"Given the confusion that can be created from the two different ways to calculate earnings, we think an old saying among investors perfectly applies: “profit is an opinion, cash is a fact.” "

Laton Spahr, Robert McClure, Eric Hewitt

Oppenheimer Funds, July 5th, 2016

Highlights

- We like companies when we see an acceleration of their Return on Invested Capital (ROIC).

- A company's dividend policy provides insight on whether it is deploying capital wisely.

- Accelerating dividends and ROIC have historically been good indicators of stock gains.

Laton Spahr, CFA

Value Team Leader, Portfolio Manager

Eric Hewitt

Portfolio Manager

Robert McClure

Senior Client Portfolio Manager

Earnings have traditionally been regarded as the key measure of a company’s success. Over the past several years, the markets have placed particular emphasis on quarterly earnings results. More recently, investors have started to focus intently on GAAP vs. non-GAAP earnings, with GAAP being the Generally Accepted Accounting Principles public companies must employ when reporting earnings. Non-GAAP, or pro-forma earnings, are generally presented at management’s discretion and can include or exclude various items, such as restructuring costs, intangibles or employee stock compensation, among others. There have been cases in which companies have reported a loss under GAAP accounting and a profit under non-GAAP!

Given the confusion that can be created from the two different ways to calculate earnings, we think an old saying among investors perfectly applies: “profit is an opinion, cash is a fact.” With that caveat in mind, the OppenheimerFunds’ Value team looks to a different measure when evaluating companies¯Return on Invested Capital, which measures the cash flow generated by a company’s underlying assets. With its emphasis on cash flow rather than earnings, ROIC is much less likely to be impacted by accounting distortions in the ways both GAAP and non-GAAP earnings can be.

Looking Through the Lens of Dividend Policy

Companies look attractive to us when we see an acceleration of ROIC. We look through what we call the Lens of Dividend Policy to determine if a company’s management is making the appropriate capital allocation decisions that will lead to an increasing ROIC.

A firm can allocate its scarce capital in a number of different ways. It can invest in its business by increasing its fixed assets or working capital or by spending more on research and development or mergers and acquisitions (M&A). If a firm does not have any attractive investment opportunities, it can also return capital to its investors. This can come in the form of repaying debt to bondholders, paying dividends to equity shareholders or offering share repurchases. The Value team focuses on dividends and share repurchases, as these are the most widely used tools of capital return.

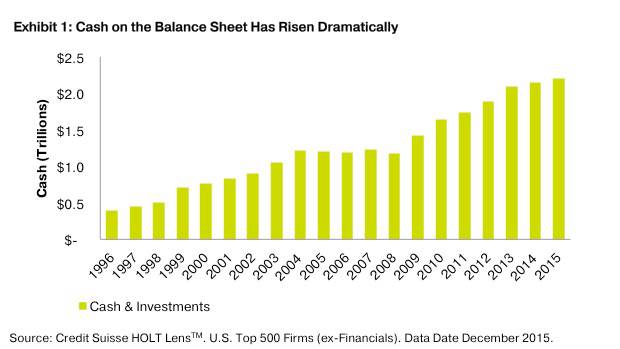

Much More Cash on Corporate Balance Sheets

Since the financial crisis of 2008, there has been a significant increase in the amount of cash on corporate balance sheets. Total cash balances have risen from $1 trillion to nearly $2 trillion.

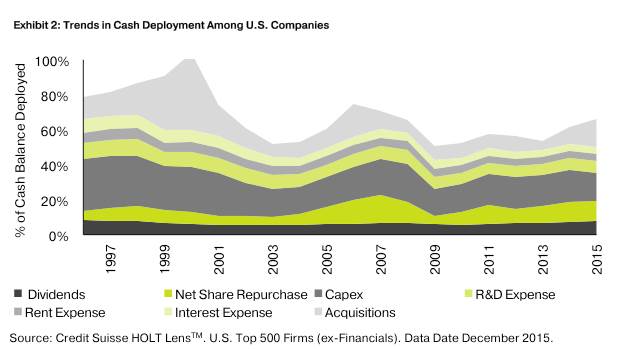

The key question is what will U.S. companies do with all this cash? Consider the historical trends, which are illustrated in Exhibit 2. The data reveal some interesting patterns:

- Capital expenditures, or investments in assets such as machinery and equipment, have been declining as a percentage of cash.

