While concerns around credit market liquidity have been rising since the global financial crisis, the COVID-19 sell-off has highlighted how fragile liquidity can be during periods of real stress.

While concerns around credit market liquidity have been rising since the global financial crisis, the COVID-19 sell-off has highlighted how fragile liquidity can be during periods of real stress.

While concerns around credit market liquidity have been rising since the global financial crisis, the COVID-19 sell-off has highlighted how fragile liquidity can be during periods of real stress. Colin Purdie discusses the short- and long-term implications for investment grade and high yield credit globally.

After entering 2020 on the back of a multi-year bull run, most credit investors would have been relatively comfortable about the short-term prospects for both investment-grade and high-yield bonds. With benign economic conditions and the continuation of accommodative monetary policy by major central banks, there was little to suggest a storm was on the horizon. The COVID-19 pandemic, and the knock-on disruption it is causing to economies and businesses, has changed everything – triggering a sell-off in credit assets that has been exacerbated by a structural lack of liquidity that many investors have had concerns about since the global financial crisis.

The dislocation in global credit markets in March was driven by several factors. Already aware of the lateness of the cycle, investors quickly became concerned about the economic impact of COVID-19 on companies’ leverage, free cash flow, and ability to pay down debt, particularly for companies where leverage was already high. This put significant upward pressure on credit spreads as investors scrambled to reduce risk. The credit market was also hit with record redemptions as investor sentiment soured,1 while non-traditional investors were trying to take short positions in certain segments of the credit markets – not unlike during the global financial crisis. As a result, too many investors were trying to sell at the same time, and there was insufficient capacity to allow this to happen in an orderly fashion.

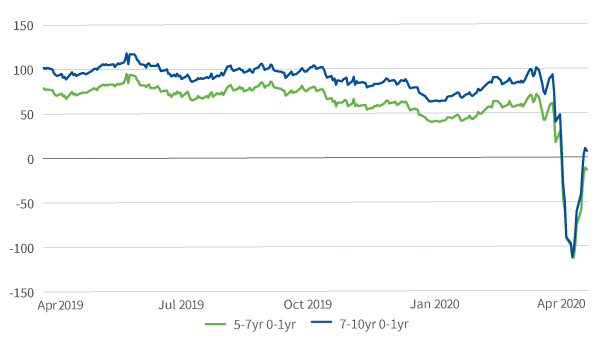

Liquidity inevitably dried up, but we have also seen irrational behaviour. In a sell-off we would typically expect assets to be sold across the credit curve and quality spectrum; in this case, investors sold what they could rather than what they wanted to. The front end of the US investment-grade curve underperformed dramatically, as investors stood to suffer less (a few basis points) by selling shorter-maturity bonds (Figure 1). This in turn caused further panic and selling, compounded by the lack of liquidity in the market.

Figure 1: US investment grade curve

Note: IG indices = H540, C340, C4A0. HY indices = J1A0, J2A0, J3A0, J4A0. Source: Aviva Investors, Bloomberg, ICE BofAML, as of April 3, 2020

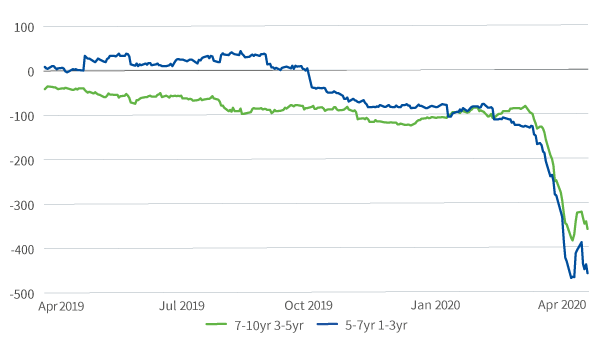

Figure 2: US high yield curve

Note: IG indices = H540, C340, C4A0. HY indices = J1A0, J2A0, J3A0, J4A0. Source: Aviva Investors, Bloomberg, ICE BofAML, as of April 3, 2020

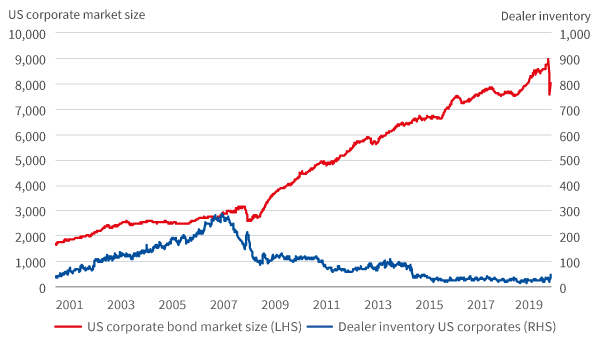

As post-financial crisis regulation limited the ability of investment banks to play their traditional role of market makers, in other words to warehouse risk, credit markets were undergoing a period of exponential growth thanks to easy access to capital and companies’ willingness to increase leverage (Figure 3). Unsurprisingly, this structural decline of liquidity – stemming from dealers’ smaller balance sheets and even more by the huge increase in market size – was a key contributor to the size of the moves in March.

