The quest for uncorrelated returns can be an expensive pursuit, especially in terms of opportunity cost.

Stuart Canning

M&G Investments, Episode, 11 June 2019

The rise and fall in popularity of absolute return funds is a case in point. For years, the Targeted Absolute Return sector was among the most popular among UK and European fund buyers, but with huge outflows across Europe and some branding the funds as ‘useless,‘ it’s fair to say there is noticeable disenchantment today.

Should we be surprised by this? And is there anything changing fashions in investment strategies can tell us about the state of market beliefs today?

The rise and fall

In many ways, this should not be a complete surprise. Specifics vary, but in general, absolute return funds set themselves a very challenging goal – generate positive returns, meaningfully above cash rates, with limited correlation to the major asset classes, and with low volatility. Something approaching the holy grail of investing, in other words.

On top of this, absolute return was increasingly interpreted to mean ‘will not lose money’ and viewed to be a safer alternative to other strategies, or multi asset funds with a higher equity component.

Judged by these standards, disappointment at an industry-wide level was likely at some point. It is logical that the average return for a group of funds that are each designed not to take a large amount of market risk will be low. There is simply not enough alpha to go around. Some fund managers may do well, others poorly. On average returns will be low at best.

The reality is that it is very hard to find assets that are liquid and uncorrelated with either growth or rates, and those which offer secure income streams are often likely to be sensitive to the latter. For some strategies, this may not have been apparent in the immediate post-crisis years as wide credit spreads and steep yields curves provided attractive returns, often with little correlation to equities.

But funds with positive interest rate sensitivity have been hit by a double whammy since the pivotal moment in the middle of 2016. First, at such low rates in developed markets, prevailing valuations of safety weren’t able to deliver the returns many had become used to:

Second, in 2018, the changing market environment which resulted in a positive correlation between bonds and equities made it difficult for investors to generate returns in most asset classes in their long positions. Therefore, any predominantly long-only strategies relying on diversification to reduce volatility suffered. They may though have had relief from the fall in bond yields so far in 2019.

Heterogeneity

None of this is to say that it was inevitable that the most popular absolute return funds would disappoint, or that they do not have an important role to play for investors from here.

Rather, it is important to stress that absolute return is an objective, not a single style or strategy. There are numerous different ways of trying to generate a return with relatively low exposure to any single asset class, be it macro, long-short equity or absolute return credit to name just a few. Not all funds have pursued the positive rates/credit dynamic described above; most probably haven’t.

The heterogeneity of investment approaches within the sector are the reason why it is so hard to generalise, other than to say making positive returns without taking much overall market exposure will always be very difficult.

Opportunity cost

But while it is difficult to generalise about funds within the absolute return sector, its popularity in recent years tells us something interesting about investor psychology more widely. The desire for uncorrelated (from equities) returns reflects a prolonged aversion to equity risk, stemming from the trauma caused by the 2008 GFC and 2010-12 European sovereign debt crises.

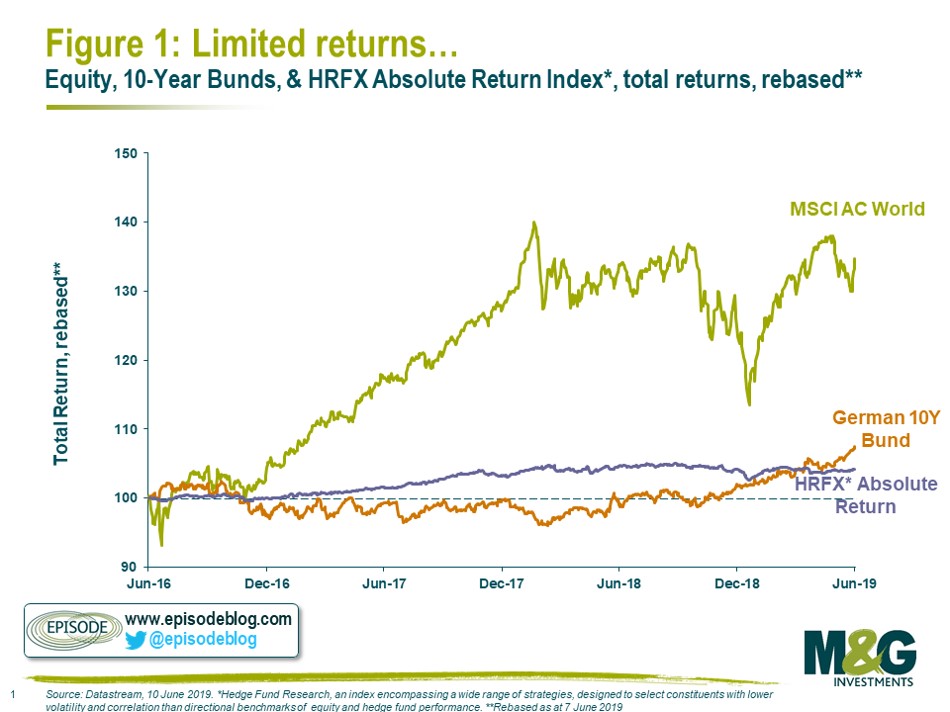

As we argued at the time of the pivotal moment, the value gap created by this aversion to equities in favour of safe assets, was likely to generate substantially higher returns for equities from that point on…although investors would have to be willing to accept volatility in order to reap the benefit (this is what is illustrated in figure one).

While returns from the absolute return sector have no doubt disappointed in the aggregate, investors are also likely suffering regret from a sense of missing out.

Where to from here?

Most investors probably don’t feel that the global investing environment is getting easier with talk of a US-China cold war, Brexit uncertainty, Italian political risk, trillions of euros worth of negative yielding bonds and a US President that changes policy with a few tweets.

A high equity risk premium and depressed interest rate expectations suggest a risky and uncertain future, with worries over economic growth outweighing any optimism of future returns. There is little evidence fund buyers are switching from absolute return to equities, for example.

In this environment, the offer of cash-plus returns with low volatility, is still hugely attractive. These are the outcomes absolute return funds aspire to and they remain in high demand. But whether investors will use the same funds in future or seek alternative approaches remains to be seen. Private or illiquid strategies may benefit from inflows due to their perceived low correlation, but investors should always consider the underlying risks they are taking. It is always worth being wary of investment fashions.

One factor which will be encouraging for some forward-looking investors is the dispersion in valuations within and across asset classes at present. This presents opportunities but no guarantee, as value investors will attest over recent years.

Irrespective, the fundamental challenge remains the same: generating returns with low volatility and low correlation will continue to be extremely difficult and few, if they are genuinely taking limited risks, will achieve this goal.

Time will tell whether regret will also be a factor in 2022 as it is in 2019 for those that have eschewed taking risk in the past few years. Worries about short-term volatility are an acute symptom of our times which investors with longer horizons would do well to ignore. In all likelihood they will again be rewarded for doing so.

Episode Blog

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.