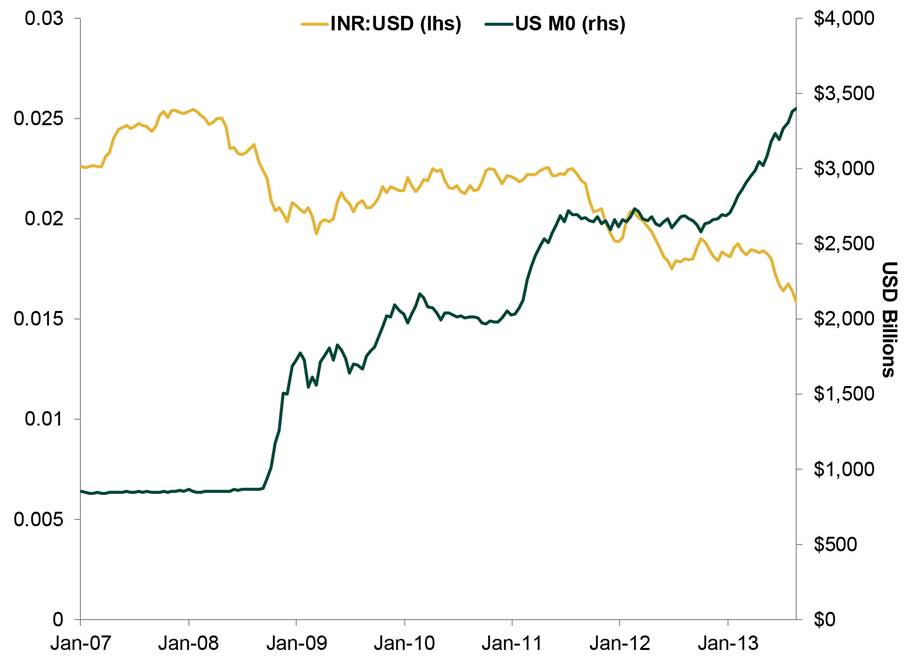

Similarly, there doesn’t appear to be a discernible relationship between the rupee and QE. Exhibit 3 plots the INR:USD exchange rate and the difference between the US M0 money supply. While the rupee did strengthen early on, it began weakening in summer 2011—long before taper talk began.

Source: FactSet Data Systems, Inc. and Federal Reserve Bank of St. Louis, as of 8/21/2013.

This all strongly indicates QE taper talk is miscast as the fundamental cause of the rupee’s summer fall. While taper-related sentiment may have a role—currency markets, like equity markets, can swing on sentiment and are vulnerable to false fears—structural issues and monetary policy errors appear to be a more significant driver.

