"Global currencies don’t so much fail as they are eclipsed by a stronger competitor."

Michael Howell

CrossBorder Capital, November 29, 2017

“...Cecily, you will read your Political Economy in my absence. The chapter on the Fall of the Rupee you may omit. It is somewhat too sensational.” Oscar Wilde, The Importance of Being Earnest

Monetary history is frequently sensational. Thus, an auspicious day in monetary history is August 15th, 1971 because it is the date US President Nixon dramatically halted the dollar’s convertibility into gold, effectively ending the post-war Bretton Woods fixed exchange rate system. Another equally important date is September 25th, 1936 when Britain, France and the US signed the Tripartite Agreement. This was effectively the precursor to the Bretton Woods’ gold exchange standard (GES), where other currencies were indirectly linked to bullion through the paper US dollar. In 1936, the three countries agreed to maintain their currency parities against each other and in-line with gold. A third, far less well-known, but arguably as important date is ‘sometime in’ July 1974 (the date is as mysterious as the agreement), when former Salomon Brothers partner Bill Simon negotiated a key ‘cloak-and-dagger’ deal between America and the Saudis. In return for Saudi Arabia pricing oil and accepting payments solely in US dollars (and implicitly agreeing to re-invest much of the proceeds back into US Treasuries), the US offered military hardware and external military support. The other OPEC nations quickly nodded through the Saudi lead. Call this the oil exchange standard (OES). The deal was never publicised. The US Treasury deliberately hid Saudi purchases of US government debt, using the obscure ‘add on’ facility at bond auctions. These purchases today may total around US$350-400 billion, but possibly far more. Whereas the GES lasted de facto from 1945 to 1971, or twenty-six years, the OES has, so far, lasted 43 years, or almost twice as long. Its length underscores its importance because the OES has been as critical for US capital as the GES, and arguably even more so. The OES underpins the dominance of the US dollar in the global financial system, and the OES, in turn, has significantly influenced the broad direction of US foreign policy since 1974. However, events may be changing, triggered by the rise of China and the on-going substitution of US shale for Saudi oil.

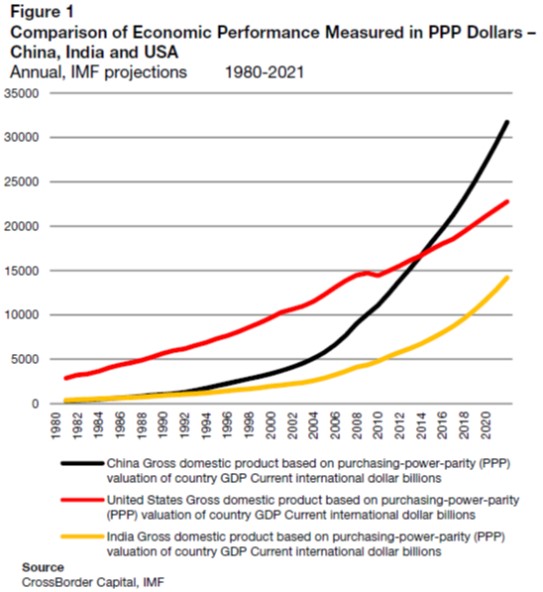

The bigger trend here is the rise of China. Global currencies don’t so much fail as they are eclipsed by a stronger competitor. Robert Mundell, architect of the Euro, rightly claims that ‘…every great country has a great currency.’ Too many in the West underestimate China’s potential. See Figures 1 and 2. China is the World’s largest trading nation. It dominates the demand for key commodities, such as copper. Its economy in ‘real’ PPP terms is now larger than the US; its credit system is already equal in size and its Central Bank, the People’s Bank, stands one fifth bigger than the mighty Federal Reserve. China’s pool of liquidity barely accounted for 6% of the World total in

year 2000, but since then it has soared by over 14-fold to reach parity with the US and the Eurozone. Throughout history, economic power is reinforced by the generation of seignorage – the ability to sell debt to others and ultimately pay for any balance of payments deficit with your paper money. For example, the US dollar circulates globally as the chief vehicle currency and is widely-held as a store of value, rather than being redeemed for another unit or swapped for gold. China not only wants to join this reserve currency club: she wants to dominate it, ultimately unseating the US dollar and specifically driving American power out of Asia in the near term. Although the US rightly fears China’s geo-political ambitions, it has been lately surprised that China is largely pursuing this policy by economic rather than military means. For example, See US Secretary of State Rex Tillerson’s October 2017 speech on US-India relations.