- Mergers and acquisitions, as well as share repurchases, have tended to track the performance of equity markets, as they’ve increased during bull markets and grinded to a halt in bear markets.

- On balance, dividend payments have been stable as a percentage of cash for a quarter century.

We believe the stability of dividends over time is an important trend that provides a key insight. From a behavioral standpoint, managements tend to be conservative with dividend policy, as shareholders generally want consistency in a firm’s dividend strategy. Investors value a regular, consistent cash payment in the form of dividends.

The frequency of share repurchases, on the other hand, tends to be volatile, and they are a representation of the firm’s cash flow generation in the past. We believe that management’s approach to dividends provides an insight into the company’s future.

A management that increases its dividend does not do so lightly. Generally, when a firm increases its dividend, it means its management is positive about the future and expects cash flow to increase. When they’re right, that increased cash flow brings an improvement in their ROIC.

When we conduct our research on companies, our focus on dividend policy often enables us to have much more strategic discussions with management teams. From these conversations, we gain insights on what their future capital allocation decisions will be and that provides a good indication of what their future ROIC may be.

Accelerating Dividends and ROIC Have Been Good Indicators of Stock Gains

Several of our holdings1 provide examples of how an acceleration of dividends has been a good indicator of strong stock performance.

- Walt Disney Company, a long-term holding in Oppenheimer Value Fund, has more than tripled its dividend since 2011 as revenues and margins have expanded at a healthy rate. That improvement enabled the ROIC to increase from 10% to 14%. As a result, the stock price has tripled during that period.

- Danaher Corporation, another of the Fund’s long-term holdings, increased its dividend by more than 400% between 2013 and 2015, even as the company continued to pursue an aggressive acquisition strategy. As a result of the company’s operating improvements, ROIC improved from 20% to 25% in this period and the stock price continued to outperform.

- AON, the large insurance broker and a more recent addition to the portfolio, has grown its dividends at a compounded annual rate of 15% over the past five years. The company has improved its ROIC by over 1,000 basis points during that period.

The OppenheimerFunds’ Value team focuses on identifying circumstances that are not widely recognized by the market and that will lead to an acceleration in return on invested capital. In our view, studying a firm’s dividend policy can provide us with important insights about the future direction of ROIC. We believe this gives us a more complete view of the underlying performance potential of a business than a focus on quarterly earnings can.

1. As of March 31, 2016, 0.50% of Oppenheimer Value Fund’s holdings were in the Walt Disney Company, 1.54% in Danaher Corporation, and 1.48% in AON

By reading this blog, you accept the Terms of Use and the OppenheimerFunds Distributor, Inc. PRIVACY POLICY/TERMS OF USE.

There is no guarantee that the issuers of stocks will declare dividends in the future, or that dividends will remain at their current levels or increase over time. Foreign investments may be volatile and involve additional expenses and special risks, including currency fluctuations, foreign taxes, regulatory and geopolitical risks. Emerging and developing market investments may be especially volatile. Mid-sized company stock is typically more volatile than that of larger company stock. It may take a substantial period of time to realize a gain on an investment in a mid-sized company, if any gain is realized at all. Value investing involves the risk that undervalued securities may not appreciate as anticipated. Diversification does not guarantee profit or protect against loss.

Holdings and sector allocations are subject to change, do not constitute recommendations by OppenheimerFunds, Inc., and are dollar-weighted based on total net assets. It should not be assumed that an investment in the securities identified was or will be profitable.

These views represent the opinions of OppenheimerFunds, Inc. and are not intended as investment advice or to predict or depict the performance of any investment. These views are as of the publication date, and are subject to change based on subsequent developments.