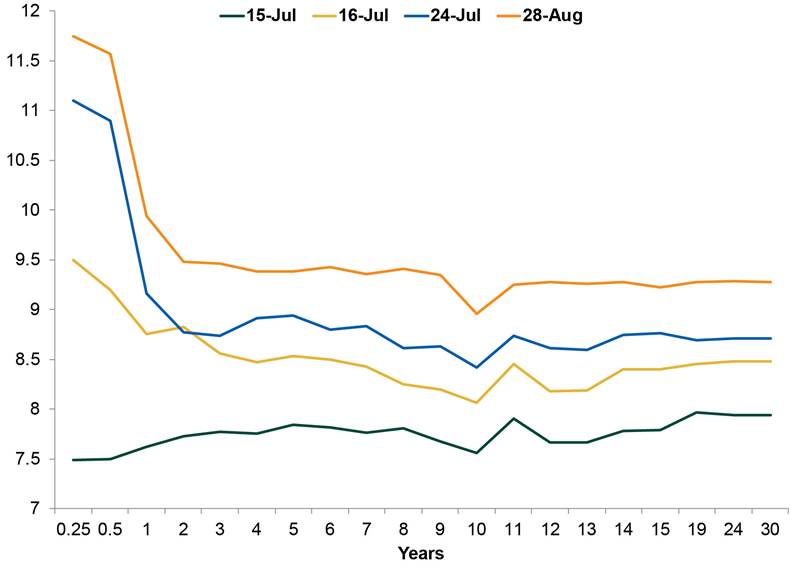

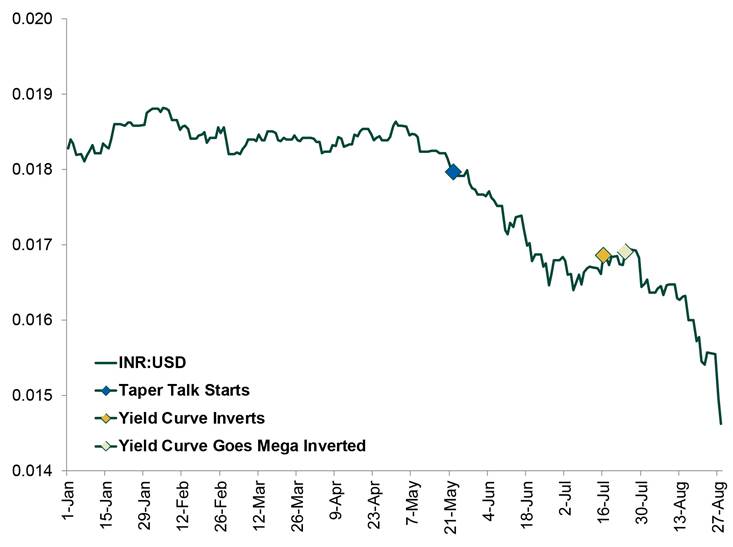

Whether coincidentally or not, the rupee’s decline began May 2—the day after the main opposition party announced it would cease cooperating with the government on planned legislation, casting doubt on further economic reforms (a key driver of investor confidence in India). This was 20 days before taper talk began with Fed Chair Ben Bernanke’s May 22 Congressional testimony. The rupee weakened through mid-June, then appeared to stabilize—until July 16, when the Reserve Bank of India (under the stewardship of former Governor Duvvuri Subbarao, who was succeeded by Raghuram Rajan on September 5) intervened. In an effort to shore up the currency, policymakers hiked the bank rate by two percentage points, inverting the yield curve. At that time, the spread between short and long rates was -1.015 percentage points. Eight days later, it had widened to -2.39 (Exhibit 4). The rupee’s freefall began shortly thereafter (Exhibit 5).

Source: Investing.com, as of 8/28/2013.

Exhibit 5: INR:USD Exchange Rate (2013)

Source: FACTSET Data Systems, Investing.com, as of 8/28/2013.

Measures taken over the ensuing weeks compounded the problem. New tariffs on flat-screen TV imports, higher levies on gold imports and “emergency” capital controls were largely perceived as ineffective stopgaps. As was the RBI’s August 23 decision to embark on its own small QE program. To inject liquidity into capital-starved banks, on August 23 the RBI launched a small open-ended quantitative easing program, further inverting the curve.

This series of events also appears tied to Indian equity markets’ Q3 correction. Inverted yield curves discourage economic activity. Central banks globally agree with this, so that a bank would deliberately invert the yield curve—then compound matters with measures that widen the negative spread—is perplexing and likely to create uncertainty for investors.

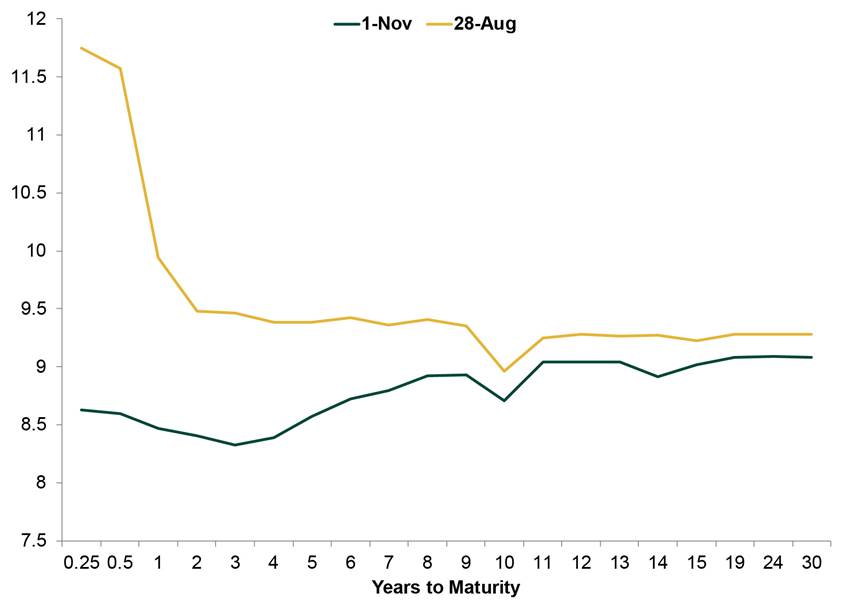

Since then, the pressure on the rupee has eased, and monetary policy appears to have stabilized. The three-month yield has fallen from 11.18% on August 30 to 8.63% on November 1, while the 10-year has risen from 8.602% to 8.705%. The yield curve still looks a bit wonky, but the long end is now positively sloped overall. (Exhibit 6) Indian stocks, too, have rebounded.

Exhibit 6: Indian Yield Curve as of 11/1/2013

Source: Investing.com, as of 11/1/2013.

Moreover, Emerging Markets—India included—look poised to reaccelerate when QE ends. QE has had an impact on the developing world that few appreciate. Long-term rates in the advanced and Emerging Markets are highly correlated. Yield curves have flattened in the developing world in sympathy with the US yield curve during successive rounds of QE. The US yield curve has already steepened in anticipation of QE’s end, and global curves have followed—Mexico, Thailand and Korea are three examples. This should aid loan growth globally, increasing the broad money supply—a powerful economic tailwind. With most investors broadly expecting the opposite, continued—even reaccelerating—growth should be a powerful positive surprise.