|

Executive Summary

The run-up in the U.S. equity market since the Presidential election in November may be tempered, as the realities of politics and policy collide with the optimistic rhetoric of campaign promises. Without meaningful fiscal expansion, investors may see the equity rally stall.

- Post-Presidential election, investors believed lower corporate tax rates would favor small-cap companies over larger-cap companies, fiscal stimulus would support the industrial sector, regulatory reform would benefit financial and energy companies, and the four-decade bull market in bonds would end.

- The market behaved according to plan for a while and reached new highs but then reality set in: large caps are outperforming small caps, growth stocks are beating value stocks, international markets (especially emerging markets) are outpacing the U.S., and U.S. interest rates are no higher than they were at the start of the year.

- U.S. equity markets may still move higher but require a catalyst, such as fiscal stimulus in the form of targeted spending and tax cuts.

- Investors may wish to consider taking gains, maintain their exposure to core bond portfolios, and reconsider international markets, both Europe and emerging markets.

|

Without meaningful fiscal expansion, U.S. equity market investors may need to temper their expectations. Markets responded favorably to President Trump’s address to the joint session of Congress. However, unless the government delivers on its pro-growth strategy, U.S. equity markets may tread water for a while.

As soon as the 2016 Presidential election results were tallied, investors had the playbook for the “Trump bull market”:

- The U.S. would be the best game in town.

- Higher-taxed small-cap companies would benefit more from lowered effective tax rates than would larger U.S. companies, which had already written the tax code in their favor.

- A massive stimulus plan would support the industrial sector, while financial and energy companies would be advantaged by deregulation.

It was all to be reflationary and the four-decade bull market in bonds would finally be over. For a while the market behaved according to plan.

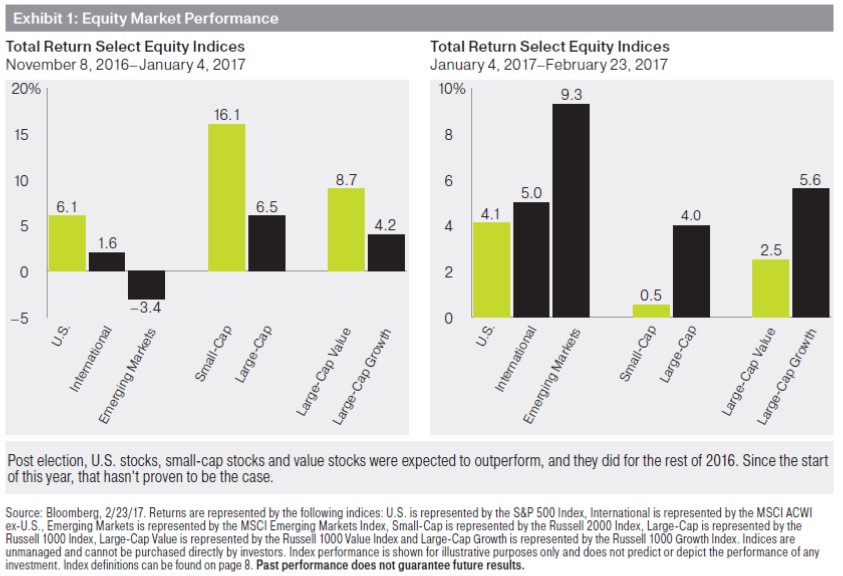

And then, a funny thing happened on the way to all-time highs in the S&P 500 Index. The composition of returns changed in the New Year. Large cap is beating small cap, growth stocks are beating value stocks, and international equity markets (emerging markets in particular) are outperforming the U.S. Long-term U.S. interest rates are no higher than they were at the start of the year and actually declined for the most of February. Exhibit 1

What changed? Nothing, and there’s the rub.

Gridlock in Washington, D.C. never really goes away (just ask Ronald Reagan who won re-election in 1984 by a landslide margin of 49 states to 1 and didn’t sign the Tax Reform Act until 1986). By the time investors awoke to the realities of Washington, the broad indices had already been repriced for stronger nominal growth, lower effective tax rates and a subsequent increase in earnings.

Skeptical Equity Markets Look for Catalyst

That’s not to say markets can’t go higher from here. They can, but a catalyst is needed, some change in policy to get us there. Fiscal stimulus—both in the form of targeted spending and tax cuts—could propel stronger growth, support earnings and drive equity prices higher.

resident Trump, on the campaign trail, called for massive absolute tax cuts for individuals and businesses. His administration and Republican members of Congress have said otherwise.