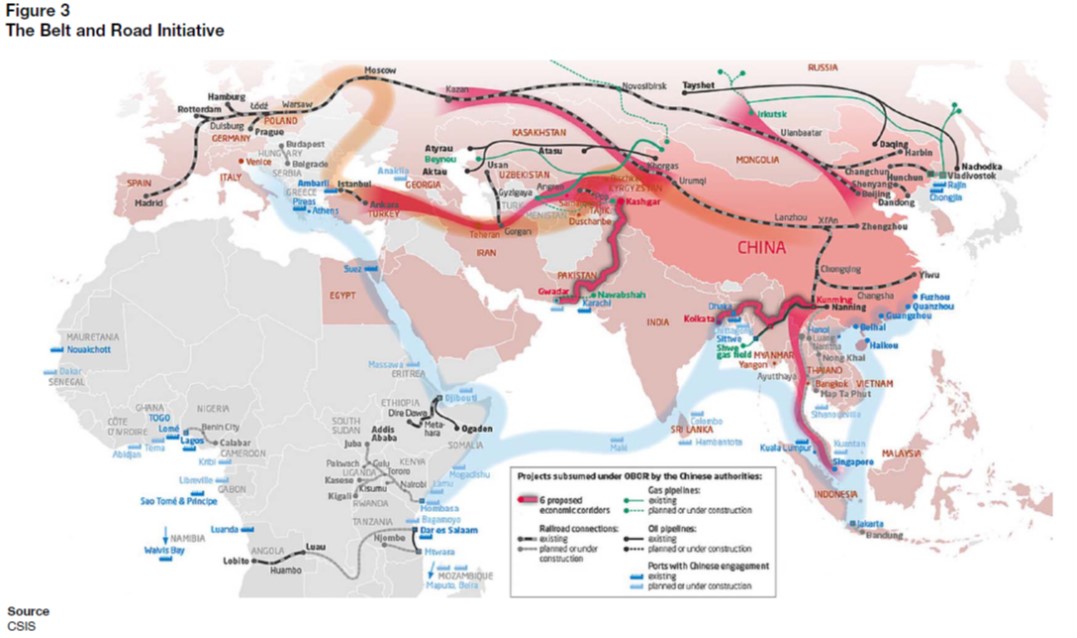

China’s economic initiative is crystallised in the US$4 trillion Belt and Road Initiative (BRI), the huge (multi-Marshall Plan like) infrastructure programme that embraces Central Asia. See Figure 3. The ambitious scheme touches 68 nations populated by 4.4 billion people. Taking prevailing World Bank estimates of the income elasticity of infrastructure spending, this programme could easily expand regional GDP by 35-40%. Taken over a quarter century, it would add 1-1½% annually to pan-Asian growth. The BRI is not just a geo-political route, but it is also the path that points to the rising importance of the Yuan. Nations along this new financial silk road will increasingly borrow and trade in Yuan. China’s policy banks are already active in granting loans, much as the US money centre banks did to finance Latin America’s infrastructure programmes in the 1960s and 1970s. By earlier example, Britain established the pound sterling as the common standard of value across its expansive nineteenth century Empire and later sustained it through the system of Imperial Preference. London’s financial markets grew fat on reinvesting these flows. Looking back, the dominance of the US dollar and Wall Street both rested on the GES and later the OES. Many persistent warnings from economists for decades that America’s economy was declining as a share of World GDP entirely missed the point that throughout the role of the dollar was paradoxically getting bigger as many newly emerging economies shadowed the US unit. Now these same economies, e.g. the Philippines, are turning towards China.

China, joined by ‘sanctions’ outcasts, such as Russia and Iran, and tacitly encouraged by Europeans that have been heavily fined by the US authorities for abusing their dollar transactions, are all actively working to break the US dollar monopoly. This means deliberately undermining the OES: a task now more easily achieved because China is a major buyer of Middle East oil, and Russia has taken an important initiative in the Syrian conflict. Already Russia trades oil for Yuan with China. The latest twist involves the ‘on-off’ planned privatisation of Saudi oil giant ARAMCO. Internal fiscal pressures compel the Saudis to sell, but as the odds of a public sale diminish the likelihood of a private sale rise, and it seems highly probable that a Chinese entity will ultimately stump up the cash. The price for this face-saving deal will likely involve some concessions on pricing oil in Chinese Yuan.

The loss of the oil market may not be fatal for America, but at US$0.8 trillion per annum of cross-border trade, it is significant. Moreover, it may mark the beginning of the US dollar’s decline. Other commodities will surely follow the petro-yuan, perhaps starting next with copper and gold, where the Shanghai futures exchange is already a volume leader? One future result is that the vast pool of dollars held offshore by commodity producers and hedgers, itself oft-used to fund Western banks, looks in real danger of serious decline. Could this necessitate more replacement QE from Western policy-makers? Peering further ahead, a pool of off-shore Yuan may build up along the BRI, although for now this is likely to be largely held by China’s allies in Central Asia. China’s rapacious appetite for commodities as infrastructure expands will boost Africa. But let’s not forget the fact that Africa itself is entering a rapid growth phase as its population quadruples from one billion to a whopping four billion over the next century: perhaps the biggest global population bulge ever? African urbanisation rates will surge, further underscoring commodity demands and further cementing the importance of

China and the Yuan.

Inevitably, there will be a new geo-political race for resources and influence. US military spending must surely rise, but this comes at a time when the US dollar looks vulnerable and the debt burden from other US fiscal commitments, e.g. Medicare and government pension liabilities, is already worsening fast. What’s more, US productivity growth, the ultimate driver of currency power, has spluttered since the 2007/08 Global Financial Crisis, certainly compared to China’s success. The post-war dominance of American capital, what we dub the ‘globalisation’ model, has depended upon a strong US dollar and low interest rates. Other foreigners apart from the Saudis have poured money into US ‘safe’ assets in recent decades. Not only has the interest rate on these debts been low, but the purchasing power of the US has allowed technology-rich US capital to flood overseas. Rising interest rates and a falling US dollar will conspire to progressively weaken this globalisation model over time. It still could be a long journey: America eclipsed the British economy in size around 1870, but it took the US dollar until the 1950s to dominate sterling. But every journey begins with a first step and China’s Yuan is stepping out.

Crossborder Capital uses this liquidity data to run a Fixed Income Macro Fund that benefits from long volatility and relative value strategies. It has the ability to gain from rising and falling markets .