"Just when you thought things were improving"

"Just when you thought things were improving"

The war in Ukraine could dampen the pace of the recovery in the eurozone, while inflation is likely to be close to 4% for the year. The European Central Bank will have more trouble navigating through the storm, though we still expect an end to quantitative easing in the third quarter and a first rate hike towards the end of the year

Just when everyone was hoping that the negative impact of the pandemic was nearing its end, the eurozone has been hit by another potentially “stagflationary” shock. While Russia and Ukraine are definitely not the biggest export destinations for the eurozone, a double-digit decline in exports to the region might still shave one or two-tenths of a percentage point off eurozone growth this year. Also, some negative confidence effects and of course a bigger headwind from even higher energy prices have to be taken into account. On top of that, it looks as if the war in Ukraine and the sanctions against Russia will worsen supply chain problems with an additional negative impact on growth.

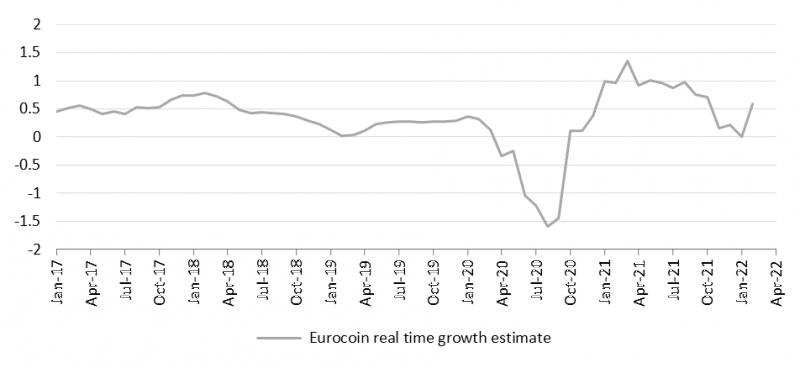

With the future of the conflict very uncertain, forecasts are by definition preliminary. Taking into account a scenario that over the course of the things will stabilise, with sanctions remaining in place, we think that it is too early to already pencil in a recession. As a matter of fact, growth momentum started to pick up again in February with the withdrawal of most Covid-19 confinement measures. Both the Purchasing Managers' Index (PMI) and the European Commission’s sentiment indicator rose more than expected in February on the back of stronger confidence in the services sector.

Even though the Bundesbank, Germany's central bank, was still fearing negative growth in the first quarter because of a high level of Omicron-induced absences in January, the Ifo Institute for Economic Research indicator increased in February for the second month in a row. However, all these surveys were done before the war in Ukraine erupted and can therefore not be extrapolated.

Growth has started to pick up again

Source: Refinitiv Datastream

Looking at the different negative impacts of the war, energy is clearly the Achilles’ heel of the eurozone. Based on gas and oil price forwards in December 2021, the European Central Bank (ECB) estimated a negative GDP growth impact of 0.2 percentage points in 2022. However, future prices have climbed higher since then, meaning that the negative impact could be slightly bigger. While it is still early days, there has already been talk of production problems because of supply disruptions from Ukraine or Russia. As such, Volkswagen had to halt production in two electric car factories in Germany because of a lack of deliveries of components. Air transport will also be hampered by blockages of key east-west flight corridors.

According to a Reuters report, the ECB quantified the negative impact of the conflict on eurozone GDP in an initial assessment at 0.3% to 0.4%, with a severe scenario seeing GDP reduced by close to 1%. For the time being, we decided to go somewhere in between with a 0.7 percentage point growth reduction, downgrading our growth forecast to 3% for 2022 and 2.3% for 2023. While the 3% might still seem high, you should take into account that the carry-over effect from 2021 is already close to two percentage points. That said, we agree that the risk to our forecasts is still skewed to the downside.

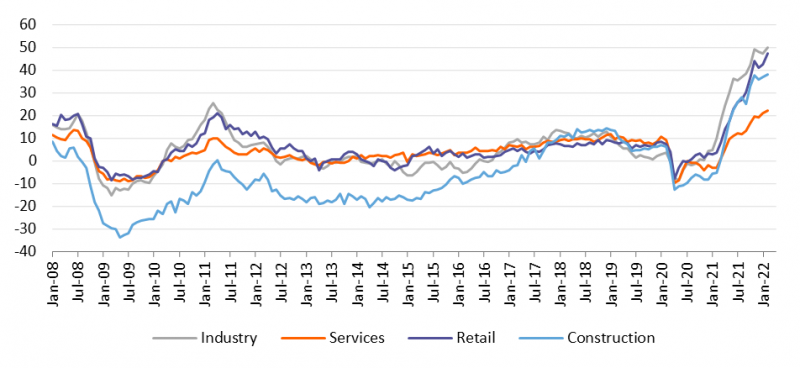

At the same time, the risk to inflation remains skewed to the upside, especially if energy prices continue to hover around current levels. The flash estimate for the Harmonised Index of Consumer Prices (HICP) inflation in February came out at 5.8%, significantly higher than expected. Core inflation rose to 2.7%. In the European Commission’s survey, selling price expectations for the next three months were the highest on record in industry, services and retail trade, while in construction they are at the highest level since 1990. This suggests that inflationary pressures are clearly broadening. We now believe that headline inflation will remain firmly above 2% for the whole of 2022, closing the year at 2.5%. On average we expect 3.8% for 2022, but not much has to happen to see a 4 before the dot.

Price expectations are going through the roof

Source: Refinitiv Datastream

Downward pressure on growth and upward pressure on inflation hasn’t made the ECB’s life any easier. Those who pleaded for an early rate hike have backtracked in the wake of the war in Ukraine, though the inflation overshoot remains worrying. The consensus seems to be building within the Governing Council for an end to quantitative easing (QE) in 3Q and a first rate hike in the fourth quarter, exactly our scenario.

Content Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.