On individual taxes, Steven Mnuchin, now Secretary of the Treasury, told CNBC on November 30: “Any reductions we have in upper-income taxes will be offset by less deductions so that there will be no absolute tax cut for the upper class.”1

In addition, House Republicans favor lower corporate tax rates but support a border-adjustment tax or an elimination of the interest deduction to pay for the lost revenue. Mick Mulvaney, the former Republican Congressman from South Carolina tapped by President Trump to head the Office of Management and Budget, has been a staunch advocate for balanced budgets and less deficit spending.

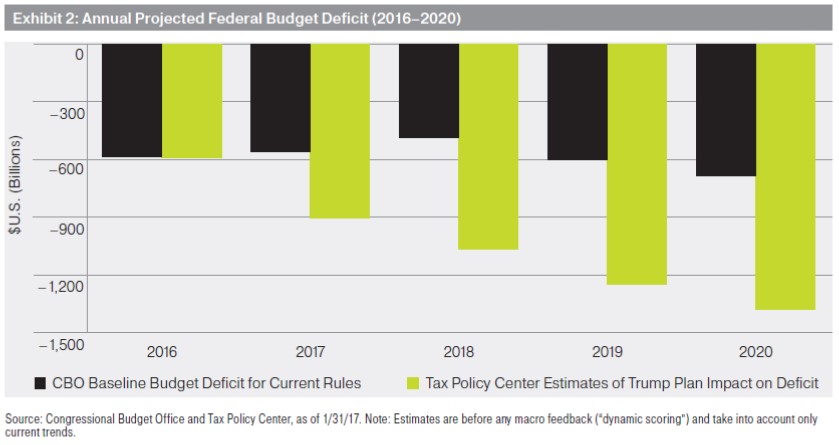

There’s a significant difference between absolute tax cuts funded by deficits and deficit-neutral tax reform. The former would broadly support corporate earnings while the latter would create select winners and losers within the equity market. The Tax Policy Center estimated that candidate Trump’s major proposals to cut taxes and boost defense and infrastructure would increase the deficit to more than $1 trillion in 2018, 2019, and 2020, all else being equal. Under current rules and with deficit-neutral tax reform, the deficit is likely to remain relatively flat over the next four years. Exhibit 2

To understand why this matters, consider the market’s reactions to the last two Federal Reserve (Fed) interest rate hikes, in December 2015 and December 2016. In 2015, by the time the Fed raised rates by 0.25% and had promised four interest rate hikes in the year ahead, the U.S. dollar had already rallied by 30%, triggering an earnings recession for U.S. multinational companies. There was simply too much money chasing U.S. dollar-denominated assets (i.e., U.S. Treasuries) without enough new U.S. Treasury supply coming on the market. The yield curve, with demand for long-term bonds up and supply not rising, flattened quickly and significantly as long rates plunged.

What the Bond Market Tells Us

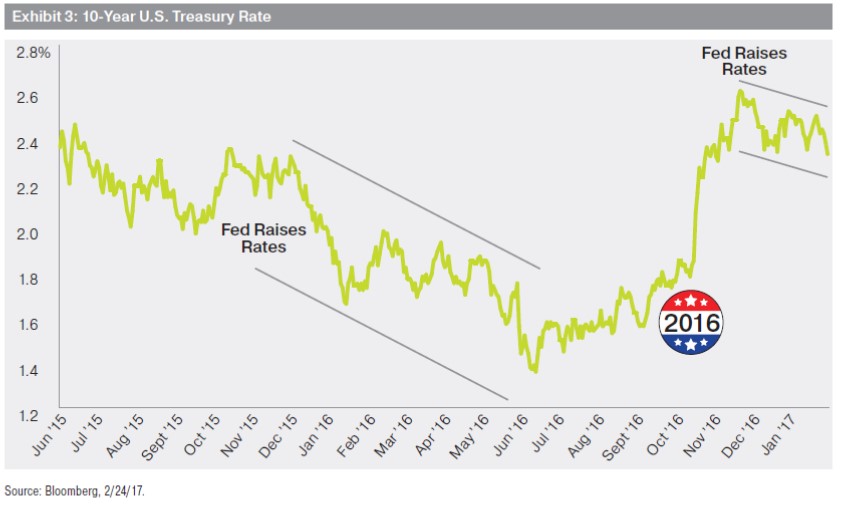

In late 2016, the bond market and the U.S. dollar responded more sanguinely to the Fed’s next 0.25% rate hike as the prospect of higher deficits loomed (i.e., greater supply to match the demand for U.S. dollar assets). Nonetheless, long rates, while meaningfully higher than they were on the eve of the Presidential election, have still gradually trended lower since the middle of December.