Figure 3: US credit market size vs. dealer inventory

Source: Bloomberg, ICE-BofA, Federal Reserve, Aviva Investors, as of April 8, 2020

In this unprecedented situation, every day continues to bring new insight into how the market, consumers and companies are being impacted. Both from a regulatory and a portfolio management standpoint, the uncertainty caused by COVID-19 has led investors to spend most of their time focusing on cash management, although – on a selective basis – some investment opportunities have been created.

In response to the crisis, major central banks quickly announced the resumption of asset purchasing programmes, which are supportive of credit, complemented by measures such as backstops that encourage banks to play their role of intermediaries.2 Such support is welcome at this time, but in some ways is a double-edged sword.

On the one hand, market participants’ reliance on central banks to consistently intervene during difficult periods for economies and markets may have contributed to corporate behaviours that have driven up financial leverage in the system. It also allowed investors to ignore this build-up of leverage, safe in the knowledge central banks will come to the rescue.

On the other hand, central bank and fiscal support from governments can have a great psychological impact to the benefit of markets – investors often only want reassurance in times of stress. To see this, look no further than the corporate bond-buying programme announced by the US Federal Reserve (Fed) on March 23.3 The US credit market was failing, and the Fed’s strong, well-articulated response put it back on track. Before central banks had even spent a penny on the programmes, the rally and the levels of issuance in the primary market were testament to the psychological benefits of these announcements.

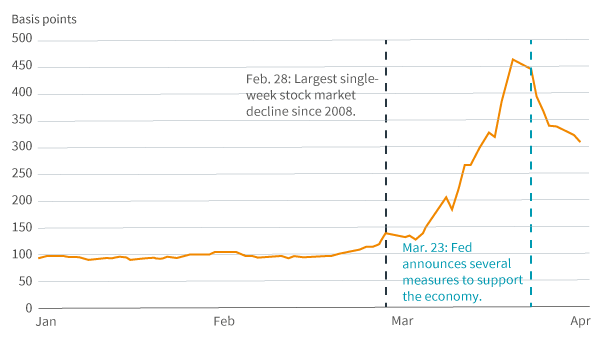

In fact, March was a record month in terms of issuance across credit. US investment-grade bond supply exceeded $260 billion, with $110 billion in the last week of March.4 The return to some semblance of normality and stability in that week seemed to open the floodgates. The pace and magnitude of new issuance were surprising, but even more surprising was that demand outstripped supply and spreads continued to rally (Figure 4).

Figure 4: Corporate bond credit spreads

Source: Federal Reserve Bank of St Louis, TRACE (FINRA), Mergent FISD, as of April 9, 2020

While this may seem paradoxical given the uncertainty over the duration of this crisis and its ultimate economic impact, it is possible the initial sell-off may have been too great, and many traditional and non-traditional buyers stepped back in all at once. The key question now is whether this can continue. Investor demand will be gauged by weighing outflows against inflows and cash balances, but with banks strong and healthy, the drivers of new issuance seem to be in place for when we emerge from confinement. This should allow investment-grade investors to act on opportunities.

At the lower end of the quality spectrum, while we expect a record amount of debt to be downgraded from investment grade to high yield, the Fed’s move to broaden its mandate and buy recently fallen angels will offer support for better US high-yield issuers.5 Many other governments have also taken action,6 and their crisis-response measures are helping borrowers deal with the credit crunch through aid such as loans, tax relief and contributions to labour costs. Unfortunately, even the generous amounts pledged by governments and central banks will not be enough to support all high-yield companies.

The greatest downside risk for high yield is the risk of recession, which is already underway. At around four times EBITDA (Earnings before interest, tax, depreciation and amortisation), high-yield companies are not overly leveraged by historical standards,7 but the sharp contraction in economic activity will put many in serious financial difficulty.

More broadly, the unexpected and extensive restrictions to economic activity have not given businesses time to adapt, and all companies’ profits have been hit. This may explain why the initial sell-off in credit was indiscriminate. Yet it is also easy to see which companies and sectors are more materially impacted – energy, consumer cyclicals, retail and autos to name a few. When people are locked in their homes, they aren’t in shopping malls, on airplanes or filling their tanks with petrol.

