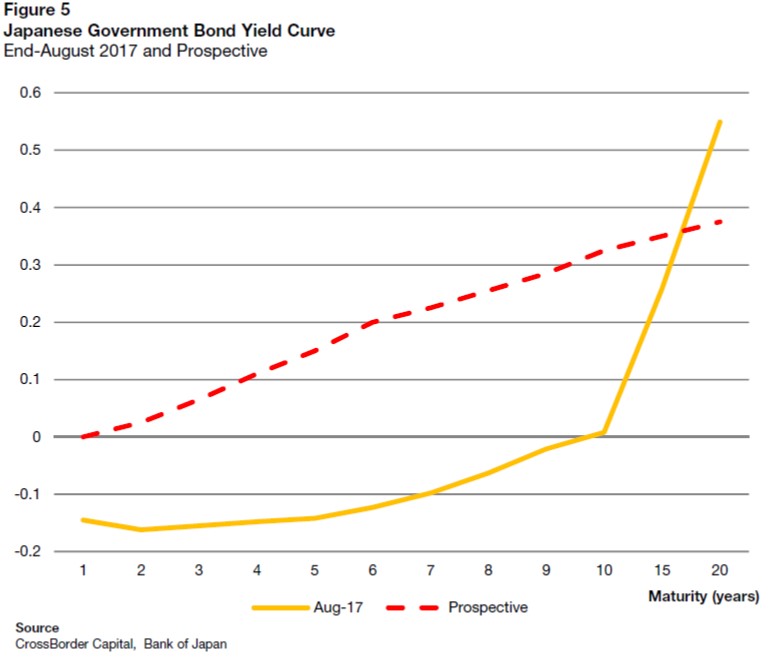

On top, upward pressure on Japanese interest rates from higher domestic liquidity will build, so forcing JGB yields higher and likely spilling over negatively into international bond markets. There is a growing risk to the 10-year JGB, which could suffer an upward yield spike from zero to around 30bp.

Key Points

As a global supplier of consumer goods, Japan has for decades enjoyed a strong Yen, high street deflation and a surging bond market. Now, re-constituted as predominantly an Asian regional supplier of intermediate goods, Japan faces different challenges and consequently deserves new policy and currency regimes. It may in future behave increasingly like a typical emerging market, choosing a more stable currency against a pan-Asian basket, but at the cost of more volatile domestic liquidity flows, particularly, when Chinese and pan-Asian liquidity are also expanding as now. These increased flows may be channelled initially into Japanese equities and latterly into outward capital flows.

A Dominant and Cyclical China

Two recurring themes in our research acknowledge: (1) the whopping size both of the Chinese economy and her international financial flows, and (2) the cyclical nature of the Chinese economy and the active role played here by the People’s Bank (PBoC), now the World’s biggest Central Bank by balance sheet size. Put another way, China unquestionably influences, if not controls, World interest rates through the spillover of inflationary pressures and term premia factors. These effects are particularly pronounced across Asia, where Chinese led supply-chains link together regional producers. The People’s Bank (PBoC) has now been easing policy since January 2016, and Chinese private sector liquidity has more recently enjoyed a strong cyclical rebound as the Chinese economy accelerates.

In this report, we draw out the implications for Japan. Japan is increasingly subject to these China-led regional economic forces which have exacerbated upward pressures on the Yen and downward pressures on Japanese high street prices, thereby recently forcing the BoJ into extreme and unconventional monetary actions. Curiously, the scale of BoJ stimulus has lately tailed-off. However, we expect it to soon restart given renewed impetus from China and the latest visible pick-up in the tempo of cash flow generation by Japanese firms.

Looking ahead, the bottom-line is that in this new, supply-chain World Japan is set to act more like a typical emerging Asian economy by keeping its currency stable against its regional peers, including the Yuan, and allowing Japanese financial markets to take the strain through greater liquidity swings. If we are correct, the Japanese interest rate yield curve will continue to steepen, with the authorities ultimately allowing the policyanchored 10-year JGB yield to move more freely once again. This should cause a ‘renormalisation’ of the Japanese term structure around a higher JGB yield base and may well have global implications, because Japanese institutional investors have been instrumental in the global ‘hunt for yield’. Thus, prospectively higher yields in Japan should add to international pressure towards rising global bond yields.