Of all the market indicators, the bond market gets it right more often than any other. The February rally in the long end of the curve signaled that the bond market is watching and waiting for stimulus and is having a hard time latching on to an extended reflation trade in a meaningful way. Exhibit 3

In the meantime, the Fed is already preparing the markets for at least two interest rate hikes this year—one in

June, the other in December. Investors can quibble over whether or not the economy is near full employment,

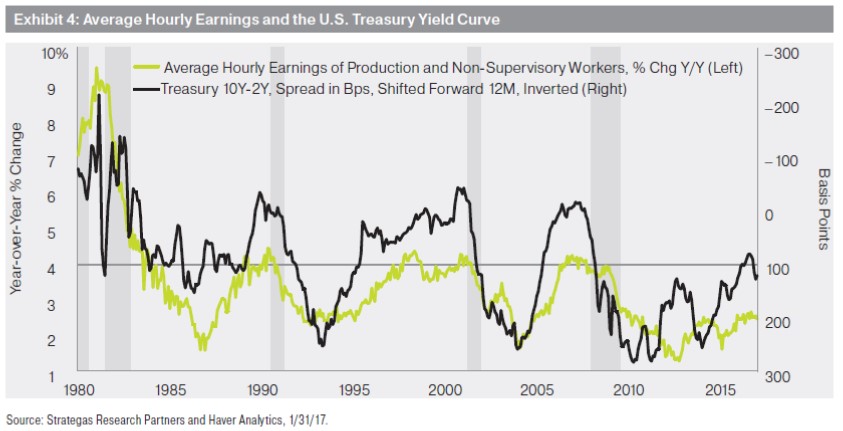

but with wages up 2.5% over the past year, it suggests that if the economy is not there yet, it may be close.

As the chart below demonstrates, business cycles typically end with wages rising and the yield curve flattening. Exhibit 4

For the cycle to continue, the Fed would ultimately have to back away from its tightening stance as it did one year ago, the Congress would have to commit to deficit spending, or both.

Three Strategies for Investors

What is an investor to do? Here are three suggestions:

1. It would be prudent for investors with extended positions or gains to right-size their portfolios and take gains. The silver lining in all of this is that the U.S. economy is already relatively healthy and inflation is still contained enough to provide the Fed cover not to tighten policy too quickly. So while U.S. equity markets are unlikely to climb substantially from here without fiscal stimulus, they are also unlikely to decline meaningfully if the administration’s domestic policy plans disappoint.

2. Investors should consider maintaining exposure to traditional core bond portfolios. Rumors of the demise of the four-decade- long bond bull market have likely been greatly exaggerated. For the U.S. interest rate regime to change over the intermediate to long term, the policy prescription has to be radically stronger than the status quo and it has to result in meaningfully higher nominal growth. For now, the U.S. equity market is more vulnerable to disappointment than the fixed-income market is to rates climbing substantially from current levels.

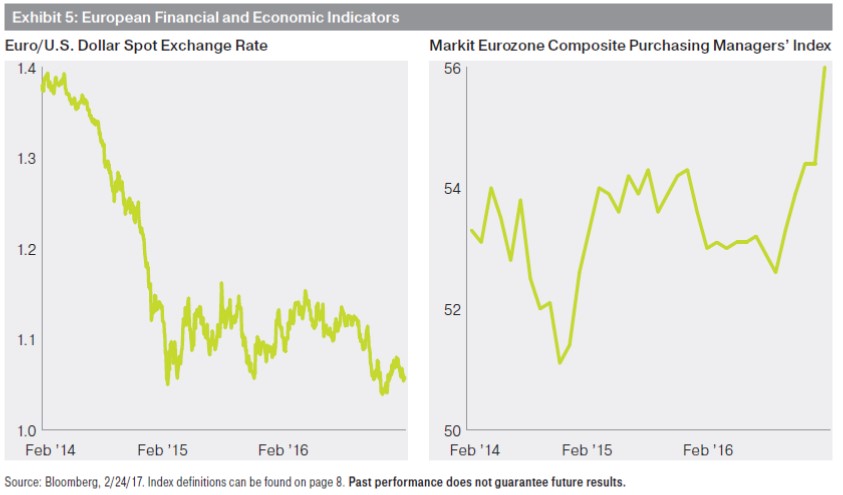

3. It may be time for investors to reconsider the international equity markets, where expectations are simply not as high as they are in the United States. Emerging markets are experiencing a cyclical recovery out of last year’s recession, particularly in commodity-producing countries like Brazil and Russia. China continues to benefit from the lagged effects of massive stimulus, while trend growth in India continues to improve.