While the majority of the market moves were related to the economic ramifications of the COVID-19, the spat between the Saudis and Russians over the oil price meant a double whammy in the energy sector, despite the agreement reached on April 12.8

As this situation endures, investors should prepare for more volatility, downgrades and defaults. Despite the market rally, March saw numerous downgrades and moves to negative watch or negative outlook by the major credit-rating agencies.9 Not only were companies unprepared for the aggressiveness of the restrictions but, having learnt the lessons of the global financial crisis when they were criticised for being too slow to act, the credit-rating agencies have been more proactive this time around in acknowledging the risks.

The most significant ratings moves were in the hardest-hit sectors – travel and leisure (very few airlines and airports were untouched), energy and consumer cyclicals. Energy has been particularly hard hit, suffering the lion’s share of both downgrades and defaults as these started to emerge. Autos have also fared badly, with all major auto manufacturers either downgraded or moved to review for downgrade or negative outlook. Ford, for example, was downgraded to high yield by S&P and cut a further notch into high-yield territory by Moody’s.10

The Fed’s support will help recent and future fallen angels and may also lead to a compression in BB spreads. At the other end of the spectrum however, valuations of B-rated companies being downgraded to CCC do not seem to adequately reflect the negative-rating trend. With CCC spreads in excess of 1,400 basis points as of April 13,11 B-rated bonds downgraded to CCC should see their spreads widen.

Investors should expect to see more defaults the longer the restrictions remain in place, but at current yield levels, our view is that long-term investors are being overly compensated for default risk in high yield, which could create an attractive entry point into the asset class. For instance, current spreads in US high yield imply a five-year cumulative default rate of about 40 per cent, and around 35 per cent in European high yield, assuming the worst (i.e. zero recovery rates). By way of context, the highest historical global five-year cumulative default rate was 32 per cent.12

Taking a long-term view, one could argue everything is cheap across the quality spectrum – provided investors can avoid companies that will default. This helps explain why we have seen such aggressive demand for credit in recent weeks. However, some companies are better positioned to navigate these troubling times, with a lower deterioration in financial metrics and cash flows.

It is important to maintain a balanced approach to credit portfolios, always having some dry powder available and being willing to take opportunities. For example, now could be a good time to sell assets that may offer solid long-term prospects but seem at greater risk in the short term, with little transparency as to when they might recover. On the flip side, other assets could be trading at similar spreads and prices while having sold off purely due to weak technical factors. If they offer more certain cash flows over the short to medium term, they could present buying opportunities. While not all risks are equal, their prices can be similar.

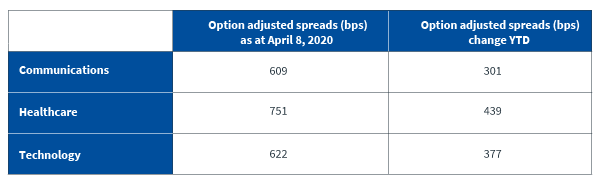

In both investment grade and high yield, sectors such as healthcare, pharma, telecoms and cable present opportunities. When everyone is stuck at home, they will be using their mobile phones, internet and cable, while healthcare and pharma not only remain open for business, they also have a big role to play in all market environments as non-cyclical sectors. In addition, high yield names in these sectors sold off heavily relative to their fundamental quality (Figure 5). This adds to their attractiveness in the short term.

Figure 5: Spread changes January to April 2020 in selected sectors

Source: Bloomberg Barclays Global High Yield ex-CMBS ex-EMG 2% capped, as of April 8, 2020

In investment grade, banks are also seeing interest from investors – not because they are immune to today’s crisis, but because they are well capitalised and prepared for such a stressed environment (a consequence of post-financial crisis regulation). Having such large capital buffers today is helping many to stay afloat and support other parts of the economy. Yet even within stronger sectors, it is important to remain selective – Italian banks entered this crisis from much weaker positions than their US peers, for example.13

At this point it is impossible to estimate how quickly the global economy might recover from such an exogenous shock. The lack of transparency and experience in dealing with a global health crisis will likely result in alternating periods of weakness and strength in risk assets as markets and consumers grapple with the true pace and depth of the economic impact and optimism waxes and wanes.

Some areas will be less impacted and will recover fastest, while others will not be able to bounce back as quickly. Particular attention should be paid to consumer psychology, which will take time to recover. When will people be comfortable again going shopping, to restaurants, to concerts or to conferences even when they are allowed to? We won’t know the answer for some time, meaning that in sectors like retail and restaurants, earnings will be weak and forward expectations will be non-existent.

When capital preservation is your focus, the biggest task for investors is identifying which sectors and companies will have the worst earnings disruption, with the least certainty as to when they may recover. Investors can handle bad news better when they can fully understand the risks and calculate the downside impact. Conversely, it is hard to make a case for investing in companies and sectors where the ability to model revenues and cash flows is difficult over the medium term. Finding companies in sectors where there is a relatively clear and stable picture over their prospects will be key to weathering this storm.

References