-

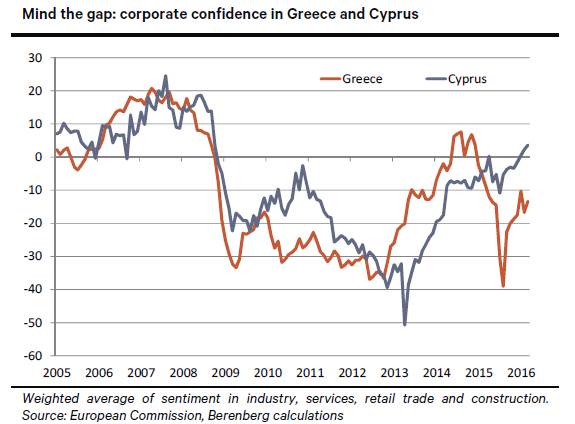

Small country, great rebound: Three years after falling into a deep crisis, Cyprus has successfully left its EU IMF adjustment programme. Following the return to growth last year, corporate confidence has surged to its best level since September 2008. The island at the Eurozone periphery is on track for a long and strong recovery.

-

The European approach is working: Cyprus thus follows the examples of Ireland, Portugal and Spain, which also exited their financial support programmes with flying colours. By and large, the European approach to offer conditional credit to euro member countries that implement serious reforms is showing results. Of course, whether these countries will stay on the recovery track will depend on their domestic political will. Serious reform reversals could still turn out to be very costly. As always, life remains full of risks.

-

Greek misery: Only one of the erstwhile euro crisis countries remains mired in misery, dependent on further external support to prevent a wholesale collapse. What explains the gap between these two close neighbours?

-

Advantage Cyprus: To some extent, any comparison between Cyprus �and Greece is unfair. Cyprus is a small open economy blessed with a fairly flexible labour market that is partly a legacy of British influence. This makes it easier to cope with dramatic shocks, such as the virtual collapse of its overblown banking system some three years ago. But that is less than half the story. After a rough start and despite the occasional hiccups, Cyprus simply did what it had to do, implementing most of the required reforms. The results speak for themselves.

-

A recovery aborted: To explain why Greece is doing so much worse than Cyprus, Spain and Ireland, we have to look at Greek politics. After a long crisis that was made unnecessarily painful by an overdose of austerity, Greek corporate confidence started to perk up in the summer of 2012. It did so for two reasons. At home, the just elected prime minister Antonis Samaras got serious about pro-growth structural reforms, working with – rather than against – Greece’s only willing lenders. In the overall Eurozone, ECB president Mario Draghi ended the systemic euro crisis by promising to act as a Fed-style lender of last resort if need be for fiscally compliant countries.

-

The Varoufakis effect: By late 2014, Greek corporate confidence had recovered to an almost six-year high. Greece seemed poised for up to 3% growth in 2015. But politics got in the way. With the rise of political risk in late 2014, confidence started to crumbled. When Yanis Varoufakis became finance minister in January 2015, starting to reverse reforms and going for full confrontation with Greece’s creditors, Greek confidence plunged like a stone, sending Greece back into recession. Rarely has a finance minister done so much damage in such a short time.

-

Shaky Greece: Since prime minister Alexis Tsipras finally fired Mr Varoufakis nine months ago, Greek confidence has recovered somewhat. But it will remain weak until Mr Tsipras starts to follow the Cypriot example and simply implements the bulk of the required reforms, instead of picking one fight after the other with Greece’s lenders.

Source:

www.berenberg.com

Link to the original document

Disclaimer

This document was compiled by the above mentioned authors of the economics department of Joh. Berenberg, Gossler & Co. KG (hereinafter referred to as “the Bank”). The Bank has made any effort to carefully research and process all information. The information has been obtained from sources which we believe to be reliable such as, for example, Thomson Reuters, Bloomberg and the relevant specialised press. However, we do not assume liability for the correctness and completeness of all information given. The provided information has not been checked by a third party, especially an independent auditing firm. We explicitly point to the stated date of preparation. The information given can become incorrect due to passage of time and/or as a result of legal, political, economic or other changes. We do not assume responsibility to indicate such changes and/or to publish an updated document.

The forecasts contained in this document or other statements on rates of return, capital gains or other accession are the personal opinion of the author and we do not assume liability for the realisation of these. This document is only for information purposes. It does not constitute a financial analysis within the meaning of § 34b or § 31 Subs. 2 of the German Securities Trading Act (Wertpapierhandelsgesetz), no investment advice or recommendation to buy financial instruments. It does not replace consulting regarding legal, tax or financial matters.

Remarks regarding foreign investors

The preparation of this document is subject to regulation by German law. The distribution of this document in other jurisdictions may be restricted by law, and persons, into whose possession this document comes, should inform themselves about, and observe, any such restrictions.

United Kingdom

This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers.

United States of America

This document has been prepared exclusively by Joh. Berenberg, Gossler & Co. KG. Although Berenberg Capital Markets LLC, an affiliate of the Bank and registered US broker-dealer, distributes this document to certain customers, Berenberg Capital Markets LLC does not provide input into its contents, nor does this document constitute research of Berenberg Capital Markets LLC. In addition, this document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers.

This document is classified as objective for the purposes of FINRA rules. Please contact Berenberg Capital Markets LLC (+1 617.292.8200), if you require additional information.

Copyright

The Bank reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the Bank’s prior written consent.

© October 2015 Joh. Berenberg, Gossler & Co. KG