For its part, the European economy is growing almost as strongly as the U.S. economy. European economic leading indicators, including the Purchasing Managers’ Index, have surged as a weak euro provides support for the manufacturing sector and provides a tailwind for corporate earnings. Exhibit 5

In conclusion, the base-case outlook in the aftermath of the U.S. election called for optimism. The markets responded in kind. The tail risks are now getting fatter. The risks to the outlook for U.S. equities, given the uncertainty surrounding the policy direction of the new administration and the prospects of Fed policy tightening,

are greater than they have been at any point in this cycle, including the Fed’s ill-informed interest rate hike in 2015. The potential for disappointment is high.

1. Source: CNBC, Nov. 30, 2016, Exclusive: Steve Mnuchin says there will be ‘no absolute tax cut for the upper class,’ http://www.cnbc.com/2016/11/30/exclusive-steve-mnuchin-no-absolute-tax-cut-for-the-upper-class.html.

Index Definitions:

The S&P 500 Index is a market capitalization weighted index of the 500 largest domestic U.S. Stocks.

The MSCI ACWI ex-U.S. Index is designed to measure the equity market performance of developed and emerging markets and excludes the U.S.

The Russell 2000 Index measures the performance of small capitalization U.S. stocks.

The Russell 1000 Index measures the performance of large capitalization U.S. stocks.

The Russell 1000 Value Index measures the performance of large capitalization value stocks in the United States.

The Russell 1000 Growth Index measures the performance of large capitalization growth stocks in the United States.

The MSCI Emerging Market Index is designed to measure the equity market performance of the emerging markets.

Markit Eurozone Composite Purchasing Managers Index is designed to measure the relative optimism of purchasing managers in both manufacturing and service sectors in the Eurozone and indicates the economic conditions of an economy.

Indices are unmanaged and cannot be purchased directly by investors. Index performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. Past performance does not guarantee future results.

Equities are subject to market risk and volatility; they may gain or lose value. Fixed income investing entails credit and interest rate risks. Bonds are exposed to credit and interest rate risk. When interest rates rise, bond prices generally fall, and a fund’s share prices can fall. Investments in securities of growth companies may be especially volatile. Foreign investments may be volatile and involve additional expenses and special risks, including currency fluctuations, foreign taxes and geopolitical risks. Emerging and developing markets may be especially volatile. Eurozone investments may be subject to volatility and liquidity issues. The mention of specific countries, regions, or sectors does not constitute a recommendation by any particular strategy or by OFI Global.

The views presented represent the views and opinions of OFI Global Asset Management. They are not intended as investment advice or to predict or depict the performance of any investment. These views are based on the information available as of the date noted and are subject to change at any time based on subsequent developments. OFI Global and OFI disclaim any responsibility to update such views. No forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of trading intent or holdings on behalf of any investment strategy. The information contained herein is deemed to be from reliable sources; however, OFI Global and OFI do not warrant its completeness or accuracy. Performance data shown represents past performance and is no guarantee of future results. This material does not constitute an offer or solicitation for the sale of any security or financial instrument in any jurisdiction where OFI Global, OFI or OFDI is not licensed to conduct business or where the security or financial instrument is not available for sale. No security or financial instrument is offered or will be sold in any jurisdiction in which such offer or solicitation would be unlawful.

OFI Global Asset Management (“OFI Global”) consists of OppenheimerFunds, Inc. and certain of its advisory subsidiaries, including OFI Global Asset Management, Inc., OFI Global Institutional, Inc., OFI SteelPath, Inc., OFI Global Trust Company and VTL Associates, LLC. The firm offers a full range of investment solutions across equity, fixed income, alternative asset classes, and smart beta. The views herein represent the opinions of OFI Global and are subject to change based on subsequent developments. They are not intended as investment advice or to predict or depict the performance of any investment. The material contained herein is not intended to provide, and should not be relied on for, investment, accounting, legal or tax advice. Further, this material does not constitute a recommendation to buy, sell, or hold any security. No offer or solicitation for the sale of any security or financial instrument is made hereby.

For Institutional Use Only. This material may not be further distributed or reproduced and may not be shown to, quoted to or used with retail investors.

© 2016 OppenheimerFunds, Inc. All rights reserved.

225 Liberty Street, New York, NY 10281-1008

BO0227.002.0217 February 28, 2017