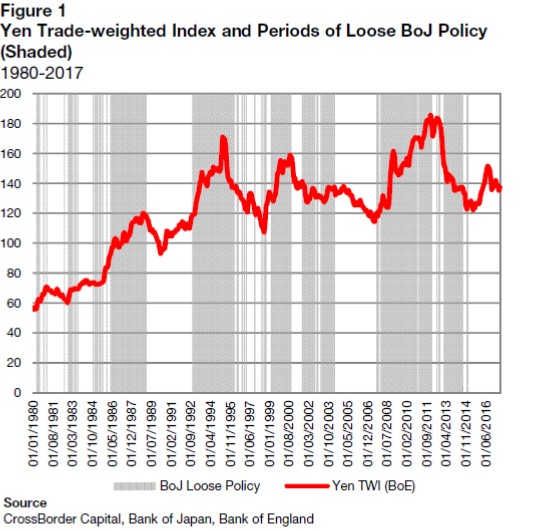

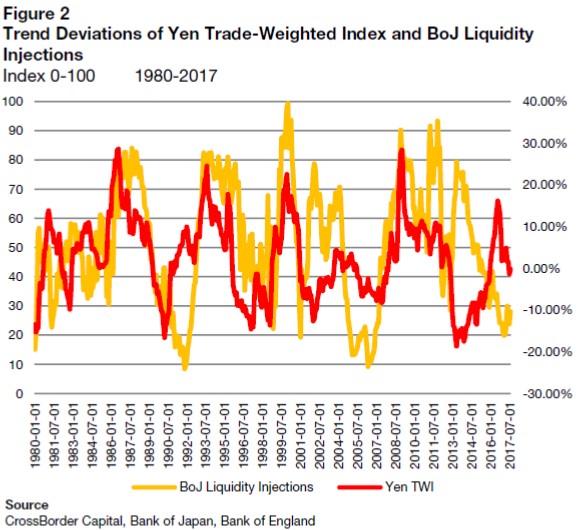

Historically, Japanese monetary policy has often been reactive to international events in order to hold down extreme upward pressures on the Yen. Looking backwards, these pressures typically emanated from the US rather than China. Thus, US dollar weakness and extraordinarily large trade surpluses were frequently met with monetary relaxation by the Bank of Japan, as forex reserves accumulated and capital flowed in. This is shown in Figures 1 and 2. Figure 1 reports the trade-weighted Yen plotted against periods of loose BoJ monetary policy. Typically, apart from the period since 2012, a strong (weak) Yen has been associated with monetary accommodation (tightness). Figure 2 shows this more explicitly, by charting trend deviations in the trade-weighted Yen against actual liquidity injections by the BoJ. It seems clear that until 2012, the BoJ added liquidity when the Yen was rising faster than its trend and pulled-out liquidity when the Yen was weak. Yet, since 2012, it appears instead to have deliberately and pro-actively sought to weaken the Yen. Admittedly, the late-1980s asset bubble and the recent period of price deflation have also seen domestic factors distort policy. Expressed in liquidity terms, the pre-2012 monetary policy meant more stable overall Japanese liquidity, since BoJ Central Bank activity moved oppositely to the direction of private sector flows. In contrast, the recent policy change has made liquidity more pro-cyclical and has meant that the CrossBorder Capital Central Bank and Private Sector liquidity indexes for Japan have seen their typical low correlation (0.17) quadruple to a sizeable positive 0.71.

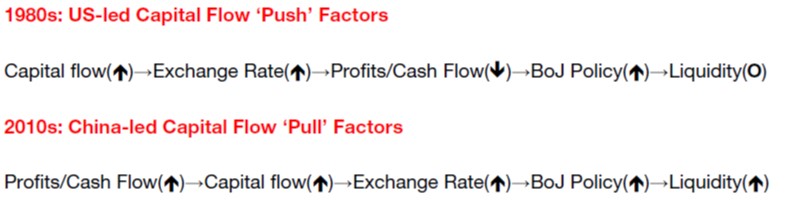

As we explain later, the change in monetary policy regime may reflect the different nature of Japanese capital inflows, from ‘push’ to ‘pull’ factors:

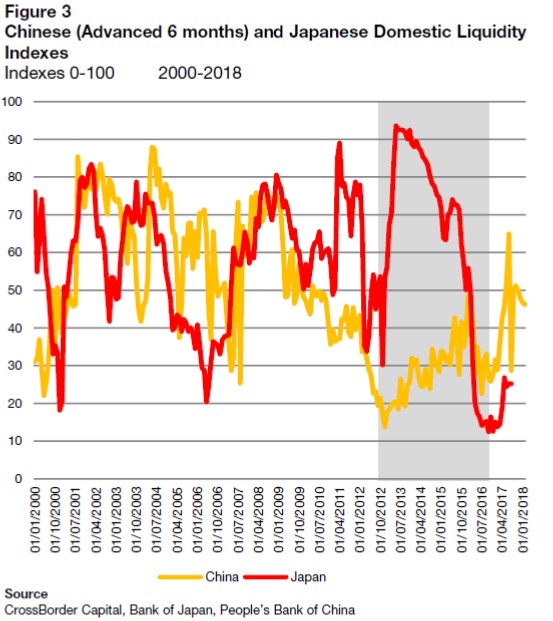

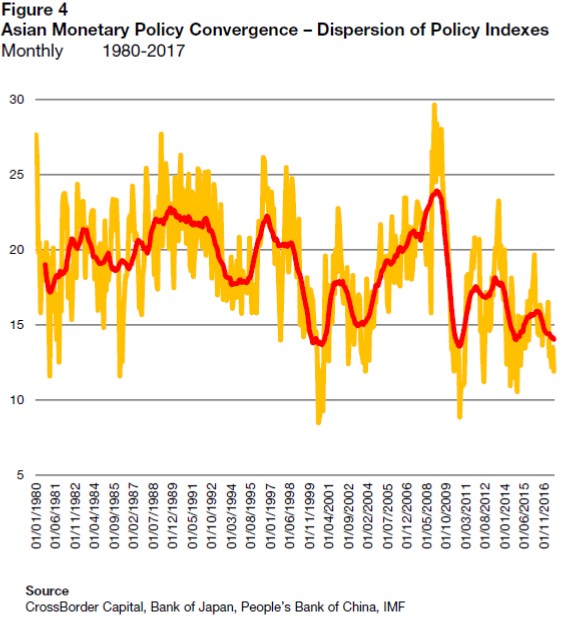

International considerations may again be set to take centre stage, partly because the US dollar is facing a period of structural weakness, but, more importantly, because the Chinese economy is gaining greater traction and influence across Asia, with another surge in productivity likely as the regional economy accelerates. Already, as Figure 3 shows, the cash generation of Chinese firms is increasing and leading the same cycle in Japan by some six months, allowing for the earlier 2013-14 positive effect on cash flows from Abenomics. In the 1980s, capital flows were ‘pushed’ out of the US into Japan by the liberation of capital flows and easy US money policies. This boosted the Yen, but hit Japanese export growth, profitability and cash flow, and led a reactive BoJ to loosen policy to help maintain domestic liquidity. In the post-GFC period, movements in the tempo of the Chinese economy alter prospective capital returns and cash flows, and so ‘pull’ global capital into the region, thereby putting upward pressure on currencies. Regional Central Banks including the BoJ, therefore, ease policy pro-cyclically to maintain currency stability and, as a result, generate more significant liquidity cycles. Another way of explaining this change is that, in the 1980s, the BoJ was targeting a stable liquidity regime, but, in the 2010 era, it has been targeting a stable currency regime, particularly against Asian units. One result, as Figure 4 illustrates, is the convergence of regional monetary policies as indicated by taking the cross-sectional dispersion of monthly Central Bank policy indexes across 17 Asian markets. Dispersion has lately dropped from an average centred on 20 index units, to around 15. In short, the Asian monetary cycle is increasingly pro-cyclical and more-and-more driven by China’s PBoC. This makes all regional policy-makers, even the BoJ, behave like an emerging market Central Bank by monetizing their capital inflows. Therefore, unless the Japanese authorities want a strong Yen, Japanese monetary policy must ease again alongside this latest evidence of rising private sector liquidity.

Structural Economic Change

How has the Asian economy changed? Put into context, Japan’s new challenges are structural and in large part the result of regional economic evolution, more competition and integration of production with a resurgent China. An important research paper written in 2014 by BoJ economists for the Asian Development Bank (ADB) confronted these issues head-on (See: Emerging Economies’ Supply Shocks and Japan’s Price Deflation: International Transmissions in a Three-Country DSGE Model, ADB Working Paper #459, Feb 2014). This paper spells out the fact that Japan has a consumer goods trade surplus of 0.7% of GDP and a 0.5% of GDP intermediate goods trade surplus with the US but a 1.8% of GDP trade deficit in consumer goods alongside a 2.1% trade surplus in intermediate goods with China.

The newly associated China/Japan transmission mechanism can be explained using the example of a positive productivity shock occurring in China’s product assembly sector, such as smart phones. Let Chinese production and exports of these smart phones increase and assume that Japanese and US imports of them expand alongside. The jump in Chinese production stimulates the domestic demand for more parts and components. Japan, being a vertically specialised competitive supplier in a supply-chain, increases its exports of these intermediate goods to China, while the US, which is essentially horizontally-specialised, does not. The resulting larger Japanese and US trade deficits with China from the increase in imports of smart phones is mitigated in Japan’s case by these extra component sales.

The smaller trade deficit in Japan than in the US means that Japan faces the lesser financing burden. This leads to Yen appreciation against the US dollar and, consequently, greater downward pressure on the inflation rate in Japan than in the US. This downward inflationary pressure has historically been intensified through the Yuan/ US dollar peg, which in the past has forced the Yen to appreciate and frequently overshoot. In short, China/ Japan supply chains and the traditional Yuan/ US dollar-pegged exchange rate regime have been important factors explaining past deflationary impacts of Chinese supply shocks on to Japan.

This mechanism has coloured Japan’s low inflation and deflation regimes through the 1990s and the 2000s. Since the 1990s, there have been several significant increases in productivity and supply capacity in the Chinese export sector. On top, several Japanese multinational firms transferred their product assembly bases to China and other emerging Asian economies. Thus, Asian firms developed pan-regional supply chains and established international vertical specialization where Japan supplies the parts and components for product assembly in these emerging economies. Thus, regional supply shocks following the intra-Asian transfer of these production bases, technology, and management expertise have boosted both exports to Japan and imports of parts and components from Japan, without significantly denting Japan’s overall trade balance. Greater trade integration has therefore put long-term upward pressure on the Yen, reinforced deflationary pressures on Japan and tied Japanese firms more closely to the pan-Asian and Chinese business cycle.

Looking ahead, additional future positive supply shocks in emerging Asian economies will result in a sustained Yen appreciation and must add to further deflationary pressures in Japan. To avoid large-scale Yen appreciation and address deepening domestic deflation, the BoJ will have to pursue persistent and more aggressively accommodating monetary policies and convince the emerging Asian economies, particularly China, to adopt more upwardly flexible exchange rate regimes against external currencies, such as the US dollar.

Investment Implications

In other words, whereas in the 1980s the BoJ targeted stable liquidity (albeit ultimately unsuccessfully), it now appears to be more actively targeting the Yen by injecting funds when it is strong and withdrawing funds when it is weak. This changed policy mix is entirely consistent with the demands of this new supply-chain World. In short, the days of persistent Yen strength against other G7 currencies when Japan was predominantly a global supplier of final goods may be over. Instead as a supplier of intermediate goods to China and emerging Asia, Japan needs a stable Yen at least against the regional currency units, notably the Yuan.

Looking ahead what does this mean? We suggest three themes:

1. Greater correlation and stability across Asian currency units, i.e. the formation of a de facto Asian currency zone (‘Asian dollar’) that will be ultimately led by China.

2. A more pro-cyclical BoJ and greater ‘emerging market-like’ volatility in Japanese and pan-Asian liquidity conditions

3. Potentially bigger JGB yield curve movements and bond yield swings and greater market cyclicality

Put another way, the Asian productivity miracle is moving outwards through the region as production diversifies geographically. Economic integration means that real exchange rates deserve to move more closely together and, in order to maintain competiveness, policy is likely to focus on greater currency stability. This means that monetary policy, and hence liquidity, will become more pro-cyclical, with asset markets taking over more of the adjustment burden from currencies. Moreover, the driver of the Asian business cycle is increasingly the Chinese producer rather than the American consumer, which may mean that Japan starts to resemble an Asian emerging market in performance.

Another big question is what happens to the JGB market? This has been heavily distorted largely by BoJ ‘forward guidance’ that has persuaded investors that policy-makers can maintain the near-zero yield on the 10-year bond. It has been clear from our research work that, whereas the difference between private sector liquidity and Central Bank liquidity drives currencies higher, the sum of stronger Central Bank and private sector liquidity pushes investors out of ‘safe’ government bonds and into riskier assets, like equities, real estate and corporate debt. Hence, if we are correct and Japanese and pan-Asian liquidity are set to turn much higher, expect a renormalisation of the JGB yield curve. This will mean higher yields across all tenors. It should also mean the end to negative convexity at the 10-year tenor and around a 30bp relative rise in 10-year yields. See Figure 5. This effect will likely be transmitted to international bond markets because Japanese investors have been foremost in driving the international ‘hunt for yield’ and they stand closer to now realising higher yields at home.